Where to for the economy and sharemarket as we head towards 2021?

Looking at the sharemarket’s performance over the last few months, some would be tempted to assume that the worst of the economic damage inflicted by the COVID-19 virus is well behind us. Economically sensitive sectors like Banks and Resources have led the rally, while many of the strongest-performing stocks have also been some of the most speculative, such as those in the buy now pay later sector.

The heavy sharemarket falls in March reversed fairly quickly thanks in large part to the massive fiscal programmes quickly put in place by governments as well as the cutting of interest rates and other unprecedented QE programmes from central banks. This has helped boost liquidity and spending power at a time when many businesses have been closed and unemployment numbers have spiked to levels not seen for several decades, both in Australia as well as in the United States and Europe.

In Australia, the Federal Government quickly implemented major stimulus programmes such as JobKeeper, JobSeeker, and other grants and payments which have boosted cashflow for many businesses and employees who were ‘stood down’. The Reserve Bank of Australia cut interest rates twice in March and implemented a bond buyback (quantitative easing) programme. The Federal Government also put in place a ‘Code of Conduct’ for landlords and tenants to reduce/defer rental payments. The banks also introduced deferrals of borrowers’ interest payments, initially due to expire at the end of September 2020, but since extended to the end of January 2021. Finally, employees have also been able to draw down their superannuation early, adding substantially to disposable income.

Company earnings and share prices both locally and globally have been – and are still being – driven by an extraordinary combination of factors. Some sectors, such as many retailers like JB Hi-Fi and Bunnings, have benefitted greatly from the huge short-term sugar hit of COVID-19 income support plus super withdrawals, while other sectors – such as travel, tourism, tertiary education and hotel accommodation – have seen their activity down anywhere between 50 and 95%.

More broadly, a decade of ultra-low monetary policy stimulus has injected massive liquidity into the global economy and significantly influenced investors’ expectations and behaviours, while the low yields from term deposits and bonds have also driven investors into the sharemarket in search of yield.

Add to that the COVID-19-driven fiscal stimulus of unprecedented government support for incomes and loan repayment delays, and feverish momentum-driven buying of ostensibly glamorous sectors such as the ‘buy now pay later’ companies, and you get a sense of what an extraordinary time we are living in.

These factors have in combination played a big role in helping the Australian sharemarket recover to the 6,000 level, well above the 4,500 level in March. Other markets like the S&P500 have rallied to within reach of their record highs thanks to similar drastic actions by US authorities. Many US technology stocks have been trading at record highs as people stuck at home have reverted to using online services such as Amazon, Netflix, Facebook and Google in record numbers.

All of this has created a ‘perfect storm’ in which focusing on good quality, defensive stocks that represent good value and a proven ability to generate and grow recurring earnings over time has led many funds – such as Investors Mutual – to continue to underperform relative to the broader sharemarket.

The question then is: have Governments and relevant authorities done enough to buffer the economy from the worst of the recession so the economy can get to the ‘other side’ of the pandemic smoothly as things return to ‘normal’? Is the sharemarket rally justifiable and sustainable? These are almost impossible questions to answer given the diverse factors at play, although we remain cautious about the outlook, and highlight the reasons why we continue to skew our portfolios defensively.

Reasons for Caution

ANZ has forecast that government stimulus has injected around A$64 billion into the pockets of workers and businesses in each of the June and September quarters. These programmes are due to roll off towards the end of 2020 and are expected to add A$24 billion in stimulus in the December quarter, a fall of A$40 billion representing around 9% of GDP.

The government also allowed early access to superannuation from mid-April, with payments of up to A$10,000 per person in the June and September quarters. The most recent data from the Australian Prudential Regulation Authority indicates that applications of A$30.7 billion were received to 26 July, while a further A$12.6 billion of applications have been received so far in the September quarter.

When the change in government stimulus is combined with reduced access to superannuation withdrawals, there appears to be a likely fall in liquidity of some A$68 billion in the December quarter. To put these numbers into context, Australian GDP was A$1.95 trillion in fiscal year 2019, or about A$500 billion per quarter. Reducing liquidity by A$68 billion is approximately 13.6% of GDP in a normal quarter in a quarter when tourism, hotels, hospitality, international education and many other industries look like they are going to remain heavily affected.

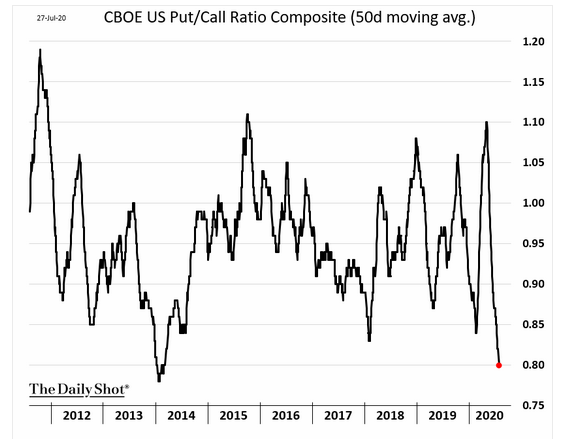

Another reason to be cautious is the apparent apathy from many investors to the recession we are still working our way through. We can see this from indicators such as put/call ratios in the US. Figure 1 shows that many investors do not appear to be expecting any downside from sharemarkets. The chart shows the 50-day moving average of the CBOE US Put/Call Ratio Composite Index, a measure of sentiment of future market direction, based on tracking volumes of puts and calls in the US sharemarket, providing a gauge of the feelings of investors and traders. The graph shows the current put/call ratio at extreme levels, indicating increasing complacency on the part of US sharemarket investors. When this complacency is so extreme, it’s often an indicator that a correction is not far away.

Figure 1: US Put/Call Ratio Composite Index

Index Source: The Daily Shot

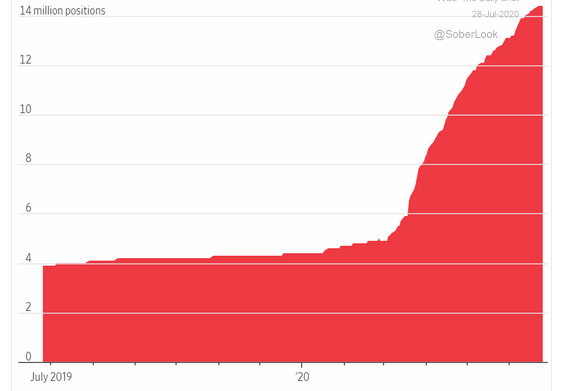

Another indicator which makes us cautious is the enormous growth in the number of day traders, potentially indicating a high level of speculative activity in sharemarkets. Figure 2 tracks the number of users of the Robinhood trading app taking positions in S&P500 Index stocks. We can see the sharp spike since the second quarter of this year, as people with time on their hands and the availability of effectively free, technology-driven trading have entered or re-entered the market, producing a wall of ‘hot money’ which has further pushed up many companies’ already rich valuations. Australian Securities & Investments Commission data has shown a similar trend – surges in daily turnover from retail brokers and sharp increases in the number of new trading accounts and a resumption in trading from a large number of previously dormant accounts.

Figure 2: Increase in Number of Robinhood User Positions in S&P500 Stocks

Source: Robintrack via Goldman Sachs, data to 25 June 2020

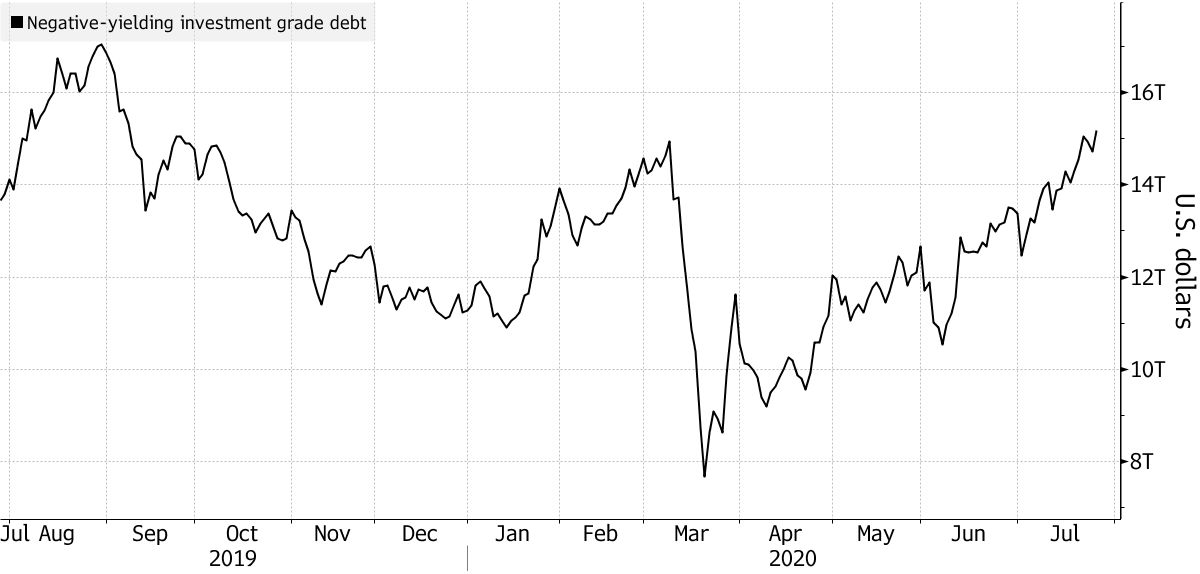

Our final graph shows another significant issue for investors – the increase in the amount of US corporate bonds with negative yields, which has almost doubled from approximately USD8 trillion in March to about USD15 trillion by the end of July – a truly extraordinary occurrence. These negative yields have occurred in large part as a result of the US Federal Reserve supporting bond markets – including the junk bond market – by buying USD120 billion a month of bonds to keep the system flush with liquidity and to support financial markets.

This level of QE is clearly not sustainable in the longer term, and at some stage, bond markets can be expected to return to some sort of normality, where investors are actually paid a return in the form of interest for taking some risk!

Bond markets’ return to more ‘normal’ levels will also have an impact on sharemarkets, as equity risk premiums will rise to better reflect the rising bond market returns.

Figure 3: Increase in Negative-Yield US Investment-Grade Debt

Source: Bloomberg

Outlook Going Forward

It’s still extremely difficult to understand what ‘normal’ is going to look like for many sectors as we head towards 2021. While the JobKeeper and JobSeeker income supports have been extended until March, which will help reduce pain for many individuals and businesses and provide further near-term support for some sharemarket sectors, it’s difficult to see how this can be sustained indefinitely. There’s a real prospect of a ‘fiscal cliff’ in coming quarters.

The other major issue is the higher level of unemployment in the year ahead. On top of the current official 7.4% unemployment rate, Macquarie Bank estimates around 3.5 million of Australia’s 14 million-person workforce – the equivalent of 25% of Australia’s registered workforce – are currently on JobKeeper. How many of these ‘stood down’ workers will have a job to return to remains uncertain, as many sectors are unlikely to recover quickly. Given this, the number of unemployed could rise rapidly to over 10% as we head towards 2021, which will be a major headwind for the economy.

Diminished household spending power, record household debt, and higher unemployment are therefore likely to weigh increasingly on economic activity and on many Australian companies’ earnings in FY 2021 and potentially into FY 2022. Many companies are actively looking to reduce their labour forces and defer or cut capital expenditure because of the uncertain outlook in 2021.

Looking beyond our shores, the US hit its first ‘fiscal cliff’ at the end of July with the failure to pass additional measures extending the Coronavirus Aid, Relief, and Economic Security (CARES) Act income and loan supports, which has already had an impact on retail foot traffic in states with higher unemployment. Developments in the US in the coming months will provide telling indicators of the likely effects of the withdrawal of equivalent stimulus in Australia. The run-up to the US Presidential election in November – with the prospect of potential changes in corporate tax rates and other economic policy settings – as well as escalating US-China trade disagreements are also likely to inspire potentially greater volatility on world markets.

Conclusion

We believe that the recovery phase for the Australian economy will be prolonged, rather than V-shaped, with weaker household income and an uncertain corporate earnings outlook leading to sharemarket volatility, as optimism wavers about how quickly many companies’ profitability will return to pre-virus levels. As a result, we have positioned our portfolios to focus on companies whose earnings are not dependent on a V-shaped recovery and which in our view are reasonably valued, have strong competitive advantages, and are run by experienced, capable management teams that can navigate the impending uncertain economic times.

Investors faced with the prospect of persistently low interest rates will continue to seek higher yields from the sharemarket. In an environment where an increasing number of companies are likely to be reporting lower earnings and dividends, investors will increasingly gravitate towards those with defensive characteristics such as proven sustainable earnings and dividend yields. We believe this will be more supportive of the prices of the quality industrials we favour such as Amcor and Orica, and we expect these companies to do well as we head towards 2021.

Learn more

IML has a conservative investment style with a long-term focus and aims to deliver consistent returns for clients. To find out more, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality and value'.

Anton arrived in Australia in the 1980’s and was soon drawn to the sharemarket at a time when high-flying entrepreneurs dominated the headlines. His passion for investing in the sharemarket has not waned and he continues to put his considerable experience and the important lessons learnt over the last three decades to mentor the IML investment team and to deliver to clients' expectations.

4 stocks mentioned

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets