Why CSL is cheaper than you think

Investors have had to pay up for defensive stocks including healthcare stalwart CSL in recent times, but there's a solid supporting argument for this price premium.

While investors near-universally agree that CSL is a very high-quality business, when it comes to price, the agreement stops. Some claim the biotech company is too expensive; others say it's fairly valued, and some say the price is irrelevant.

Following another outstanding result yesterday, David Moberley from Paradice Investment Management believes investors focusing on the headline PE ratio are being misled by a quirk of accounting. Moberley believes this inflated figure effectively assigns a $30 billion-dollar negative value to the company's research and development (R&D) pipeline - which he thinks is a mistake.

How long have you held CSL?

CSL has been a long term holding our portfolios. Five or more years.

What attracted you to the company?

We think CSL is one of the highest quality businesses in the market. It is a global leader with scale advantages, an excellent management team, strong cashflows and a conservative balance sheet. The business has a significant runway of growth and can invest significant sums at very high returns.

It's the one of the few companies we’ve met that has a five- to 10-year planning cycle. That is why I think the management of the business is just phenomenal.

Whenever we think we’ve come up with a risk for the business and call the management team to talk about it, they’ll turn around and say, "Oh yeah, that's fine. We were thinking about this three years ago. We've actually already planned for it and this is our primary, secondary, and tertiary contingency plans." It is a phenomenal business.

What were the key points of the recent result?

Management delivered net profit after tax 6% ahead of its prior guidance on a constant currency basis. This was slightly ahead of where consensus estimates were. The result was strong across the board. Not only strong growth in their key bioscience division, but also in the flu vaccine business. Cash flow was strong, despite the company continuing to invest in future growth opportunities. The balance sheet is conservative with net debt-to-EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortisation) running at about one and a half times.

The result for the flu business highlighted what a stunning turnaround they have been able to manage in that business. CSL acquired this business off Novartis for close to its asset backing about five years ago. It paid $275 million for a business that had a book value of about a billion dollars, and had to sustain a few years of losses while they fixed it up. Including capital expenditure, all up they spent about $800 million. That business just delivered $332 million of EBITDA. The quality of the management team and the focus on return on invested capital (ROIC) is a little bit underappreciated in my view, and I think what they have been able to deliver with flu is phenomenal. It should be commended for that.

Were there any surprises in the results?

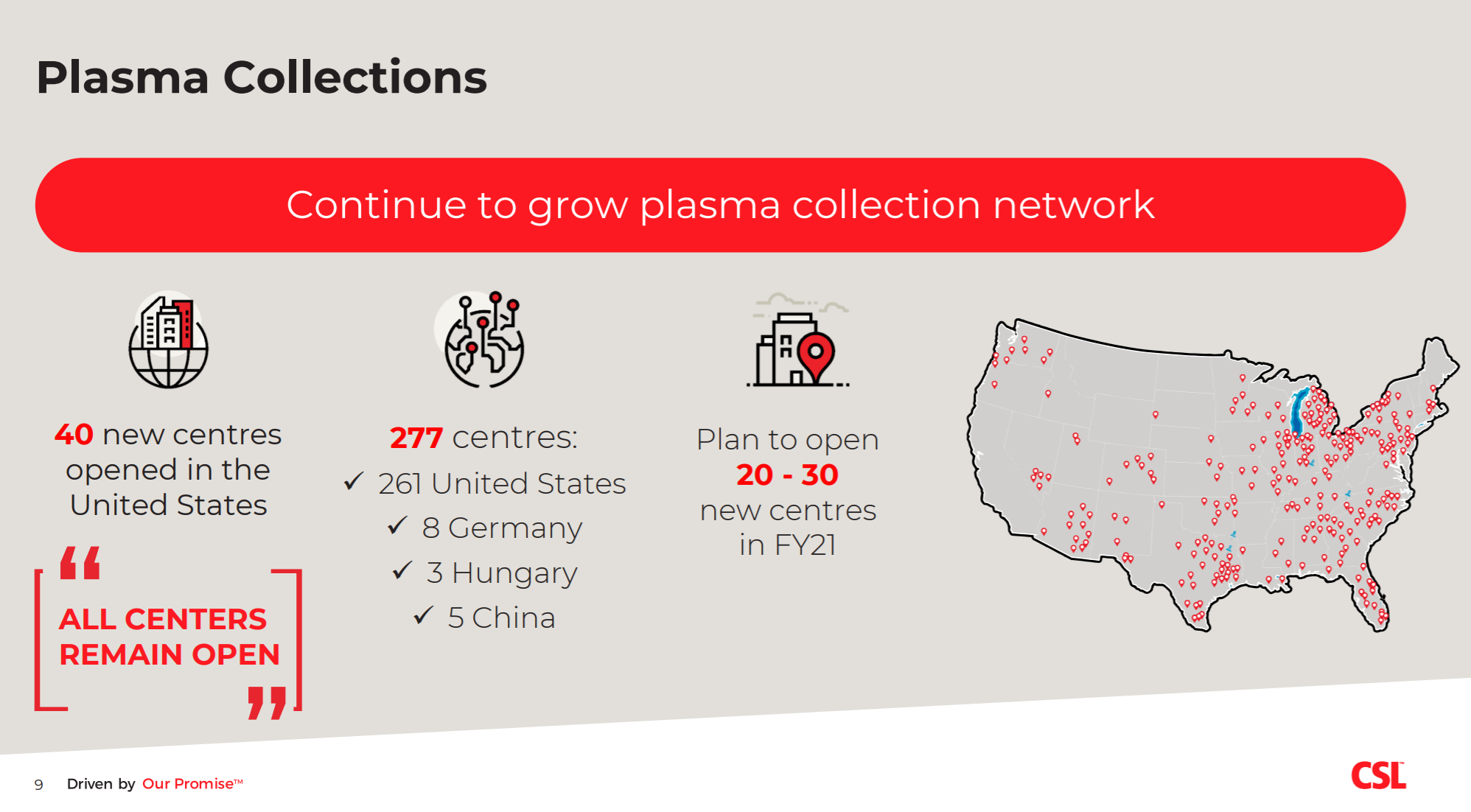

The big surprise in the result – and maybe this is why the stock was so strong on the day – was really around the outlook commentary. The stock had been sold off in the last three months leading into the result, and this is largely because of concerns around the supply of plasma and the collection centres in the US. These have been impacted by COVID-19 and have not had as many donations as they would have liked. This had meant that a lot of analysts had pulled back their forecasts for earnings expectations into '21.

Not only was FY20 strong, but the outlook commentary highlighted there'd been improvement in collections in July.

The company also outlined several options that could help mitigate some of these supply headwinds in the short term.

Source: CSL company presentation

Source: CSL company presentationOn top of that, management's guidance suggests they will be able to continue to deliver solid growth. Given how early this guidance has been put out, particularly with the uncertainty in the market, I think it was it taken as being quite conservative.

A lot of investors view CSL as being expensive. Could you explain why you see it as offering good value?

I think looking at headline PE for any company is overly simplistic. CSL spends around a billion dollars in R&D at the moment. Your bottom-line profit is being suppressed by a billion dollars of investment.

If you value that at the headline PE, you're saying that that R&D pipeline is worth roughly -$30 billion, which is clearly not the right way of thinking about it. Typically, CSL's been able to deliver very strong returns on that R&D, and the business runs a ROIC of around say mid 20%.

There's clearly a huge amount of value in that pipeline and I think the way we prefer to look at a business is to value each of the separate businesses individually and then we actually add on a component to that R&D pipeline. Given they are a dominant global leader with great scale advantages, strong growth outlook and an under-geared balance sheet, I can't see why the stock wouldn't continue to trade at a significant premium to the market.

Does CSL expense all its R&D in year one?

Yeah, that $922 million is what is being expensed through the P&L. If you're looking through a company's profit and loss statement and their earnings is being suppressed by the fact that they're investing a billion dollars to support future growth, then I think just valuing that part of the business at the headline multiple is obviously not the right way of doing it. For us, we prefer to look at that R&D pipeline separately.

Is there anything in that R&D pipeline that you’re particularly interested in?

Yes, there's a trial that they're running called CSL112. It's a potentially company changing drug. CSL112 is designed to remove cholesterol from plaques in the arteries which can lead to heart attacks or stroke events. The company is currently part way through a phase 3 trial, fully funded and expensed by themselves.

This product has a large market opportunity with a high unmet need. If the product is proven it could end up generating revenue up to a third of the current immunoglobulin business at very high margin. There is additional value created if this product is successful driven by the last litre economics of the fractionation process, that is to say, this product can be manufactured out of the existing raw materials driving margin up for the overall business.

I also think the company's work around COVID is interesting. CSL is collaborating with the University of Queensland for a vaccine candidate. It's also working on a number of treatment options for COVID, including the use of using antibodies from recovered patients.

Source: CSL company presentation

Source: CSL company presentationWant more earnings season Q&As like this?

Hit like so we know that you want more of this type of content.

Throughout August, my colleagues Bella Kidman, James Marlay, Vishal Teckchandani and Glenn Freeman will also publish similar Q&As on Livewire readers' most-tipped big caps and small caps. Hit FOLLOW on our profiles to be notified when these wires are published.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

........

This material has been prepared or contributed to by Paradice Investment Management Pty Ltd (ABN 64 090 148 619, AFSL No. 224158) (“Paradice”). This material (or any contribution to it) is not intended to constitute advertising or advice (including legal, tax or investment advice) of any kind. It is of a general nature only and has been prepared or provided on the understanding that Paradice is not providing professional advice on a particular matter. The information and opinions contained herein are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Before relying on the material or making any decision in relation to the funds, you should consider your needs and objectives, consult with a licensed financial adviser and obtain a copy of the relevant product disclosure statement, which is available by visiting www.paradice.com. Past performance is not a reliable indicator of future performance. The value of an investment in the funds may rise or fall. Returns are not guaranteed by any person.

1 topic

1 stock mentioned

3 contributors mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment