Weapons of capital preservation

Global equity markets had another positive quarter, continuing to build on the strong recovery from the COVID-19 lows in March. A flattening of the COVID infection curve helped calm market fears, while the aggressive stimulus by global central banks and governments allowed investment grade companies to access cheap funding and assist furloughed industries through the health crisis.

From a bottom up perspective, it has become increasingly clear that many large and important listed companies, particularly in the digital, healthcare and climate change sectors are well placed to grow post the pandemic. This has resulted in a bifurcated market since the March lows with structural growth stocks outstripping companies that are worse off in a post-COVID world.

This is most apparent in physical industries like retailing, banking, industrials, and travel. The differentiation in performance is stark when looking at the calendar year performance of the major indices in the US (S&P up 4.1% and the tech heavy Nasdaq up 24.5%). Meanwhile, indices with a higher concentration to more traditional industries have struggled with the US Russell 2000 (small caps) down 9.8% and the German DAX down 3.7%.

Market outlook

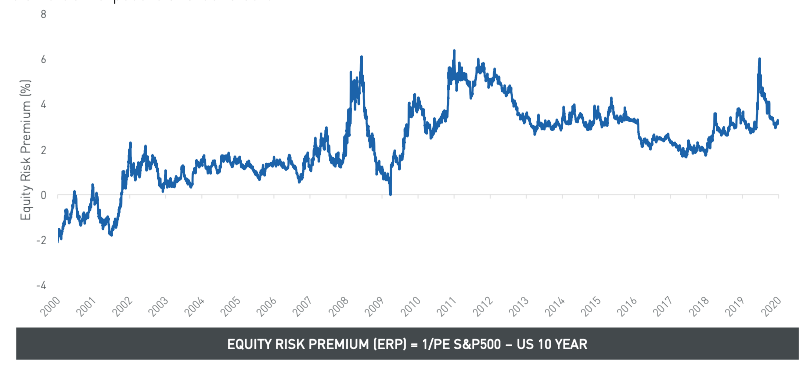

While acknowledging the strong market performance since the COVID lows, the equity risk premium available is still attractive with rates being held low (see chart below). Furthermore, we are excited about many of the Areas of Interest (AoI) emerging through the pandemic. We expect our companies in the Digital Enterprise, Digital Payments, eCommerce, Innovative Health and Climate areas to continue to deliver strong upcoming earnings results and provide bullish outlook statements.

Source: Bloomberg Finance L.P 30 September 2020

From a valuation perspective, we still see reasonable opportunities in these areas and note that in most cases the stock moves post COVID are simply reflecting a pull forward in market share gains. That is, much of this growth would have occurred anyway, but the disruption from COVID has accelerated these trends and pulled the gains into 2020. We would re-iterate that over the medium to long term it is far more important to correctly identify an area of structural growth and the companies set to benefit from that growth, than to try to predict the direction of the economy or market.

From a market risk perspective, we acknowledge the uncertainty leading into the US election (note: we see the primary risk here as being a contested election, or blue wave) but it is actually the uncertainty around the spread of COVID heading into the northern hemisphere winter that continues to be our bigger concern.

As such, we emphasise the importance capital preservation, but we do caution investors that not all tools will work as effectively next time around as they may have in the March quarter for clients in the Munro Global Growth Fund. This is partly due to the current high volatility causing higher put option pricing.

Capital preservation tools

Cash

Note the importance of being able to reduce net market exposure and raise cash levels if managers are uncomfortable with the market outlook and/or risks to the downside are judged to be elevated. For example, the Munro Global Growth Fund has a flexible mandate that allows it to hold up to 100% cash. In place is also are portfolio stop loss rules, with the investment team explicitly required to address the portfolio’s net market exposure at a 5% drawdown.

Put Options

Where risks in the market are judged to be elevated, funds often buys short-dated put option protection on major market indices. Option protection is also used on upcoming binary events such as major government elections, central bank meetings or exogenous events (e.g. COVID). Please note that put options are not always in place and may become too expensive a form of ‘insurance’ if volatility is already high.

Short Positions

Funds can short sell and consequently take advantage of falling stock prices as well as rising stock prices. This can occur when funds hold a negative view on a particular company, but it can also be used to hedge the underlying portfolio, for instance, by shorting futures contracts on the Nasdaq index.

Currency

During market sell offs, the US dollar often rises as a ‘flight to safety’ currency, causing the AUD to fall. Funds may hold higher exposure to USD assets as another tool to help preserve capital. Conversely, one could also increase AUD hedging to protect capital if the expectation is the AUD is entering a period of appreciation.

Stocks

Lastly, stock selection is a critical tool to help preserve capital: our Fund runs a detailed stop loss process on all its positions and when triggered instigates a formal position review process. While the Fund is not compelled to sell on these triggers, the review process is invaluable to identify at risk companies when the risks may not have immediately been apparent.

Two companies with strong tailwinds

Danaher

Danaher designs, manufactures and markets products and services in the sectors of life sciences, diagnostics testing and environmental sciences. We first invested in Danaher in February 2018 given the attractive end markets they were exposed to, with the characteristics of structural growth, resiliency during recessions and high recurring revenue from consumables. They have one of the best management teams and investment philosophies we have seen with their “Danaher Business Systems” (DBS) framework. Rather than grow margins by cost- cutting, the DBS process increases cost lines such as Research & Development (R&D) leading to more innovation and higher priced products and expanding gross margins. Those higher gross margins can then be partially re-invested back into R&D and sales & marketing (S&M), whilst letting some margin fall to the bottom-line.

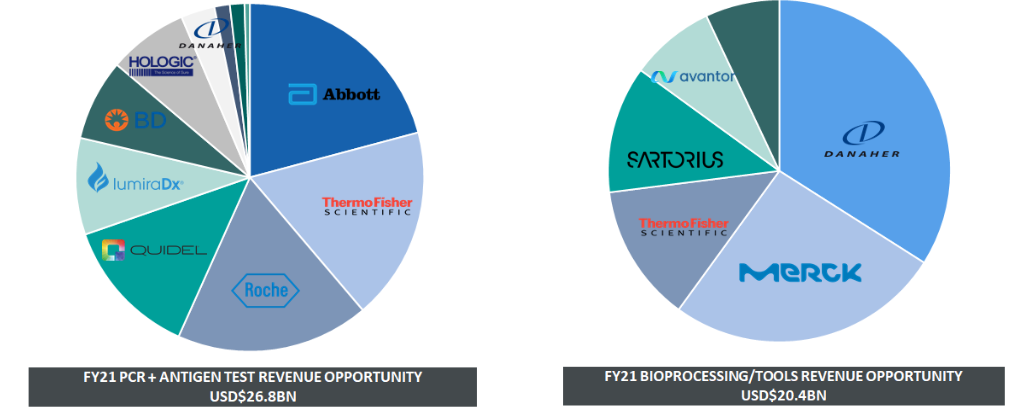

Since COVID-19, we have increased our position size in Danaher substantially. The arrival of COVID-19 gave the recent acquisition of Cytvia (GE’s biopharma business) an added growth driver – vaccine development and production. Danaher is the global leader in supplying instruments and consumables to the biopharma manufacturing industry (see chart below). The rush to develop and build increased capacity for COVID-19 vaccine development and production led to sales growth of >20% for Danaher’s operating businesses in this segment, up from a run-rate of high single digits. Assuming COVID-19 vaccines are developed and production occurs at large scale, growth for Danaher should continue to remain elevated.

Thermo Fisher

Thermo, like Danaher, is a leading life sciences equipment manufacturer. We invested in Thermo alongside Danaher because of how well positioned it was to benefit from some of the most important trends in healthcare, including the advancement of biologics, the advent of cell and gene therapy and personalised medicine, molecular diagnostics and, in materials science, the development of nanotechnology. The company’s leading market share across many of its addressed markets, combined with the depth of its product offering, enhances its ability to support growth and gain share.

We also increased our position in Thermo Fisher considerably on the back of the COVID-19 pandemic. Like Danaher, Thermo is a key supplier of instruments and consumables to the bioprocessing industry and so will benefit from the vaccine development and production. However, in the nearer the term, the biggest tailwind from COVID-19 is on the testing side. Whilst Danaher also has some exposure via their Cehpied business, Thermo has a larger exposure to this end market (see chart above).

Thermo saw a $1.5bn COVID tailwind in 1H20 and expects another $3bn in 2H20, driven by the sale of COVID related tests (now making over 10m kits per week, which will step up to 20m tests a week in October) and related reagents and consumables. This additional $4.5bn of revenue equates to an uplift of 18% on their 2019 revenue base of $25.5bn. This testing tailwind, along with the vaccine development tailwind, will persist for years to come for Thermo Fisher.

Final words:

Danaher and Thermo Fisher together look set to benefit for years to come from increased demand for their testing products as the virus remains, increased demand for their biopharma manufacturing equipment as the vaccine is developed and finally, from a step change in overall healthcare spending as governments seek to prevent further pandemics in the future.

Source: JP Morgan, Citi, 2020

Want to learn more?

Munro focuses on identifying and investing in companies that have the potential to grow at a faster rate and on a more sustainable basis than the peer group. To find out more, hit contact below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has over 20 years of financial services experience and over 14 years managing absolute return mandates focused on global growth equities.

........

The material contained in this publication is being furnished for general information purposes only as is not investment advice of any nature. The information contained in this document reflects, as of the date of publication, the views of Munro Partners and sources believed by Munro Partners to be reliable. There can be no guarantee that any projection, forecast or opinion in these materials will be realised. The views expressed in this document may change at any time subsequent to the date of issue.

This information has been prepared without taking account of the objectives, financial situation or needs of individuals. Before making an investment decision, investors should consider the appropriateness of this information, having regard to their own objectives, financial situation and needs.

Past performance information given in this document is given for illustrative purposes only and should not be relied upon as (and is not) an indication of future performance. No representation or warranty is made concerning the accuracy of any data contained in this document.

5 topics

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Nick is a founding Partner and the Chief Investment Officer of Munro Partners. He is responsible for the investment management of Munro’s key investment funds and the formulation and implementation of the proprietary investment process. Nick has...

Expertise

Comments

Comments

Sign In or Join Free to comment