What's next for AREITs?

Alex Cowie

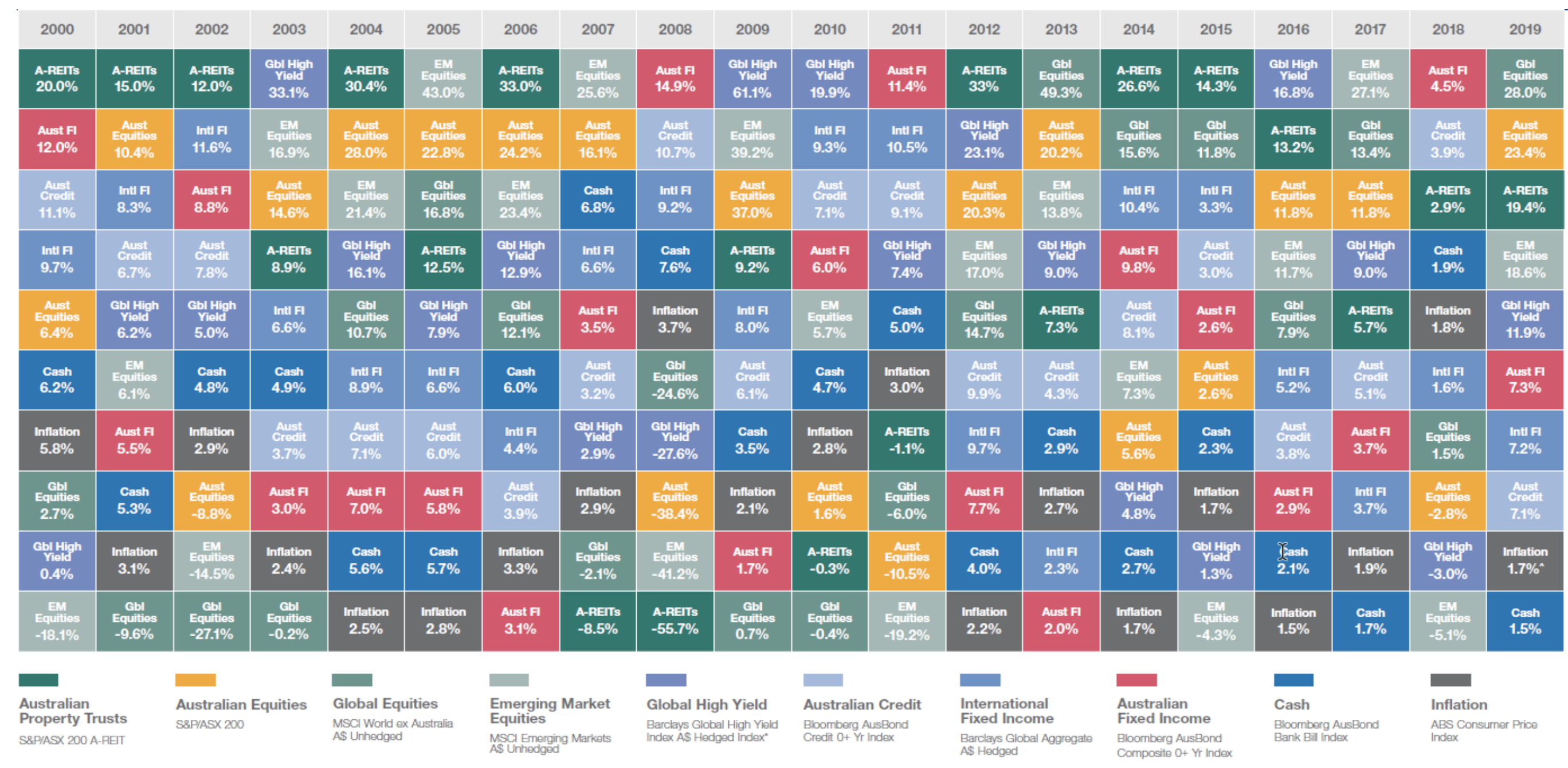

Australian Real Estate Investment Trusts (AREIT) have been the best-performing asset class during eight of the last twenty years, and have performed well in most of the other years. The table below, published at the start of this year demonstrates this clearly, with AREITs in dark green at, or near to, the top of most columns.

Source: Schroders

Source: SchrodersThe stark exception to this trend was during the GFC when AREITs were the worst-performing asset class during both 2007 and 2008, with moves of -8.5% and -55.7% respectively.

Is 2020 going to be another one of the sector's horror years? Over the last month, the index has halved in short order, touching levels not seen since June 2012.

This dramatic fall has been even worse than that of global peers, given the local skew to retail, a sector that was already looking sick but is now in an induced coma. Scentre Group (SCG) for example, fell by 65% on the back of seeing malls and some offshore locations being closed in Europe and the US.

However, like the rest of the market, the index is now starting to bounce, and brave souls that bought on the lows are now sitting on a more than 20% gain in a few days.

Where to from here?

To get a handle on the state of play, and to see if an opportunity is appearing here, I listened in on the latest webinar conducted by sector experts APN Property Group, hosted by their CEO Tim Slattery, and Pete Morrissey who heads up their real estate securities team.

With this year's crash evoking painful memories of the GFC for many investors, Pete Morrisey emphasised the solid fundamentals of the sector today versus those against the GFC. Pete said:

"A-REITs are in a significantly better financial position than they were in the GFC. Balance sheets are extremely well-managed, with the average debt on the sector at its lowest level since the late 1990s. It is just chalk and cheese, compared to where things are at today, compared to that entering the GFC. The majority of the REITs, right now, sit at the lower end of their target gearing band, meaning they have a lot of capacity to absorb this. They have a lot of cash-on-hand to assist in getting through this really tough time. The average debt maturity is over 5.5 years, across the sector, with hedging of almost 80%. So balance sheets are very well-positioned and will benefit from far more debt diversification than in the GFC period, with Australian banks being in a far stronger position. We can't necessarily rule out the prospect of a capital raising, across some of the names, if there was a continuation of the recent moves. But A-REITs are, realistically, in the best position they possibly could be, to absorb the sell-off that has been occurring".

This theme of robust fundamentals repeated through the webinar: with references to tenant strengths, good balance sheets, manageable amounts of debt, and the reliability of earning streams.

Expanding on their Convenience retail REIT (AQR) as an example, Tim Slattery discussed the makeup of the portfolio, emphasising the low gearing and the defensibility of its earnings:

"It's a portfolio of long lease term service stations. It has a weighted average lease expiry of over 11 years. Full occupancy at 100%, and it has gearing of less than 30%, at balance date. Based on all the public information that is out there, for Convenience Retail REIT, you would see that its earnings, before interest, would need to fall by over 60%, or interest rates would need to rise to over 11%, or the value of this property portfolio would need to fall by 40%, before banking covenants would be reached. The portfolio there is valued, on a weighted-average cap rate, of 6.9%, and has a range of national and international tenants, in its portfolio. We believe that that cap rate of 6.9%, in a collapsing interest rate environment, certainly needs to be viewed with some perspective.

During the Q&A at the end, one listener posed a frank question around how long key holding, Scentre Group, could survive without reaching covenants. Pete answered by saying:

Assuming malls remain open, which the Prime Minister has indicated they are an essential service, SCG's liquidity position is currently $1.8 billion. So very significant to cover all their CY20 debt maturities, in the event that re-financing is not forthcoming. The debt level of Scentre Group, it's an A credit rating with S&P and Fitch, so that is high. The highest in the A-REIT sector, and one of the highest in Australia. Its gearing is at 33%, with its covenant around gearing at 65%. So, in a worst-case scenario, say the malls close. A sensitivity analysis indicated they have sufficient funding to meet all their interest rate obligations for 8 months, if they didn't receive any income. Clearly, that isn't going to happen. The other thing is that almost a quarter of Scentre Group or Westfield sales relate to basic essential goods, such as grocery, fresh foods, so they will, in fact, be receiving income, through this period.

The sector is clearly under extreme duress right now, with a great deal of uncertainty remaining. There has certainly been chatter of price movements being aggregated by the sale of one large portfolio in the sector, as well as the activity of quant traders.

The question now is whether the dramatic market reaction has overshot, leaving a sector boasting strong fundamentals but trading at firesale valuations. If so, then the current set up could be the foundation for 2021 to be yet another year that sees AREITs at the top of the asset class performance tables again.

Access a steady stream of reliable income

To find out more about the income options that APN Property Group provides, please click the 'contact' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Featuring

Tim Slattery,

Dexus

Tim leads APN’s team and is responsible for setting and implementing APN’s strategy and growth objectives and the investment performance of APN’s investment products and the company itself.

2 stocks mentioned

1 contributor mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment