Stocktoberfest: When rotation goes too far

Charlie Aitken

Aitken Investment Management

Aristocrat (ALL) has had a poor performance period, down 15% from recent highs, but I believe at current levels represents an opportunity. The selling in ALL can be attributed to a variety of developments:

Firstly, we have seen globally and locally a rotation from higher PE “growth” stocks to lower PE “value” stocks.

Secondly, the Australian Dollar appeared during September to have made a short-term bottom and ALL is a majority USD earner: that AUD rally has since reversed in October.

And thirdly, analysts have been trimming their Aristocrat EPS forecasts marginally to reflect higher Design & Development costs (D&D) as management has guided to a step up in content development at the newly acquired digital subsidiaries Big Fish and Plarium. There has also been speculation of a large transition based seller of ALL, driven by an investment mandate loss.

While I strongly believe we are witnessing the early stages of a rotation from growth at any price (GAAP) to value/growth at a reasonable price (GARP) as long bond yields break higher, inside that rotation there will be stock specific bottom-up investment opportunities where the rotation has gone too far.

I believe ALL around $28.00 now represents one of those opportunities as the investment arithmetic is compelling.

The graph below overlays the ALL share price and current year consensus EPS forecasts (red line).

Consensus EPS forecast for 2018 for ALL have been lowered by just -1.4% over the last month, yet remains +18.8% higher than this time 12 months ago. ALL shares have dropped ~15% since their late July peak. The consensus FY19 P/E is now under 19.4x, yet we believe the stock offers another year of 20% EPS growth. At a PEG ratio of under 1, that is an opportunity ahead of a seasonally strong period for the ALL share price.

Catalyst ahead

In terms of catalysts, the annual G2E gaming was held in Las Vegas last week. It has typically been a positive catalyst for the stock because ALL presents market-leading products and content to industry participants as well as buy and sell side analysts. We see no reason for the conference this year to be any different given the level of investment into design and development remains ahead of peers. We do expect G2E to reinforce ALL’s market-leading position. Aristocrat is then due to report its 2018 financial year results on the 29th of November (ALL has a September year end).

Key fundamental drivers

In addition to a change in market sentiment and positioning we see several key fundamental drivers of upside to Aristocrat at current levels:

- Organic Growth: ALL’s 2018 earnings (to be released in November) should show organic earnings growth for the business of around 23%. This growth is being driven by solid performance from its core North American gaming operations and also from its existing digital business (Product Madness). Industry feedback, surveys and performance data all suggest that Aristocrat is still winning share in the US gaming market.

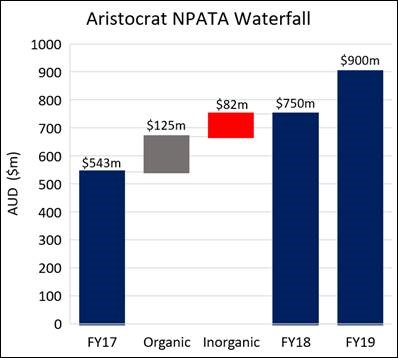

- Inorganic growth: ALL made two meaningful and highly strategic digital acquisitions in this financial year (Plarium for US$500m in October 2017 and Big Fish for US$990m in January 2018). Both acquisitions were fully debt-funded meaning that they are highly accretive to EPS. These acquisitions will provide a significant contribution to FY18 numbers – in our estimate contributing 15% earnings growth to ALL. See below an NPATA waterfall chart based on AIM estimates for the next two FY results highlighting the split between organic and acquired earnings growth.

Source: Company Data, AIM Estimates

FY19 will be the first annual period with a full year inclusion of Plarium and Big Fish and we conservatively forecast that organic growth will step back to around 20%.

ALL should be a significant beneficiary of the US tax reform given that around 70% of Aristocrat’s earnings are from the United States. However, given existing transfer pricing arrangements between Australian and US subsidiaries, this benefit will take a few years to come through. Guidance for FY18 is a 29% effective rate. This should progressively step down towards around 24% over the next few years providing another tailwind to earnings.

The following graph highlights that Aristocrat is trading more than 1 standard deviation below its 2 years average PE ratio after the recent sell-off. This is in stark contrast to most other “growth” stocks which are trading well above long-term averages.

With this in mind, we believe ALL at the current share price levels offers a compelling opportunity. Aristocrat remains a top 5 holding for the AIM Global High Conviction Fund.

We prost Stocktoberfest with...

Good old Victoria Bitter!

Did you enjoy that?

Aitken Investment Management employ a high-conviction thematic long-short strategy, investing primarily in listed global equities, as well as selected commodities, currencies and derivatives. For more information please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire