Weekly S&P 500 ChartStorm - 23 Oct 2016

Those that follow my personal account on Twitter and StockTwits will be familiar with my weekly S&P 500 #ChartStorm in which I pick out 10 charts on the S&P 500 to tweet. Typically I'll pick a couple of themes and hammer them home with the charts, but sometimes it's just a selection of charts that will add to your perspective and help inform your own view - whether its bearish, bullish, or something else!

This week's ChartStorm highlights an important mix of technicals and fundamentals, which in combination could be the right mix to catalyze a grind higher in the market, and as outlined in previous editions: reinforce the seasonally positive last couple of months of the year...

The purpose of this note is to add some extra context beyond the 140 characters of Twitter. It's worth noting that the aim of the #ChartStorm isn't necessarily to arrive at a certain view week by week, but to highlight charts and themes worth paying attention to.

So here's the another S&P 500 #ChartStorm write-up

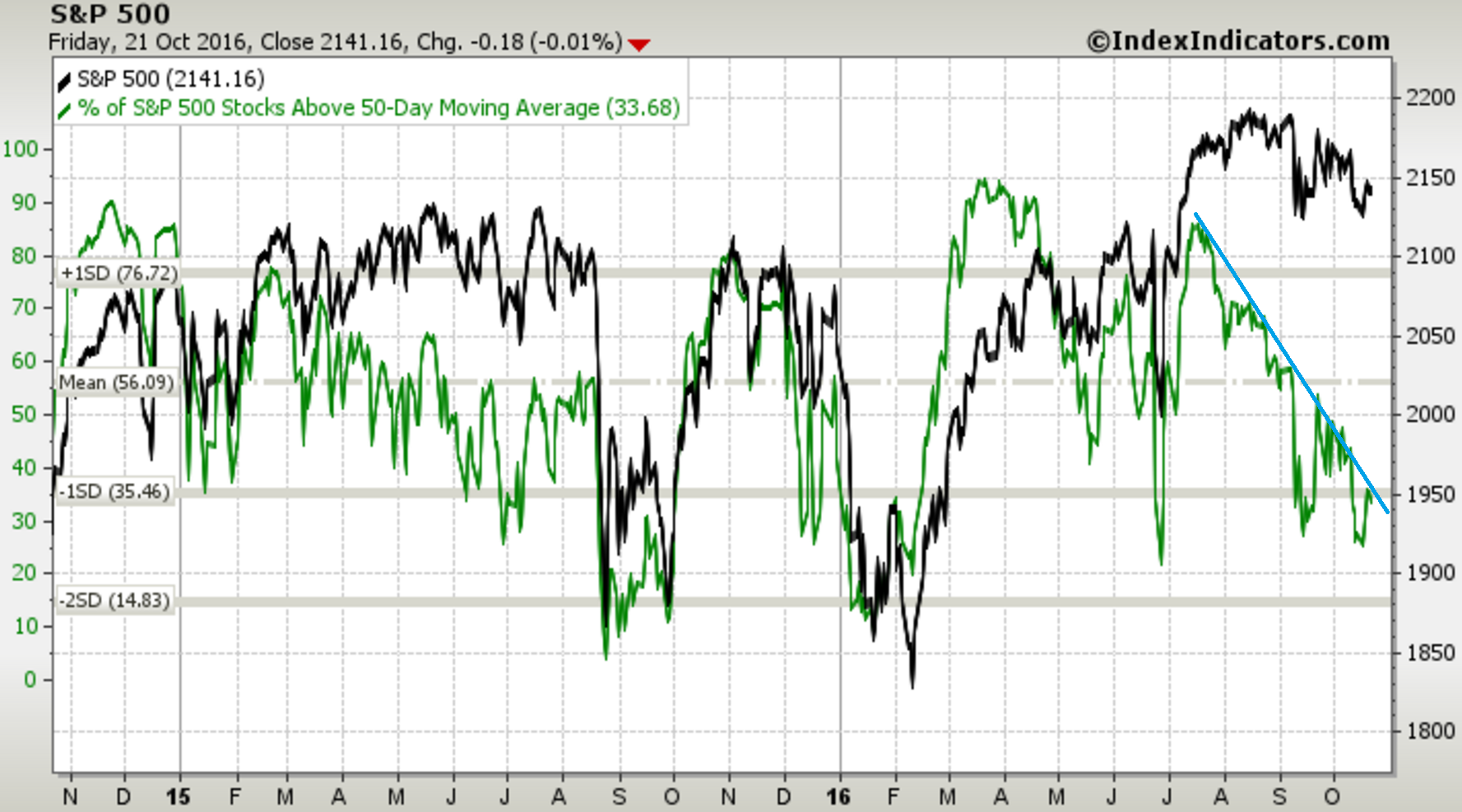

1. 50 day moving average breadth: The downtrend line in 50 day moving average breadth (VIEW LINK) of S&P500 companies trading above their 50 day moving average) remains, and the breakdown in breadth goes to show the underlying weakness in the market despite relatively little movement in the headline index. At present the indicator is around oversold levels, but the logical conclusion of the downtrend is some sort of deeper market selloff. By the same token a break of the trendline will be positive.

Bottom line: While 50DMA breadth is starting to look oversold, it remains in a downtrend.

2. 200 day moving average breadth: While 50DMA breadth has collapsed, 200 day moving average breadth seems to be holding up so far, with over 60% of companies still above their 200 day moving average - not at oversold levels, but with decent room to move to the upside. The issue is, visually it looks like it's rolling over. You also have a minor case of divergence in that price has basically been going sideways while breadth has declined - it's not true bearish divergence in that price is not going up while breadth is going down, but it does give pause for thought.

Bottom line: 200 DMA breadth has not declined to the same extent 50DMA breadth has, showing that there is a certain degree of underlying strength still there.

[2 200dmab.PNG]

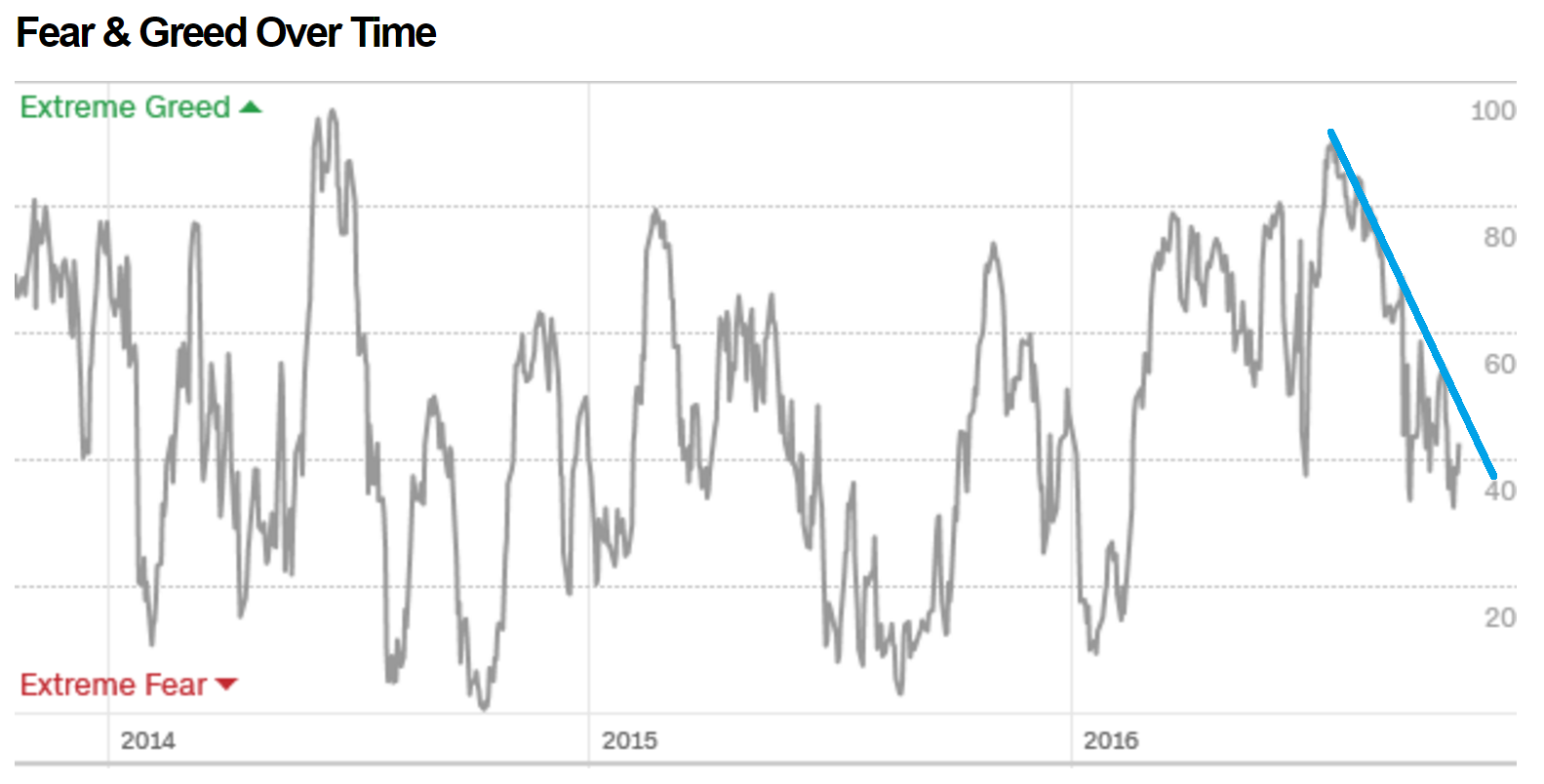

3. Fear and Greed: Similar to the 50DMA breadth, the Fear and Greed Index (VIEW LINK) has been trending down, and at some point if this trend continues it will show up as much less boring market activity. The other implication of the downtrend is that trendlines are made to be broken, and if and when it breaks to the upside it will likely be the part where the S&P500 breaks out of its trading range and heads to new all-time highs, until then tread with caution.

Bottom line: The fear and greed index is in a downtrend.

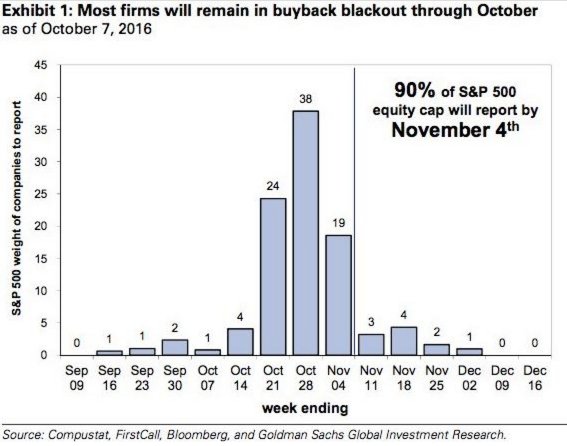

4. Earning season is upon us: The bulk of US Q3 earnings reporting takes place over the next two weeks, and if you were looking for a catalyst for either a continuation or break of the downtrend in the chart above, this could be it. Indeed, signs are coming through already that the earnings recession may be over and done...

Bottom line: Earnings season crunch time is now - a possible catalyst for a move.

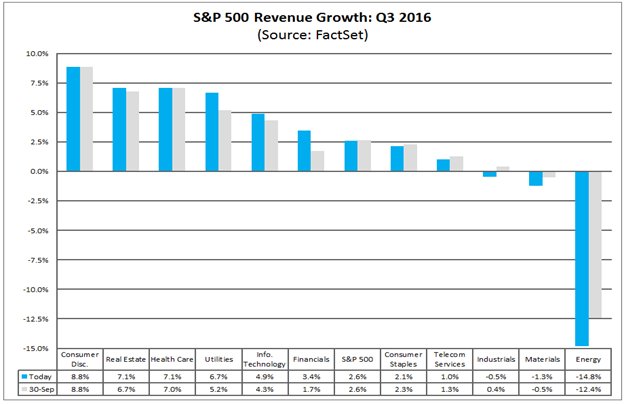

5. Sales growth: As FactSet (VIEW LINK) shows, sales growth has been going pretty well for most sectors of the S&P500 - this is not the type of chart you would see if there was a systemic issue or if the US was headed for recession. What is notable though is the divergence e.g. the services and consumer sectors are doing very well, whereas commodities and manufacturing - not so much. With commodity prices finding a floor and in some cases convincingly rebounding, the weak spots may well turn around soon.

Bottom line: Going into Q3 there are some decent results coming through on the sales side.

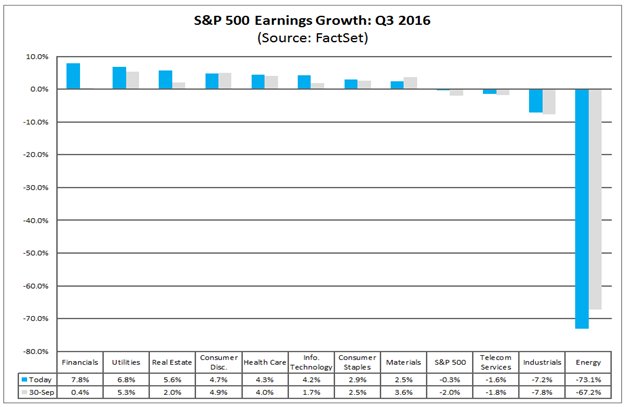

6. Earnings: As for earnings, it's a similar story in that energy is at the bottom of the table (because of the oil price crash and global supply glut). But a surprising standout lies on the other end of the chart - financials. If you recall, earlier this year the big concern was that financials were headed down the tubes again, but improving earnings will call that pessimism into question, particularly given the valuation adjustment that has taken place in financials. That aside, 8/11 sectors are seeing earnings growth, which is a clear majority.

Bottom line: The earnings picture, while slightly blemished by energy, looks fine.

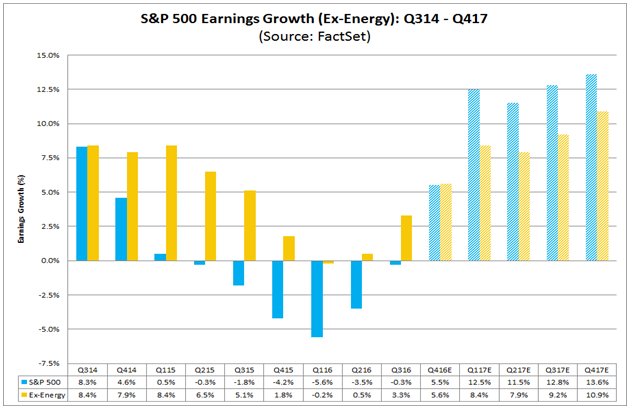

7. Earnings ex-energy: Another one from FactSet (VIEW LINK) - S&P500 earnings growth excluding energy. The reason you do this is that it shows the earnings recession was not really a systemic issue, i.e. it was concentrated in the energy sector. But that's not to say the rest of the market got a free ride, the impact of the US dollar surge was also a big headwind for a number of sectors, and can go a long way to explaining the weakness in some of the ex-energy sectors. Going into Q3 things look to be on the mend, and base effects will boost energy before long.

Bottom line: The earnings picture ex-energy helps see an underlying trend which is not as bad as might seem when looking at the headline S&P500 earnings picture.

8. Earnings/Economy leading indicator: While this chart stirred quite the controversy and comment when it was posted on twitter, the gap seems to be resolving in the direction we initially expected. The red line is the Economic Cycle Research Institute (ECRI) (VIEW LINK) Leading Growth Indicator. In the past this indicator has given a reliable lead to earnings momentum, and now does not seem to be any different. Already earnings momentum (VIEW LINK) picking up as expected - so earnings could be the fundamental catalyst to drive the market higher.

Bottom line: Earnings momentum is picking up as flagged by the ECRI leading indicator.

[spxearn out.PNG]

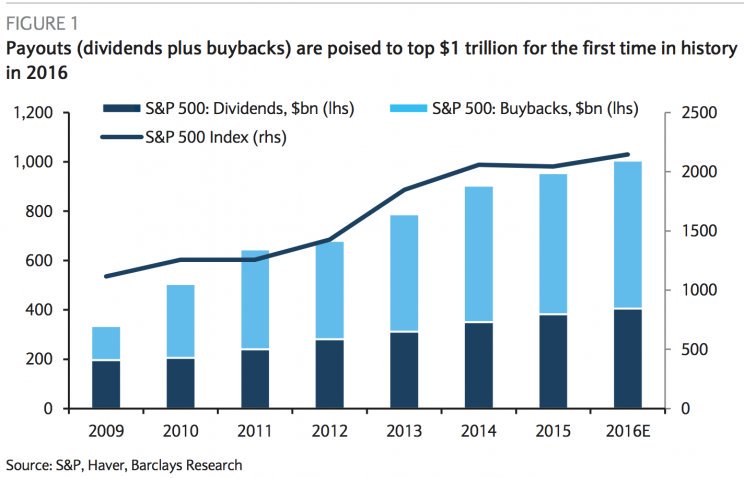

9. One trillion dollars: This is one for the interesting basket - dividends and buybacks (VIEW LINK) the S&P500 are set to top US $1 trillion this year, all time record high. It shows the force that buybacks have become, and just like dividends, once you start paying out to share holders they will keep wanting more and it wont even be good enough to pay out the same level let alone let it drop. So the question becomes, is the $1 trillion dollar mark a milestone or a potential headache in the making?

Bottom line: Dividends and buybacks combined will likely top $1 trillion this year.

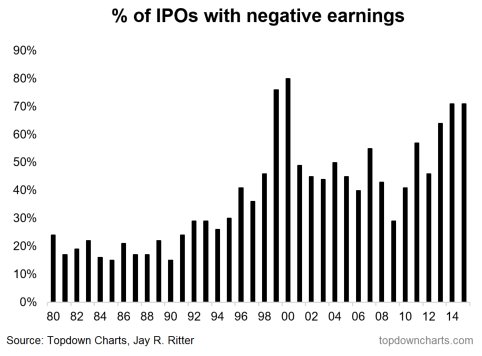

10. Loss making IPOs: Another interesting char is the proportion of companies going to market that were loss making. Over the past two years over 70% of companies that went to market had "negative earnings". It brings back memories of the 2000 dot-com bubble, but as the Topdown Charts blog (VIEW LINK) out, it's on lower IPO volumes, and it's largely driven by the Biotech sector.

Bottom line: The proportion of companies with negative earnings doing IPOs was over 70% in the past two years.

So where does all this leave us?

This week there's probably 2 key themes:

1. Breadth and sentiment lines

Charts 1 and 3 showed important downtrend lines - in sentiment and market breadth. These downtrend lines are important as the logical conclusion of their continuation is some sort of breakdown or capitulation in the stock market. The other key point is that trend lines are made to be broken, and when/if those two trend lines get broken to the upside things could move quickly and far.

2. Earnings trends

As Q3 earnings reporting season starts to ramp up signs are so far that earnings and sales outcomes are set to be pretty solid. Excluding energy (and including energy) the trend is clearly for improvement after a shaky patch. With base effects, and improving leading indicators, the all important earnings fundamental factor could actually be the catalyst the market needs to grind higher.

Summary

This week's ChartStorm highlighted an important mix of technicals and fundamentals, which in combination could be the right mix to catalyze a grind higher in the market, and as outlined in previous editions: reinforce the seasonally positive last couple of months of the year.

Article originally appeared here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Callum is Head of Research at Topdown Charts.

Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

4 topics

Callum is Head of Research at Topdown Charts. Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

Expertise

Callum is Head of Research at Topdown Charts. Topdown Charts is a chart-driven macro research house covering global Asset Allocation and Economics.

Expertise

Comments

Comments

Sign In or Join Free to comment