Why are Australian bank ratings under pressure?

Earlier this week, Standard & Poor's (S&P) placed the entire Australian banking system on Negative Outlook. This implies that there is a one-in-three chance 25 Australian Banks' credit ratings may be downgraded within the next 2 years. S&P cited the continuing strength in property prices increases the risk of a sharp correction. This combined with record household debt could lead to widespread credit losses in the banking system. But it’s worth putting into perspective these risks in the context of the strength in bank balance sheets and trends in lending indicators where owner-occupier and investor credit growth has moderated as a result of tighter lending standards and macro-prudential policies.

UBS Asset Management

UBS Asset Management

We also note the following:

- Bank capital levels are solid and are likely to be further strengthened;

- Non-performing loans and arrears – despite increasing moderately in the last 18 months – are still below historical averages and compared to global peers;

- The risk profile of new borrowers has improved materially where the share of new high loan-to-valuation (LVR) lending and interest-only loans has fallen, 80%+ LVR lending is now at its lowest share in almost a decade

- Dynamic LVR is now around 50%, and mortgagees are reported to be around 2.5 years ahead on mortgage repayments on average.

House price growth nationwide has slowed compared to last year, and although Sydney and Melbourne have bucked the trend recently, new apartment supply is projected to catch up to demand over coming years. On the other hand, anecdotally there is still a sense of 'fear of missing out,' particularly with the younger generation where housing affordability will remain a significant challenge. Investor lending, now subject to an APRA imposed 10% growth limit, had initially weakened but is now seeing a bit of an uptick. This would make sense with Net Interest Margins and equity returns under pressure and NAB and ANZ refocussing efforts back into the domestic market, creating an intensely competitive environment.

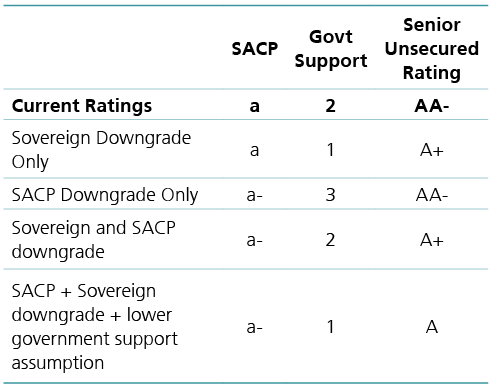

This week’s announcement nonetheless adds to the increasing threats to the major banks’ credit ratings as there are now three potential sources for downgrades:

- Stand-Alone Credit Profile (SACP) downgrade: this refers to bank ratings without upward notches for government support. Strictly speaking, the announcement this week relates to a negative outlook on the banks’ SACP’s;

- Sovereign downgrade: we think this is the most immediate and likely catalyst for a downgrade, though largely still uncertain and predicated on the Commonwealth budget being placed on a 'sustainable' path to balance; and

- Reassessment of government support: there is the potential for S&P to reassess the assumption from ‘highly likely’ to just ‘moderately likely’ in the next couple of years. This could arise if APRA introduces a Total Loss-Absorbing Capacity (TLAC) framework*, similar to that of other jurisdictions, where certain classes of creditors can be bailed-in, reducing the need for a government bail-out.

We can arrive at different S&P rating outcomes for the major banks depending on which combination of events are triggered:

A sovereign downgrade will result in a downgrade of the major banks' senior unsecured ratings. According to S&P's ratings methodology, a downgrade of the major banks’ SACP’s will not by itself result in a downgrade of senior unsecured ratings, but a combination of this and a sovereign downgrade will. If all three events are triggered, the result will be a two-notch downgrade. Clearly, this is the worst case and most uncertain scenario, and while we currently assign a low probability of it happening, there are numerous moving parts, including how the Australian TLAC framework takes shape and the amount and type of capital the banks raise in response to it and how quickly they raise it.

Written by Earl San Juan, Credit Analyst at UBS: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity investment capabilities that can also be combined into multi-asset strategies.

2 topics

6 stocks mentioned

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets