Where to next for gold?

Q1 2020 was another positive one for gold, with the price rising by 4% in USD terms. The rally, which saw the gold price end March 2020 just below USD 1,600 per troy ounce, marks the sixth straight quarter of price gains, with the yellow metal up by 32% over this time period.

Australian dollar investors have had an even better time in recent months, with gold ending the quarter above AUD 2,500 per troy ounce, a new all-time high, with the price up by 56% since September 2018.

The strong price gains in gold, combined with the vicious sell off in global and Australian equity markets in Q1 2020 has seen investment interest in gold pick up considerably. Perth Mint gold coin and minted bar sales more than quadrupled between February and March 2020 (silver sales also tripled), with March sales 186% higher relative to the same month last year.

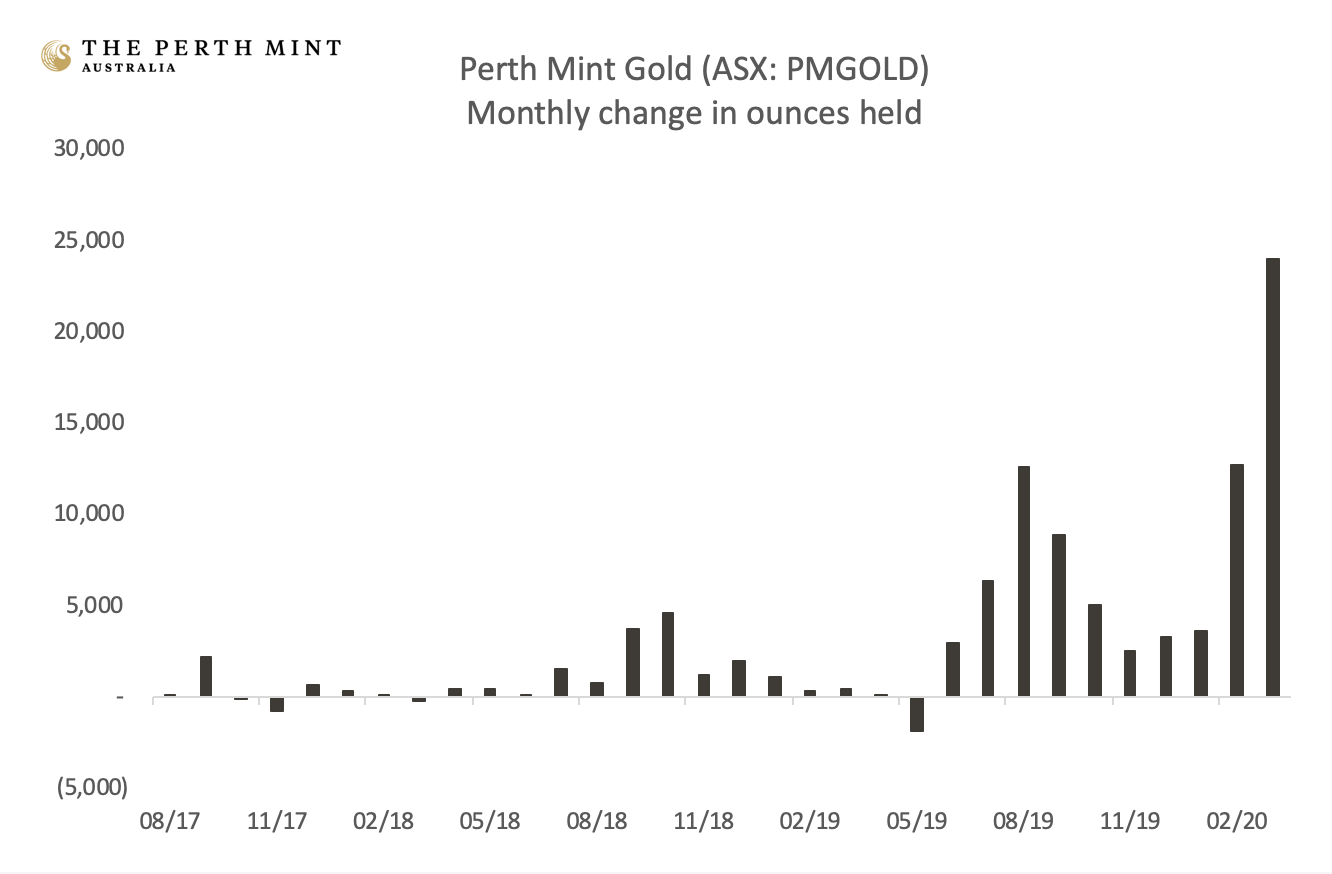

The sharp increase in investment interest can also be seen in the chart below, which plots monthly inflows (in ounces) into Perth Mint Gold (ASX:PMGOLD) since late 2017.

Source: The Perth Mint

At almost 25,000 ounces, inflows in March 2020 were the highest on record, almost doubling the previous monthly record, which was set in August of last year. Since September 2018, when this gold rally started, holdings in PMGOLD have more than doubled.

Strong demand is also evident across other ASX listed gold vehicles , with the total value of all gold exchange traded products (ETPs) rising from AUD 786 million in September 2018 to AUD 2.03 billion by end February 2020.

Gold investors should be very happy with the performance of the yellow metal over the past 18 months, however looking forward there are a number of factors which could push prices in either direction, some of which are listed below.

Potential headwinds

- Gold and the USD have risen together for most of the last 18 months, but continued US dollar strength could hold gold back, especially if we see a sharp spike higher in the greenback.

- Low and rapidly declining inflation expectations may subdue gold prices, though gold has rallied strongly in prior periods of low inflation.

- Russia halting official purchases of gold takes out a large buyer, though net central bank demand is likely to remain positive in 2020.

- Sell off in silver and gold stocks: Strong precious metal bull markets often see silver and gold stocks outperform gold to the upside. This has not happened this time, with the gold to silver ratio ending Q1 2020 above 110, a huge increase from end 2019 when the ratio was just 85. Gold stocks (as proxied by GDX) were also down, falling by over 20% for the quarter.

Potential tailwinds

- Gold is strongly outperforming equities, with the S&P 500 to Gold ratio dropping from 2.13 at end December 2019 to 1.77 by end March 2020. This should help attract additional inflows from investors.

- Emergency fiscal stimulus and monetary policy easing are likely to support gold, with the balance sheet of the US Federal Reserve already exceeding USD 5 trillion. Unlike prior iterations of quantitative easing, there appears to be no upper limit to the current programme.

- The majority of global sovereign debt now trades at negative real yields, making gold a high yield (and zero credit risk) investment in comparison.

- Continued uncertainty regarding the impact of coronavirus on economic growth should also help support gold, even if a global recession is now the ‘base case’ for most investors.

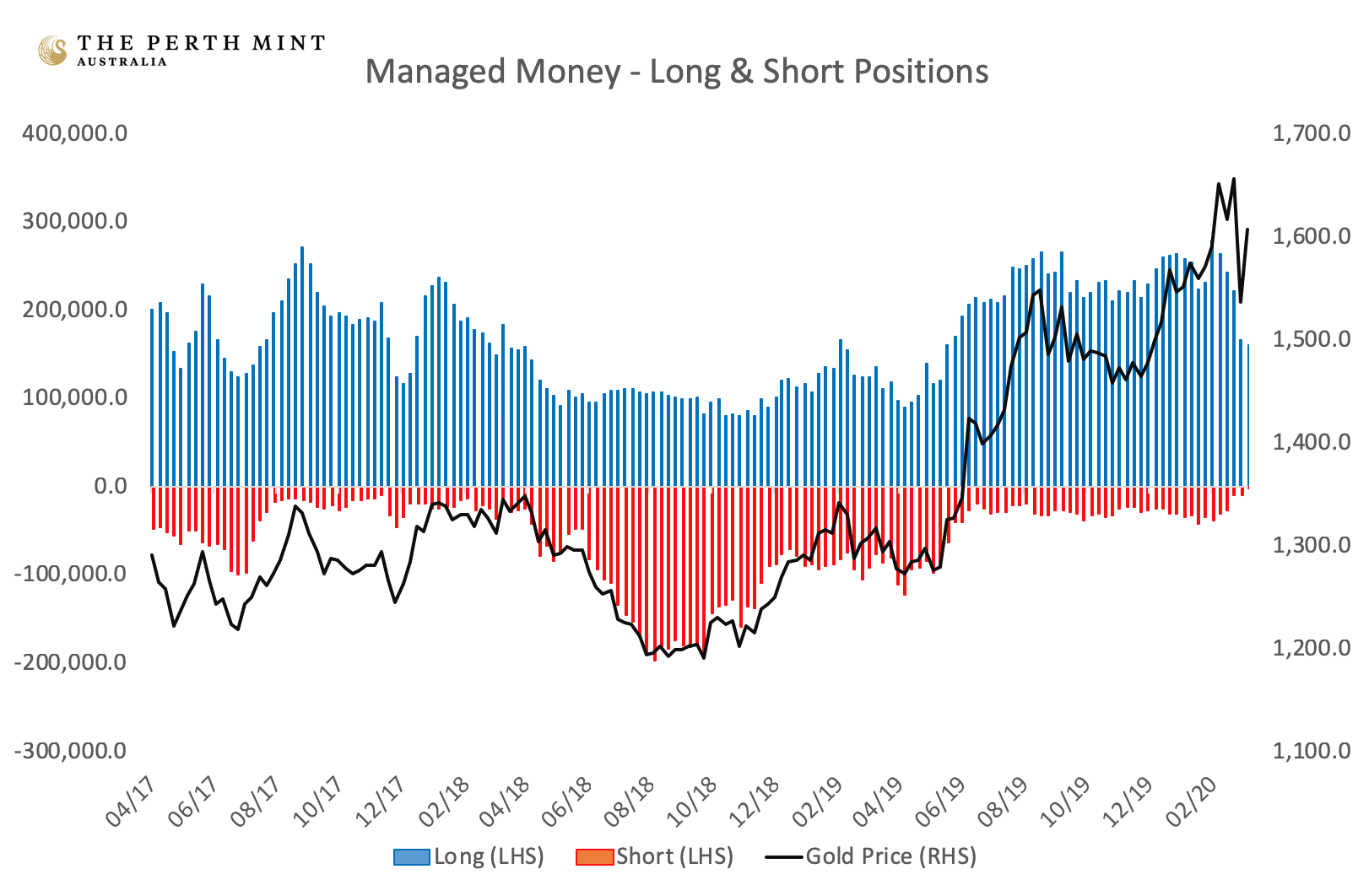

Managed money speculators have also cut their gross long positions by more than 40% since mid-February 2020, meaning substantial froth has come out of the market in the past six weeks. The importance of this sector of the market can be seen in the chart below, which plots managed money gross long and gross short positions from late 2017 to today.

Source: The Perth Mint, CFTC

The chart highlights the large build up in managed money long positions, and the complete unwind of managed money short positions between September 2018 and February 2020, with this activity playing a key role in the gold rally over this time period.

The other factor which will impact gold in the coming quarters is the performance of equity markets. Coming off one of the worst quarters on record, one would not be surprised to see a rally, especially given the sheer scale of monetary and fiscal stimulus being deployed across the G20. Indeed, some equity markets already rallied almost 20% in late March.

Against this, investors need to bear in mind that whilst equity markets are cheaper, they are hardly cheap. It seems like a lifetime, rather than a month ago that this article was posted on Livewire warning about historically high price to earnings and price to sales ratios.

The crash in the equity market has driven these ratios down, but one suspects the denominator for both ratios (earnings and sales) has a long way to fall in the coming quarters, with some earnings predicting double digit declines. Many listed companies are also openly stating that they’ll no longer engage in buybacks, a process which has provided a huge boost to earnings ‘growth’ over the last decade.

There is also the question of whether or not we will see a V, a U or an L shaped economic recovery once the threat of coronavirus has been sufficiently contained. Given no one can determine when a proper recovery can even begin, nor how much monetary and fiscal largesse will be required to keep economies on life support, the jury is still well and truly out in this regard.

Longer term outlook

Beyond the short-term drivers, there are a handful of key reasons investors continue to turn toward gold, five of which are explored in The Perth Mint’s newly released whitepaper: The benefits of gold as a strategic asset for SMSF trustees.

The five key reasons to own gold include:

- Strong long-term returns: Gold has delivered long-term returns of approximately 9% in AUD terms since the 1970s.

- Outperformance in low real-rate environments: Gold priced in AUD has delivered annual average gains of just over 20% (nominal) in years where real interest rates are 2% or lower.

- Outperformance in periods of equity market weakness: Gold has on average outperformed bonds and cash in months, quarters and years where equity markets deliver negative returns.

- Foreign currency exposure: Gold priced in Australian dollars will benefit from any fall in the value of the local currency.

- Simple, low cost and liquid: Gold is one of the most liquid asset classes on the planet and can be stored at rates that are cheaper than the average ETF.

After Q1 2020, gold’s ability to outperform during periods of equity market turbulence will be front of mind for most investors. Going forward, the two most relevant factors we expect to drive demand is the simplicity, liquidity and cost effectiveness of gold, and its track record of strong returns when real cash rates are low.

As Q2 2020 begins, bond markets are telling us that we are going to see negative real interest rates all the way out to 2050 in the United States (assuming inflation doesn’t fall further, which in itself will pose a challenge to financial markets), with the 30 year US Treasury ending March with a yield of just 1.35%.

No matter which way bond markets move from here, one can see gold getting a bid. If rates head higher, then risk assets will come under pressure (as will the real economy) and gold will find favour as a safe haven, as it has in Q1 2020. By definition bond portfolios would see mark-to-market losses in such an environment, encouraging investors to broaden the range of defensive assets in their portfolio.

If rates remain low, or indeed head lower, then more investors will seek an allocation to the yellow metal, preferring to speculate on the potential for gold to deliver strong capital gains in the monetary environment we find ourselves in, as it has in the past.

Gold’s simplicity, liquidity and cost-effectiveness should also continue to help it find favour amongst investors going forward. Unlike many alternative assets (private equity, unlisted infrastructure and property etc), gold is easy to get into and out of on a daily basis, with daily liquidity that is comfortably in excess of USD 100 billion.

This is a factor that is relevant to all investors, from younger Australians starting out on their investment journey through to SMSF trustees. Indeed, it also applies to institutional wealth managers who may need to reconsider the liquidity profile of their alternative assets in light of the coronavirus crisis, and the new rules regarding member access to superannuation assets.

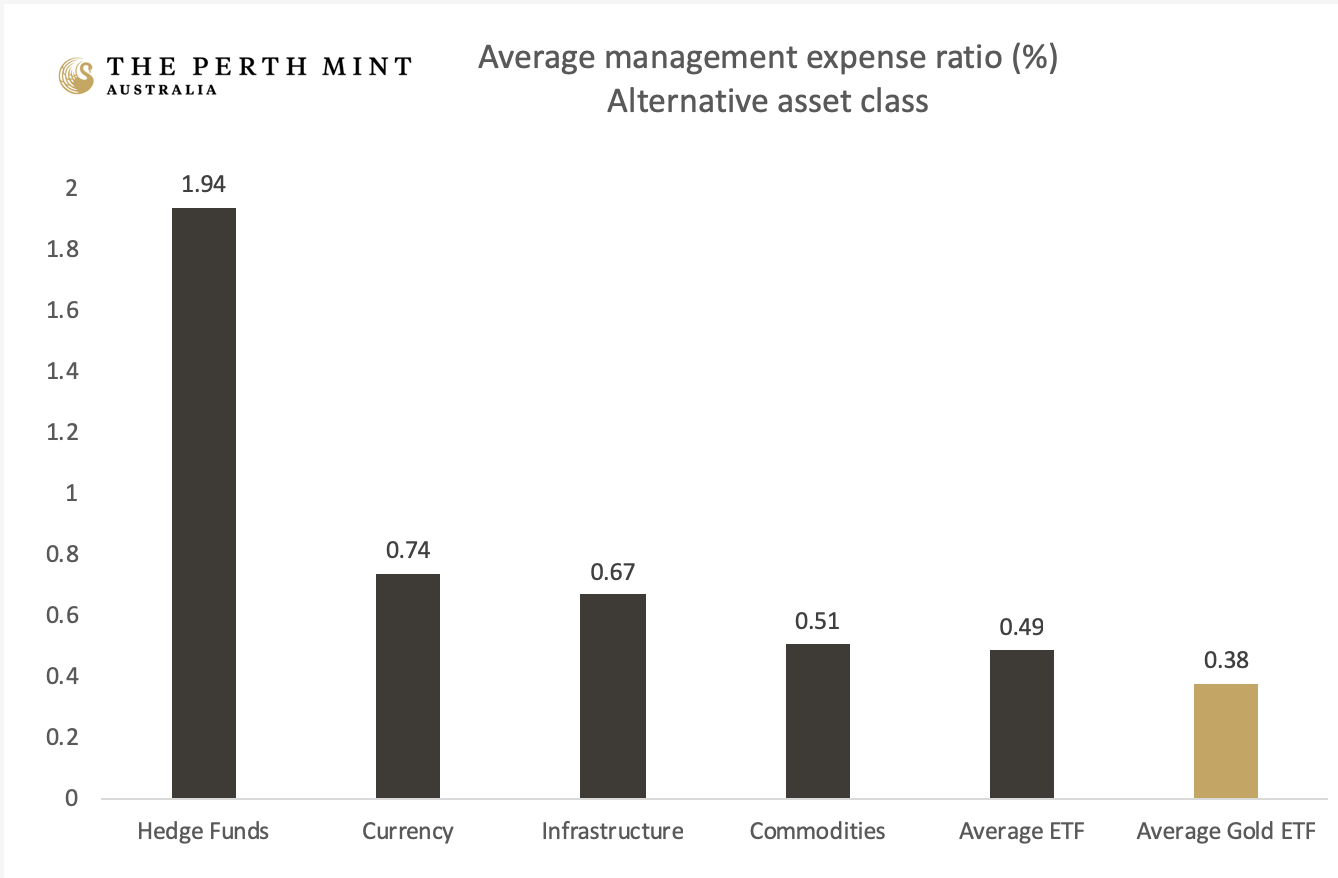

From a cost perspective, gold also wins hands down relative to most alternative assets. The following chart highlights the average management expense ratio (MER) for a variety of alternative asset classes available in ETF form via the ASX, as well as the average cost of investing in hedge funds.

The chart draws attention to the fact that at 0.38%, the average MER for listed gold products is lower than the average cost for ETF products as a whole, and substantially cheaper than other alternative assets investors can access.

This is obviously beneficial to the end investor who will get to keep more of the return generated by gold for themselves, rather than paying it away in product fees.

For a more detailed read on the reasons investors are turning to gold, you can access the full whitepaper at this link

Jordan Eliseo

Senior Investment Manager

The Perth Mint

3 April 2020

Disclaimer

Past performance does not guarantee future results.

The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in gold and the causes of the GFC. Lover of markets, competition & technology

.jpg)

4 topics

.jpg)

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in...

Expertise

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in...

Expertise

Comments

Comments

Sign In or Join Free to comment