TOL - 10th Dec, 2020

Why ASX hybrids are likely to perform strongly

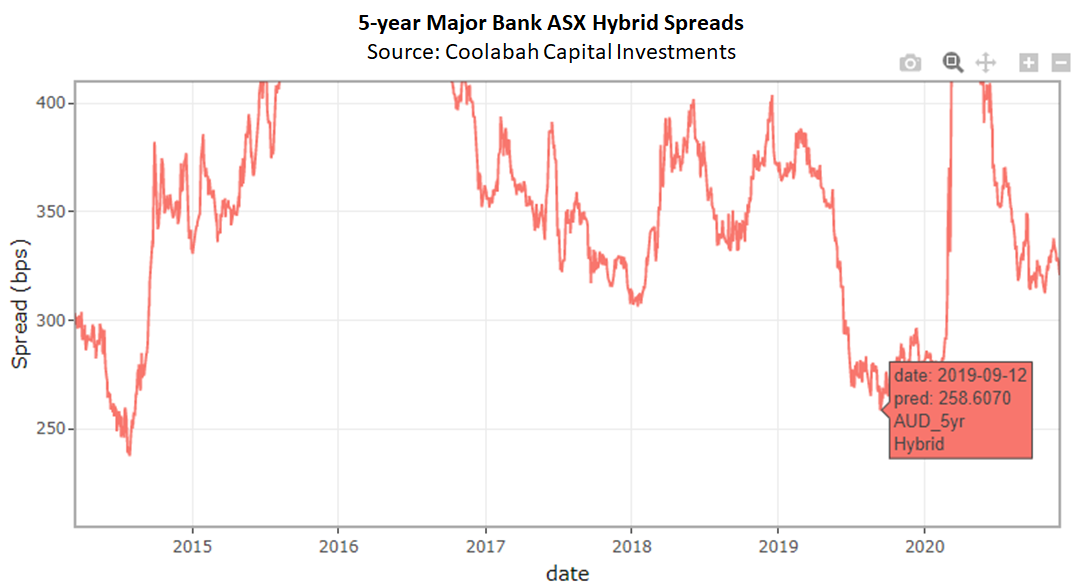

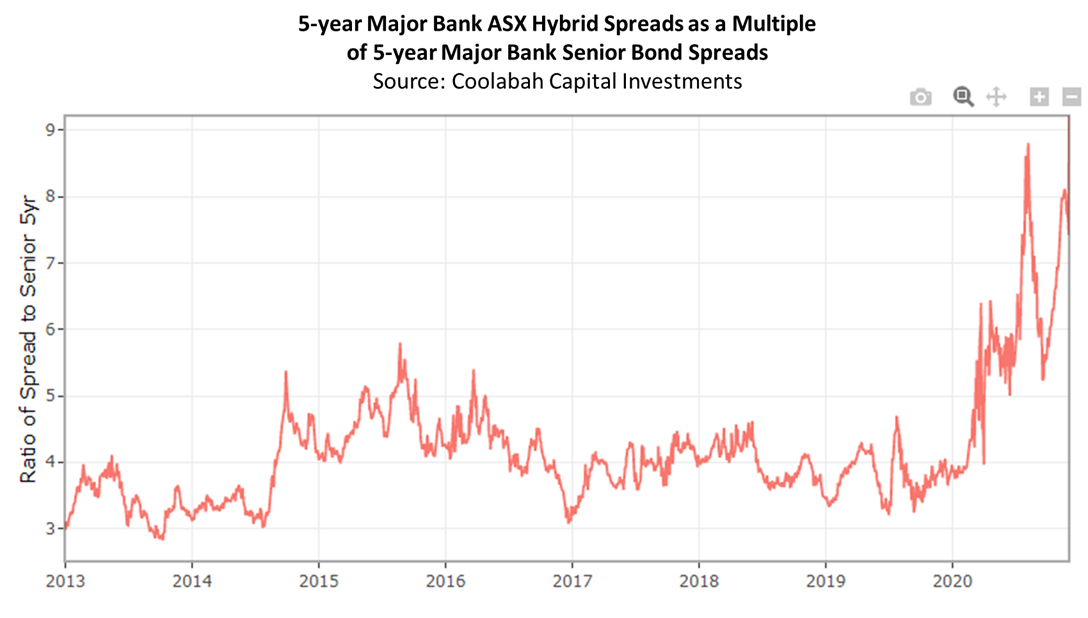

The major banks’ ASX hybrids are expected to perform strongly in the period ahead as their credit spreads compress back to pre-COVID levels and we move past a torrent of recent new supply with no less than five deals having priced on the market.

Ying Yi Ann Cheng, Portfolio Management Director at Coolabah Capital Investments, which manages $4.7 billion in assets, says 5-year major bank hybrid spreads blew-out to around 3.4% above the quarterly bank bill swap rate in November as a flood of new issues from Bendigo, Bank of Queensland, Challenger, Westpac, and NAB came to market.

“Pre-COVID, 5-year major bank hybrid spreads were around 2.6% above the bank bill swap rate. This implies potential capital gains of more than 3.3% if credit spreads mean-revert back to pre-COVID levels.”

The two images below from Coolabah below show major bank hybrid credit spreads over time and relative to major bank senior bond spreads.

Another sector that Cheng says Coolabah likes is the AA rated state government bond market, which is benefiting from the RBA’s quantitative easing (QE) program where the central bank is actively buying these bonds. Coolabah expects the RBA to extend its QE program next year as it seeks to continue to reduce Australia’s jobless rate to below 4% in an effort to boost otherwise anaemic wages growth.

Learn more about Coolabah Capital Investments

Coolabah Capital Investments (CCI) is a leading active fixed income manager, specialising in liquid, high grade credit. Click here for more information about Coolabah's income generating investment strategies.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Featuring

Ying Yi Ann Cheng,

Coolabah Capital

Ying Yi joined Coolabah Capital in 2017 as a full-time portfolio management director and market technicals analyst focussing on market research, analysis and technical factors, while also assuming responsibility for external stakeholder management. She spent the majority of her career at Citibank in London, where she was a Vice President, specialising in G10 and Emerging Market currencies, advising hedge fund clients and sovereign asset managers on alpha-generating and risk management strategies. She was most recently at RBC Capital Markets working within fixed-income and credit. Prior to the sell side, Ying Yi had interned at Colonial First State and PwC in various quantitative roles.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 stocks mentioned

1 contributor mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management