What keeps Charlie Jamieson up at night?

Do you remember last year when US 10-year government bonds cracked 3%? I do. Everyone started talking about flattening yield curves, a potential recession in the US and Jamie Dimon said the 10-year could hit 5%…

Widely regarded as the risk-free rate used for the pricing of all other assets the 10-year is kind of a big deal. So, when I flicked on my screen in 2019, I was somewhat shocked to see the US 10-year yield at just 2.70%, which is only fractionally higher than it was a year ago.

Something happened in the last few months of last year that hosed down rate hike expectations. I thought I’d fire a few questions at Charlie Jamieson from Jamieson Coote Bonds to get a run down on what changed plus a few other points of interest.

---------

Q1. Charlie, what have been the primary drivers or catalysts that led to the big move lower in bond yields?

When you pull on a rubber band hard enough, at some point it snaps. The rise of US interest rates has been pulling on/tightening the global economy for a few years now. Late last year, the expectation of higher rates combined with liquidity withdrawal (central bank balance sheet reduction) caused the markets to snap with equity markets and corporate credit bonds melting, while government bonds enjoyed a flight to quality rally as the preeminent ‘’defend and protect’’ asset class. This made government bonds the best performing asset class of 2018.

This is important because it highlights how portfolio diversification and risk balancing delivers optimised portfolio solutions for investors.

Q2. I understand that the Fed was quite vocal in late December. What did they say, how is this different to their previous message and what are the implications?

The Fed completed a 180-degree turn in six weeks regarding their outlook for monetary policy and balance sheet normalisation (liquidity withdrawal) which is in stark contrast to their messaging in early October. This is very concerning and means that our global central bankers cannot forecast with accuracy the impacts of their new policy tool of Quantitative Easing (QE)/Tightening (QT). Remember, since the 2008 GFC we have been playing with financial nitroglycerine. This hasn’t been trialled before and no one knows how it will end.

Q3. I’ve had a few conversations with investors who thought the market got spooked by the Fed’s change in narrative? Do you think they saw something in the US economy that gave them major concerns?

The sell-off in corporate credit spreads was a major influence for the Fed, as corporate credit markets have a history of seizure (think GFC), starving the economy of corporate debt funding whilst jamming investors in corporate credit with mark to market losses. This tightens financial conditions quickly and becomes a self-fulfilling death spiral for the economy which requires material policy intervention.

Q4. The strength in US Dollar has been playing havoc with Emerging Markets – is there any relief in sight?

No. Emerging markets borrowed heavily in USD, debts which must be serviced from their domestic currencies. The lifting of US interest rates makes US dollar bonds more appealing with higher income yields which is keeping the USD strong as a currency. Emerging markets have also been the major beneficiary of excess liquidity chasing yield/returns. That theme, driven by accommodative central bank policy via quantitative easing is now complete as we are rotating from quantitative easing to quantitative tightening.

So Emerging markets face a twin battle of both higher debt servicing costs and a lack of capital sponsorship as excess liquidity is withdrawn.

Q5. In July last year you wrote a piece saying that the Fed would again over-tighten. Does their change in narrative make you think they’re more cognisant of this risk in the current cycle?

We believe the Fed has already over tightened, as not only have interest rates moved from 0.00% to 2.50%, but QE has turned to QT which shows significant additional tightening. The lag effect of higher funding costs and reduction in liquidity takes significant time to bleed through into the data, remember the Fed stopped hiking interest rates in June 2006, but the GFC didn’t really kick off until mid 2008, some two years later.

Q6. You also spoke at Livewire Live and referenced yield curve flattening and that this has been a good predictor of US recessions. That’s an alarming prospect, but the yield curve never inverted so clear sailing, right?

Image: Your author speaking with Charlie Jamieson at Livewire Live 2018

Image: Your author speaking with Charlie Jamieson at Livewire Live 2018

Parts of the US Treasury curve inverted last year, with 3 year and 5 year bonds trading at lower yields than 2 year bonds. The highly referenced 10 year versus 2 year bond yield finished 2018 at a differential of +19 basis points, down from +51 at end of in 2017 and +125 at end of 2016, Today at time of writing that is now +17. This theme has been a wonderful predictor of US recessions with a lag effect of 6 to 12 months.

Buckle up, the second half of 2019 or early 2020 looks to be the landing zone and markets will move well ahead of time.

Q7. In that same July article, you noted that domestically calls for a rate cut would grow as 2018 progressed. That’s proven to be the case. Do you really think the RBA will cut rates? How would that help?

What happened to all those strategists and economists that forecast rate hikes last year? In a world addicted to cheap and freely available debt, the calls for rate cuts will grow as the Australian economy continues to tighten, led by housing and residential construction downturn. The RBA could cut rates to offset this tightening and attempt to re-ignite demand. We think the bar to rate cuts is pretty high at a domestic level, as increased government spending will help offset near term housing weakness. A global shock (which has a high probability at end of cycle) is a more likely catalyst for the RBA cutting to restore confidence.

Q8. Orderly or Disorderly? What’s your current view on the price action in domestic residential property?

So far the market downturn has been orderly, but it will likely crescendo with a disorderly pop. We have written about ‘’forced sellers’’ driving valuations quickly lower. This is the mechanics of market price action and will likely be triggered by excessive leveraged participants, who no longer hold sufficient equity, being stopped out.

Q9. Nearly there... What keeps you up at night from a markets perspective?

A failed corporate credit refunding. The structures of the corporate credit market remain weak with a huge debt build up from low interest rates, combined with poor credit quality, and poor secondary market liquidity.

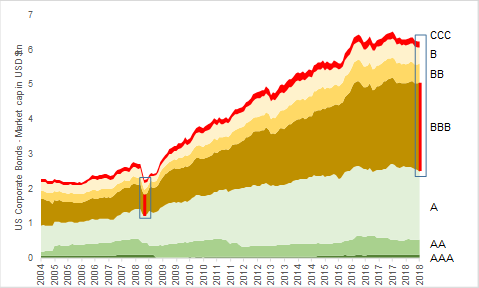

A failure to roll corporate credit debts forward would be a shock to markets with systemic implications for all asset markets.

Figure 1. Market capitalisation US corporate bonds by credit rating: the quality of corporates has deteriorated with greater debt issuances in lower quality segments.

Q10. Could you sum up your view on the outlook for government bonds in just a few sentences?

A critical evergreen ‘’defend and protect’’ allocation which provides government guaranteed returns, excellent liquidity and often negative correlations to riskier assets for material portfolio benefit – as 2018 has just shown. As we are now towards the end of global rate hiking cycle championed by the US Federal Reserve, bonds will likely perform very well versus other asset classes, albeit at a fraction of the market risk.

Disclosure: Like most investors, I have a diversified portfolio and I remain heavily allocated to both domestic Government Bonds and Global Government Bonds.

Never miss an update

Stay up to date with my latest investor interviews by hitting the 'follow' button below and you'll be notified every time I post a wire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions.

Safe investing and thanks for reading Livewire.

1 contributor mentioned

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets