What Beyond The Rally?

There is one specific reason as to why I would caution investors to have high expectations about the local share market post October carnage, and that is because of US government bond yields, in itself the trigger to global share market weakness over the past two months.

No doubt Fed Chair Jerome Powell thought he'd sooth market fears about the Federal Reserve tightening too fast when he declared in early October US interest rates were still a long way off from reaching neutral territory, but financial markets received the message in a "OMG!, there is a lot more tightening coming" way, and down went equity markets.

The irony is that since October 3, the yield on 10 year US Treasuries has declined from 3.23% to 3.08%, but one should interpret this as the self-correcting mechanism that exists because of short term refuge being sought in the traditional US safe haven. (When more money flows into bonds, prices rise and thus yield drops). After all, these are US government bonds, the safest among all safe assets in our life time (at least in the short term).

About one month later, global equities seem extremely oversold, which is what one would expect given how savage the sell-offs have been, so assuming bargain hunters will start moving in, and investor sentiment as a whole can relax a little, this "relaxing" will not only translate into recovering share market indices, it will also lead to short term safe haven seekers abandoning the US bond market again.

Can everyone see where I am going with this?

Global investors worrying about what US bonds might do next are not in a position to now forget about US inflation, the Federal Reserve, the risk-free rate and global yields. Equities remain at risk of being a permanent prisoner of the global bond market, at least until current dynamics shift decisively either way.

And this still could well become a matter of be careful what you wish for.

Let's assume inflation does fall, which -all else being equal- would make a lot of sense given global growth is still decelerating, and has been for a while, thus removing the need for bond yields to rise further. They might even trend lower then.

How do you think this will impact on equities?

****

Australian investors already have witnessed what investor doubt about future growth prospects can do to share prices. FlexiGroup ((FXL)) shares are down -35% over the past three months, including a brief respite rally during reporting season in August. Automotive Holdings ((AHG)) shares are down -33% over the same period, and -43% over the past twelve months. Shares in EclipX ((ECX)) have lost -23% and -41% over respective horizons.

The local housing market is weakening, and has been for a while, and now retailers have started noticing a real impact on their sales numbers from households tightening their purse as the bricks and mortar wealth effect is evaporating. On Tuesday, as I am writing this Weekly Insights, cheap bling retailer Lovisa's ((LOV)) share price is down in excess of -19% after yet another disappointing market update from the sector.

Investors are responding by pulling money away from companies that are directly linked to either housing or consumer spending, and that is a big chunk of the Australian share market (including the banks, of course).

This indiscriminate selling is opening up opportunities for savvy investors who know better than to use the same brush for all listed companies -- REA Group ((REA)) and Carsales ((CAR)) spring to mind, but also Bapcor ((BAP)) and GUD Holdings ((GUD)) -- but this also puts one big dent into the ruling mantra that "value" investing is now making a lasting come-back, and "growth" investing is out of fashion.

Which is why this week's warning by Tony Brennan and James Wang, equity strategists at Citi, seems a little bit off the mark, unless one continues to look into the future with a rose tinted pair of glasses. Growth stocks are still trading on elevated multiples, and at a noticeable premium versus "value" stocks, the Citi strategists observe.

This, in their view, implies growth stocks remain at risk of further share price weakness. Granted, issuing profit warnings is no longer the sole privilege for structurally challenged "value" companies or local retailers, now high PE companies such as Kogan ((KGN)) and BWX ((BWX)) have joined in, but should we really compare these companies with the likes of CSL ((CSL)), ResMed ((RMD)), REA Group, et cetera simply because they are all trading at a premium to the lower value end of the share market?

In the short term, no such distinction might become apparent. Savage sell-offs have significantly dented investor sentiment and many would be in the mood to sell first, then ask questions, and see their actions being vindicated because of falling share prices, seemingly without any distinction on the basis of past track record, idiosyncratic quality characteristics, or reasonable growth prospects; but such distinction will establish itself at some stage.

Which is exactly why strategists at Macquarie continue to advise investors hold on to, or start buying shares in "growth" stocks such as Reliance Worldwide ((RWC)), a2 Milk ((A2M)), Cleanaway Waste Management ((CWY)), BHP ((BHP)), Aristocrat Leisure ((ALL)), Amcor ((AMC)), Seek ((SEK)), WiseTech Global ((WTC)), Orora ((ORA)), and others. All these stocks have weakened significantly in recent weeks, so now valuations have pulled back considerably, but these companies' resilience and growth prospects have not changed.

"In Australia", state the Macquarie strategists, "we think the call to buy value stocks won't work unless growth stocks continue to fall or value stocks begin to see an earnings improvement. We cannot see signs that the broader earnings environment is improving given the structural headwinds for large sectors such as banks, telcos, retail and other areas where there is “stroke of the pen risk” from government intervention (healthcare and energy)."

Which is why "value" stocks have not genuinely protected investors' capital during share market turmoil in October, and why I find it nigh on impossible to see any rotation in investor portfolios locally becoming sustainable. As I have pointed out on many occasions in the past: there is a seismic change taking place in the corporate sector, facilitated by innovation and technology, and this is not a one-off event.

The world is changing in front of our eyes, and these changes will be permanent. Losers do not become winners simply because of high yield or a cheap valuation. Short term maybe, not longer term.

In terms of stocks suited for income seeking investors, Macquarie suggests the Big Four banks, alongside Tabcorp ((TAH)), Challenger ((CGF)), Atlas Arteria ((ALX)), Sydney Airport ((SYD)), Transurban ((TCL)), GPT Group ((GPT)), and Scentre Group ((SCG)), but also Amcor, GUD Holdings, DuluxGroup ((DLX)), and Premier Investments ((PMV)).

****

It is important to note, housing market related weakness is not purely a domestic phenomenon. In the USA of Donald Trump, investors are equally waking up to the fact the domestic housing market is rolling over, and it has been for a while now. In Australia, this is one major input into why shares in Boral ((BLD)) are now a long way off from the $8 reached in early February. They closed just above $5.50 on Tuesday. Similarly, shares in James Hardie ((JHX)) and Reliance Worldwide, to name but two others in the same boat, are now equally well below price levels witnessed earlier in the year.

Two observations deserve to be highlighted in this context. One is that financial conditions are tightening in the US, and elsewhere, as one expects to happen because this is the explicit aim of Fed tightening. The second observation is that the housing market is often a leading indicator for the economic outlook in general terms, and this is of course because housing activity forms such an important ingredient for everything that moves inside an economy, and the US is no different. The fact that US housing market momentum is decelerating noticeably, and has been for a number of quarters, should thus have every investors' attention.

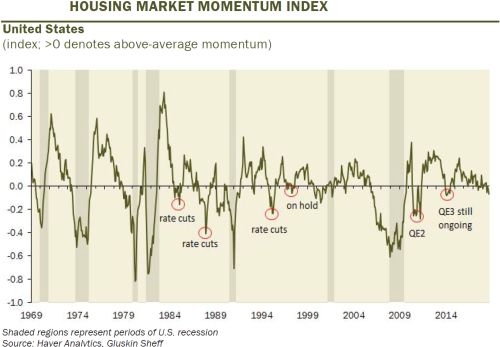

Glushkin Sheff chief economist and strategist, David Rosenberg, has kept an eagle eye on the US housing market for a prolonged time, and he sees no good things happening. Last week, he presented a proprietary index for US housing market momentum, combining signals from data such as new home sales, existing home sales, building permits, housing starts, etc into one easy-to-read momentum index.

That index (see below) has now fallen into negative territory. Of most importance, and as pointed out by Rosenberg, going back five decades, every single time when this index has broken below zero, either the Fed was easing policy or the US economy was on its way to the next economic recession.

This time around the Federal Reserve is tightening, and Chair Powell, and other members of the Federal Open Market Committee (FOMC), the board that votes and decides on interest rate hikes, is explicitly of the intent to continue hiking rates.

****

Could it be that, beyond the portfolio rotation out of excessive investor exuberance and higher bond yields, investors are already preparing for a much slower growth environment for US companies and the US economy? After all, the world's most influential economy has just printed GDP growth of 4.2% and 3.5% respectively for the past two quarters. Not exactly numbers that should have anyone worried about corporate profits and economic health, or so it seems at face value.

At face value, yes, but what if we look beneath the bonnet?

Then we find that Q3 growth was boosted by consumers drawing from their savings while businesses were building inventories and the US government was spending like a drunken sailor (look up: Iceland and US marines). Larger inventories are most likely in anticipation of trade tariffs. Underlying, argues Rosenberg, true economic growth is sub-2%, which will become apparent in the quarters, and the year, ahead.

Increased business capex in the aftermath of the infamous Trump tax cuts seems to have been a brief phenomenon only. The US housing market already is weak (see above). For US consumers, the wealth effect from a raging bull market for equities is no longer.

For good measure, the Chicago Fed National Activity Index, which combines a gargantuan 85 different economic indicators, has now separated itself from the monthly PMI readings, instead falling to a four-month low of 0.17 in September, essentially indicating US growth momentum is slipping, not holding up.

Many of the bullish arguments and forecasts I have read over the past month or so concentrate on the fact that US companies are still growing at a healthy pace, while the US economy continues to churn out healthy data and indicators, irrespective of tariffs, rising bond yields, Fed tightening, a strong US dollar, and economic momentum weakening elsewhere (including, ominously perhaps, in Europe).

I now suspect this bullish picture will increasingly come under closer scrutiny, including from Fed officials. This makes it extra-difficult to make confident forecasts about what might, is likely, or rather unlikely to unfold for the remainder of 2018, and for the year ahead.

But it is most likely most appropriate to dial back too optimistic scenarios from here onwards, and adopt a more measured, cautious, less-risky portfolio composition, in line with events, and my writings, of the past weeks.

In terms of the bigger picture, the MSCI All-Country Index, which shows the broader trend and picture for equities globally, effectively peaked in early 2017 and since an ever smaller group of equity markets kept on marching higher, until US markets were left as the last ones standing tall. Then October 2018 happened.

To some commentators, US equities forever marching on while the rest of the world was no longer able to looked simply like an unsustainable situation. Now that the US has been pulled in line with the rest of the world, investors have been made aware of the many tangible risks out there. Let's not get ahead of ourselves, but also, every investor should realise there is no guarantee of a positive outcome either.

This is the time to remind ourselves, investing is about managing risks.

****

For the FNArena/Vested Equities All-Weather Model Portfolio, the first four months of financial year 2018/19 have equally brought about above average volatility, and this for a portfolio that most times exhibits less fluctuations than the broader Australian share market.

After a successful eighteen months until 30th June, July saw slight underperformance versus the ASX200 Accumulation index (+0.85% versus +1.39%), after which August reversed back into outperformance (+2.53% versus +1.45%), and then September reversed positions again (-2.8% versus -1.26%); pretty much in line with global portfolio rotation.

This implied that by the close of the September quarter, the portfolio had slightly underperformed (+1.23% versus +1.53%). October is not yet finished, but up until today a slight outperformance has occurred (note prior to today's sharp rally, the ASX200 Accumulation index was still down -7.7% for the month thus far, having been down -8.73% last week).

On my observation, each share market sell-off in recent years has had its own specific character. This time around, owning high quality, structural growth stories didn't help much, but moving money into safe cash has made a difference.

Also note that while the ASX200 Accumulation index is now in negative territory for the running calendar year (with only two more months left) the All-Weather Model Portfolio has thus far remained in positive territory, despite extreme draw downs and volatility.

Total performance for the six months to June 30th was +6.86%. For the full financial year ending on June 30th the portfolio's performance was +16.59%.

FNArena provides impartial and independent market analysis and commentary, as well as proprietary tools and insights into the Australian share market. Our service can be trialed for free at (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

FNArena is a supplier of financial, business and economic news, analysis and data services.

3 topics

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

Comments

Comments

Sign In or Join Free to comment