What Mattered Today; Wesfarmers picks a poor day for a poor update

A day of mixed fortunes for Australia today with Hemsworth and co promoting Aussie tourism with the much anticipated Super bowl ad aired at halftime during the Philadelphia Eagles victory over the New England Patriots…not sure how the wider response has been but I quite liked it – CLICK HERE to view if any interest. A less positive day for investors though with the market whacked by -95pts suffering from the US led hangover of rising interest rates fuelled by signs of rising wages re-focussing attention back onto the outlook for inflation. In short, rates are going higher but the market is obviously concerned whether or not the Federal Reserve is behind the curve. If inflation spikes then the markets obvious conclusion will be that the Fed has acted too slowly to raise rates, and their hand may be forced to go harder and faster than they / the market would like, but as they say one hot day doesn’t make a summer!

It is interesting to think about the state of play in US equities – January was exceptionally strong, the best January since 1997 and investors piled into US stocks, cash levels are now low, margin loan origination and quantum has become high and optimism was rife. That rally in Jan was clearly unsustainable and we’re seeing a sharp sell off as a result. Despite the reasoning provided above – higher rates – inflation expectations and the like, I think it’s simply a case that US equities were overextended and needed to pause / pullback. reiterating our views from this morning which todays trade does not alter;

- We are looking for the US S&P500 to correct another say 4% during February.

- We believe this is the “Warning Shot” for stocks that we have discussed a number of times over recent months for a short-term buying opportunity.

- We still see fresh highs from US stocks, potentially into the dangerous April / May timeframe where we are likely to become aggressive sellers.

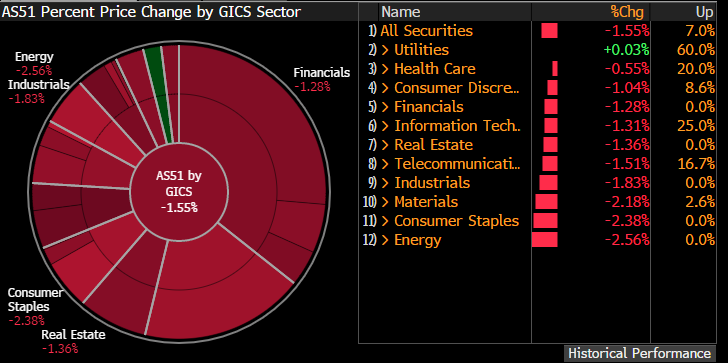

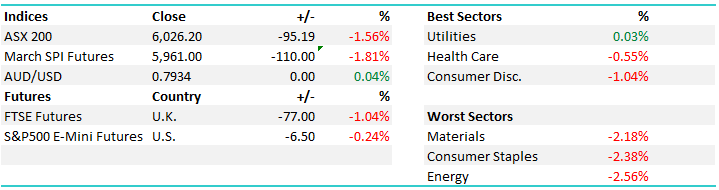

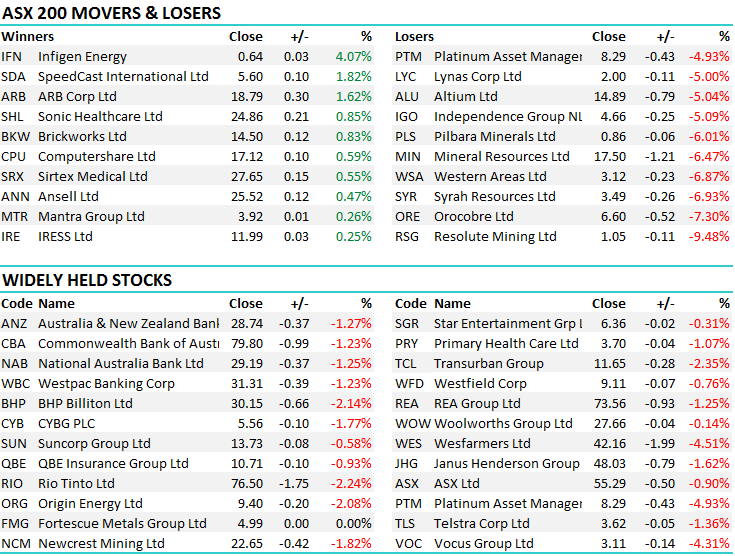

The Australian market actually did ok today given the torrent going against it. A drop of -1.56% versus the -2.5% drop in the States on Friday – plus US Futures were weak on our open, down another -0.5% before clawing back some of it, while trade in Asia was also soft – hard for our market to do any better than it did given the negative international and regional influences. The Energy sector was hardest hit in America on Friday and the local sector followed suit today while a downgrade from Wesfarmers put the kibosh on the consumer staples – WES taking a whopping 8.5 index points off the 200 today.

Source; Bloomberg

Source; Bloomberg

Looking at the 2 MM Portfolio’s is interesting today – performance in periods of market weakness are always telling. The Platinum Portfolio was down, pretty much in line with the mkt but cushioned partially from our cash weighting (a daily movement of -1.4%) while the Income Portfolio lost 0-.53% - about a third of the mkt decline. That portfolio holds 55% equities and the rest in more defensive income securities & cash, however the equities have a value bias, no expensive growth stocks and that approach is shown to work better in periods of weakness / volatility.

More broadly today, the S&P/ASX 200 index lost 95 points, or -1.56 per cent, to 6026, the broader All Ordinaries index also fell -101 points, to -1.63 per cent, to 6128, while the Australian dollar reached US79.31c.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

CATCHING OUR EYE

1.Wesfarmers (WES) $42.16 / -4.51%; Hit hard today following a review of their underperforming divisions – basically Bunnings United Kingdom and Ireland (BUKI) and Target – which has prompted them to take write downs, mostly non-cash but it’s still not a good look. They say poor trading (and execution) in both entities are to blame and the mkt suddenly gets the Masters induced shudders. Although it’s a poor update for these divisions, the BUKI division is running pilot programs only and is not big driver for growth now while target has been weak for ages. This announcement will obviously take some heat out of the recent share price momentum, but what’s more important is what will Coles do in the face of a resurgent Woolworths, given Coles’ poor LFL comps from 4Q16 to 1Q18, and increased competition in the Supermarkets segment? Interestingly, this was new CEO Rob Scott’s 1st major news announcement, and clearly not a strong start – will his tenure now be a case of being continually on the backfoot repeatedly over the coming years as the market questions the validity of persisting with the BUKI expansion every result?

We think Wesfarmers trades lower, and will present an opportunity around $38 - to receive an alert on this and other trades we are taking now - sign up for a free 14 day trial - CLICK HERE

Wesfarmers Daily Chart

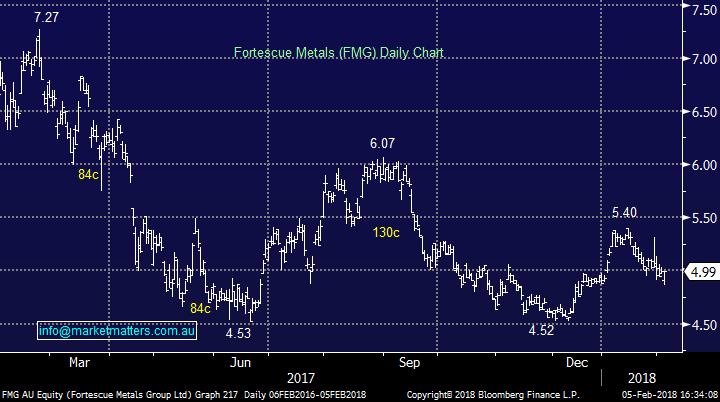

2. Janus (JHG) &Fortescue (FMG); Both on our radar at the moment with FMG showing resilience today in the face of a weak market which highlights underlying appetite for the stock. We bought in the income portfolio below $5 and remain comfortable here , while Janus is fast approaching our $47 target after a poor session today that saw the stock off by 1.62% to close at $48.03.

Fortescue Metals Daily Chart

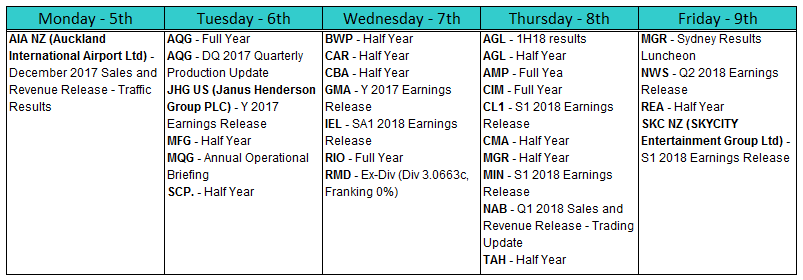

REPORTING THIS WEEK

No real companies of magnitude today however things kick up from tomorrow onwards.

James & the Market Matters Team

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

3 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment