What Mattered Today; Banks Seasonality working to offset Materials & Energy

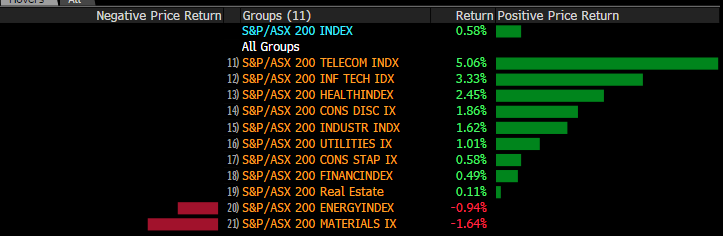

It feels like we’ve been writing about Trump / trade wars & tariffs all week with market movements based on the rhetoric coming out of Washington. By weeks end though, markets had settled and all sectors on the Australian bourse (except energy) actually closed higher with the ASX 200 putting on 0.57% / 34pts over the week.

Weekly Sector & Market Performance

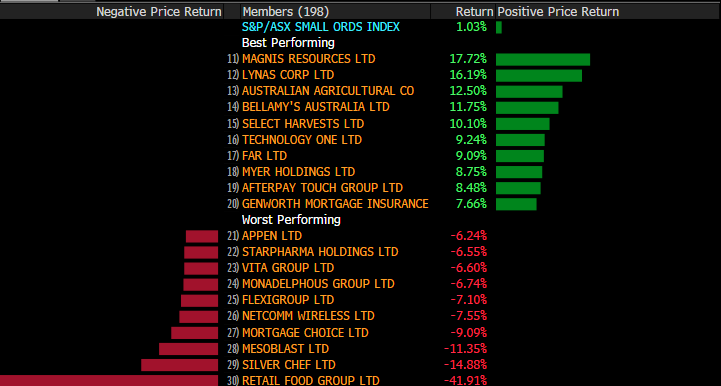

Looking at key stocks on the week in both the large caps and the Small Ords shows another period of big underlying moves – not to the extent we saw during official reporting season but still worthy of mention.

Starting in the Small Ords, Lynas (LYC) was a standout on the back of a better report early in the week, a turnaround story and that’s being reflected in the four fold increase in the share price since 2017. On the flip side, Retail Food Group (RFG) has found itself in a world of pain following difficulty finalising their results and subsequent negotiation with bankers around debt covenants. They now hold $260m in debt with a market cap of $217m and an earnings picture that it under significant pressure. To us, this is simply unsustainable and a real risk to the company’s ongoing viability. Silver Chef (SIV) is another one under pressure with their Auditors putting big question mark over their recent set of accounts – again, a stock we would have no interest in even at these depressed levels.

Small Ords Weekly Performance

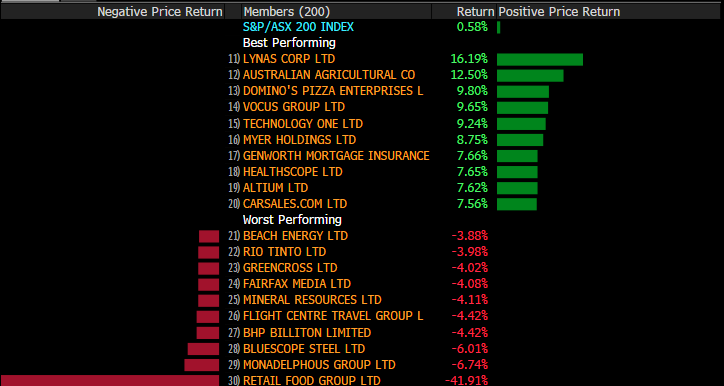

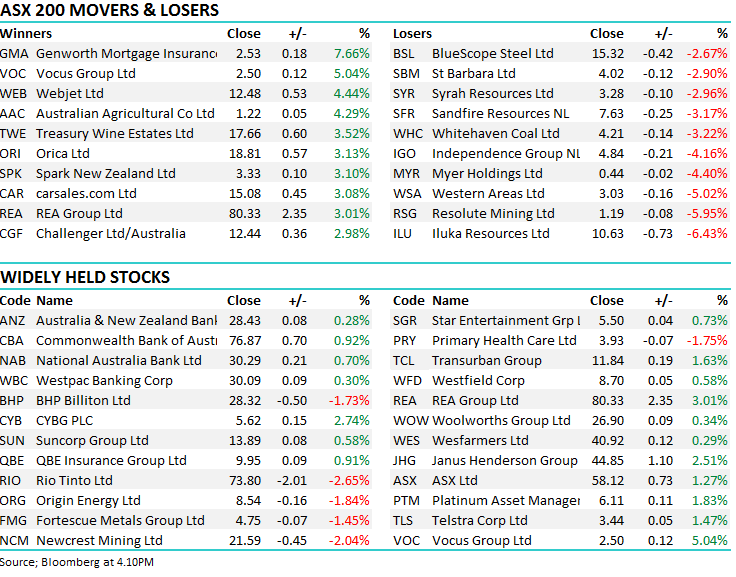

In the larger cap space we saw some relief buying in Australian Agricultural (AAC) and Genworth (GMA), the latter of which we hold in the MM Income Portfolio. This has been our worst performing investment since the portfolios inception with the stock owing us $2.79. We maintained our position through the recent weakness for 3 main reasons.

1. The company has a buy back in play that ‘should’ have been providing some support to the stock

2. The parent company that still owns 26% of the stock is a natural seller, some relieve should be seen if / when their stake is placed and there are rumours this is about to happen

3. The company has a huge amount of excess capital on their balance sheet that should (ultimately) find its way back to shareholders.

The stock closed today at $2.53 up 7.66%. On the flipside, Myer has been dumped from the ASX 200 which put pressure on the stock today, however they are in the green for the week.

ASX 200 Weekly Performance

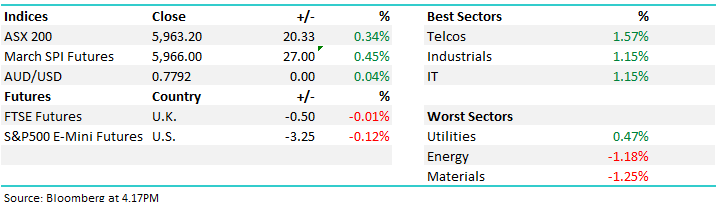

Today, the S&P/ASX 200 Index finished 20 points higher to 5963 points - a rally of 0.34%.

ASX 200 Chart

ASX 200 Chart

CATHCING OUR EYE

1.Macquarie Group $105.46 / +1.38%; A good day today with the stock breaking out to new highs. We outlined 5 shorter term plays to look at this morning and Macquarie was one of them. We hold the stock in the MM Platinum Portfolio and wrote the following in the AM report day….We believe MQG will make fresh all-time highs in the very near future – we’re long and happy! Its strong correlation to US indices which are again looking excellent adds weight to this opinion.

- Buy MQG below $104.50 targeting over $110 with stops below $101.60 – note only ok risk / reward but the bullish trend is very strong.

Also, once / if MQG breaks above $105.60 technically stops could be raised to $103.80 making the risk / reward more attractive!

Macquarie (MQG) Chart

2. Bank seasonality; We’ve written a number of times recently about bank seasonality with the March / April period being a very strong one for the sector – today the banks got into the groove and rallied nicely – CBA adding 0.92% to $76.87, NAB adding 0.7% to $30.29, ANZ adding 0.28% to $28.46, and WBC up by 0.3% to $30.09.

Here’s a quick look at the seasonality for CBA over the last 10 years. Typically, CBA will put on +6.5% over the March / April period and this is clearly the time to be / stay long the sector.

Have a great Weekend,

James & the Market Matters Team

The above is an extract from the Market Matters Weekend Report. For a free 14 day trial of our service CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

6 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why my mum might help pop the CBA bubble

Elston Asset Management

Equities

Is the end of globalisation the end of global equity investing? The follow up...

Arteqin Capital Limited

Education

Missing the first double on this biotech star

Livewire Markets