Which superannuation funds may be affected by the ALP Franking Credit Proposal

The ALP proposal to limit refunding of franking credits will clearly impact pension phase self-managed superannuation funds (SMSFs). We believe it has the potential to impact many other superannuation funds. In this paper we build a model of the key variables which determine whether a superannuation fund is likely to lose refunds of net franking credits under the ALP proposal. Our model is consistent with and helps explain an article in The Australian which reported that $309m in franking credit refunds were paid to over 2000 APRA regulated superannuation funds, including 50 (out of a total of 240) large APRA funds, in 2015-16, impacting 2.6m member accounts.

The ALP proposal

On March 13 the ALP announced a proposal to abolish the net refunding of franking credits to Australian investors other than for charities and endowments which would be exempted from the proposal. The initial proposal was expected to impact 1.17m individuals and superannuation funds and generate $59B in government savings over 10 years.

On March 26 2018, the ALP revised their proposal in the light of significant public criticism of the initial proposal. Direct investments by pensioners (part and full on aged, disability and other Centrelink pensions) were excluded from the no franking credit refund regime. This exclusion means that 306,000 individuals on pensions will continue to receive franking credits on investments in Australian shares and partly offsets the criticism that this proposal impacts many battlers. SMSFs are also exempt from the no refund rule if they had at least one pensioner or allowance recipient member before March 28 2018, but we understand this exemption only applies to SMSFs, and not to other superannuation funds.

Which super funds are affected?

The proposal looks to abolish the net refunding of franking credits, but franking credits themselves are not abolished. Australian investors can continue to use franking credits to offset income tax payable and for a superannuation fund, contributions tax payable.

Whilst the ALP believes the main superannuation funds impacted by this proposal will be pension phase SMSFs, ATO taxation data (as quoted in The Australian) and analysis of APRA statistics show that many APRA regulated funds will likely also be impacted. This implies the impact of this proposal may be far broader than initially predicted (1.17m individuals).

To better understand which superannuation funds may be affected we built a superannuation tax model under which we undertake sensitivity analysis of the key drivers to losing franking credit refunds and their potential magnitude. Franking credits will be lost if total tax payable by a superannuation fund is less than franking credits received. Tax payable by a superannuation fund is a function of tax on investment earnings on the accumulation portion of a fund, as well as contributions tax payable on normal contributions. The percentage of pension phase assets, the level of taxable earnings and the level of contributions will vary from fund to fund and may vary from year to year. For example, taxable investment earnings will be largely determined by the state of investment markets. The level of franking credits can also vary between funds and over time. We base our estimate of the typical impact of imputation assuming an average SMSF exposure to Australian shares based on March 2018 ATO statistics of 31%, and the franking credit yield of the S&P/ASX200 Index which has averaged approximately 1.5% pa over the 10 years to December 2017. Investors with higher allocations to Australian shares, or allocations to higher yielding Australian shares could earn even higher levels of franking credits and would thus stand to lose more if franking credit refunds are denied. In our sensitivity analysis we double the level of franking credits in our high franking scenario.

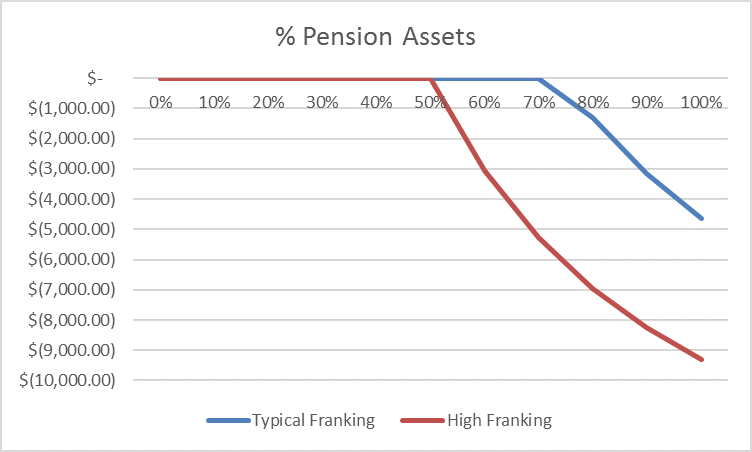

We then varied the proportion of a superannuation fund devoted to pension and accumulation as well as the levels of franking credits, contributions tax and taxable income . Figure 1 illustrates the outcome of our sensitivity analysis varying the proportion of pension assets and the level of franking credits. Clearly funds with 100% pension assets will lose all their franking credits assuming they are not subject to the pensioner exemption for SMSFs. We estimate that for a typical level of franking credits, funds with 70% or less in pension assets should not expect to lose franking credits. For funds with double the typical level of franking credits this number drops to 50%.

If accumulation phase (or 15% taxed) members aren’t paying contributions and therefore aren’t paying contributions tax, funds are more likely to lose franking credits, whilst funds with higher levels of taxable income would be less likely to lose franking credits. Higher levels of taxable income are usually associated with strong markets and/or the realization of capital gains.

Figure 1. Sensitivity analysis of the impact of non-refund of franking credits for superannuation funds expressed as $ annual cost on $1m pension balance

Source: Plato

We also note that the number of funds impacted will likely vary from year to year in response to the level of investment returns. When investment returns are very low or negative, tax on investment earnings will also be low, increasing the chance that the value of franking credits received by a fund exceeds tax payable. Accordingly, when investment returns are low, a higher percentage of superannuation funds may miss out on some or all of their franking credits, exacerbating the low investment returns.

Summary and Discussion

In this paper we have developed a model to predict the likely superannuation funds which may lose franking credits should the ALP’s proposal to limit the refunding of net franking credits be implemented in its current form. This model suggests that it is not just pension phase SMSFs which will be impacted by the ALP proposal. We find that the loss of franking credits is likely to positively related to:

1) The percentage of assets in pension, with maximum loss at 100% pension assets, but losses starting to occur from 50% to 70% pension assets; and

2) The level of franking credits generated by the underlying assets (the more franking credits generated the more likely you are to lose some);

and negatively related to:

3) The level of taxable income generated from the underlying assets (with losses in franking credits more likely in periods of weak investment markets/weak taxable income meaning investors may likely receive a double hit to returns); and

4) The level of contributions/contributions tax payable by accumulation members (the less contributions tax payable the more likely a fund loses franking credits).

Our model explains why The Australian reported that 50 large APRA regulated superannuation funds (out of 240) received net refunds of franking credits in the 2015/16 tax year. Our model finds that any relatively mature superannuation fund, where maturity is defined by the percentage of member balances in pension mode, may be in a net franking credit refund position.

Whilst many SMSF members have been vocal critics of this proposal, we believe members of other superannuation funds probably don’t even know they receive franking credit refunds (they are not reported on investment summaries) and probably won’t know whether they might miss out on franking credits should this proposal be enacted. We suggest these members or their advisors should ask – would my superannuation fund lose net franking credit refunds?

Finally, we believe that as the superannuation industry matures as a whole, as more and more members of superannuation funds migrate to pension status, the loss of franking credit refunds will impact a growing number of superannuants, be they members of government, industry, retail or SMSFs. As such we believe this proposal may represent a ticking time bomb for the whole superannuation industry.

Looking for income specialists?

Find out more at the Plato Investment Management website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006.

Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street Global Advisors, responsible for over $10B in active and enhanced equity investments. Earlier he held various positions at Westpac Investment Management, including Chief Investment Officer, Head of Equities. During his time at Westpac he was also instrumentally involved in the mergers of BT and Rothschild.

Don has a strong interest in responsible investment and governance. He has a PhD in Finance and a Bachelor of Commerce with First Class Honours from UQ, and a University Medal.

2 topics

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Comments

Comments

Sign In or Join Free to comment