Why we think healthcare will continue to run

Healthcare stocks experienced both highs and lows in 2020, with the sector declining in March as the COVID-19 pandemic took hold, then rallying as the biopharmaceutical industry mobilized to combat the virus. The sector pulled back again on U.S. election uncertainty, only to rebound following promising data for COVID-19 vaccines and a more benign election outcome. Now heading into 2021, we believe this upward momentum could have staying power.

Innovation opens new markets

For one, biopharma’s response to COVID-19 has cast a spotlight on the industry’s innovative might. So far, two vaccines – one from Moderna and another jointly developed by BioNTech and Pfizer – have shown to be roughly 95% effective in preventing symptomatic disease in late-stage clinical trials. A third vaccine from AstraZeneca and the University of Oxford could be as much as 90% effective. Even more impressive, the Moderna and BioNTech/Pfizer vaccines use novel messenger RNA (mRNA) technology, and all three vaccines were developed in under a year (compared to historical vaccine development of a decade or longer).

It remains to be seen how much these and other vaccines can add sustainably to the bottom lines of their developers (nearly 50 vaccine candidates are in clinical trials). Even so, the industry’s push to address the COVID-19 crisis – with billions of dollars invested in research and manufacturing – has helped to accelerate and/or validate new technologies. mRNA therapy has been studied for indications such as cancer and infectious disease but, so far, has not earned regulatory approval.

The lessons learned from developing COVID-19 vaccines could be applied to mRNA programs for other vaccines as well as for a variety of cancers and other applications.

mRNA technology is just one example of the type of research now advancing in biopharma. Over the next few years, we expect to see data readouts for gene therapies addressing devastating diseases such as Duchenne muscular dystrophy, hemophilia and cystic fibrosis. We’re also seeing an explosion of cell-based medicines for cancer and rare diseases and precision oncology therapies that take a more targeted approach, including “guided missile” delivery of chemotherapy to tumor cells using antibody-drug conjugates. If successful, many of these medicines could revolutionize the standard of care for important disease categories and open new market opportunities.

The return of M&A

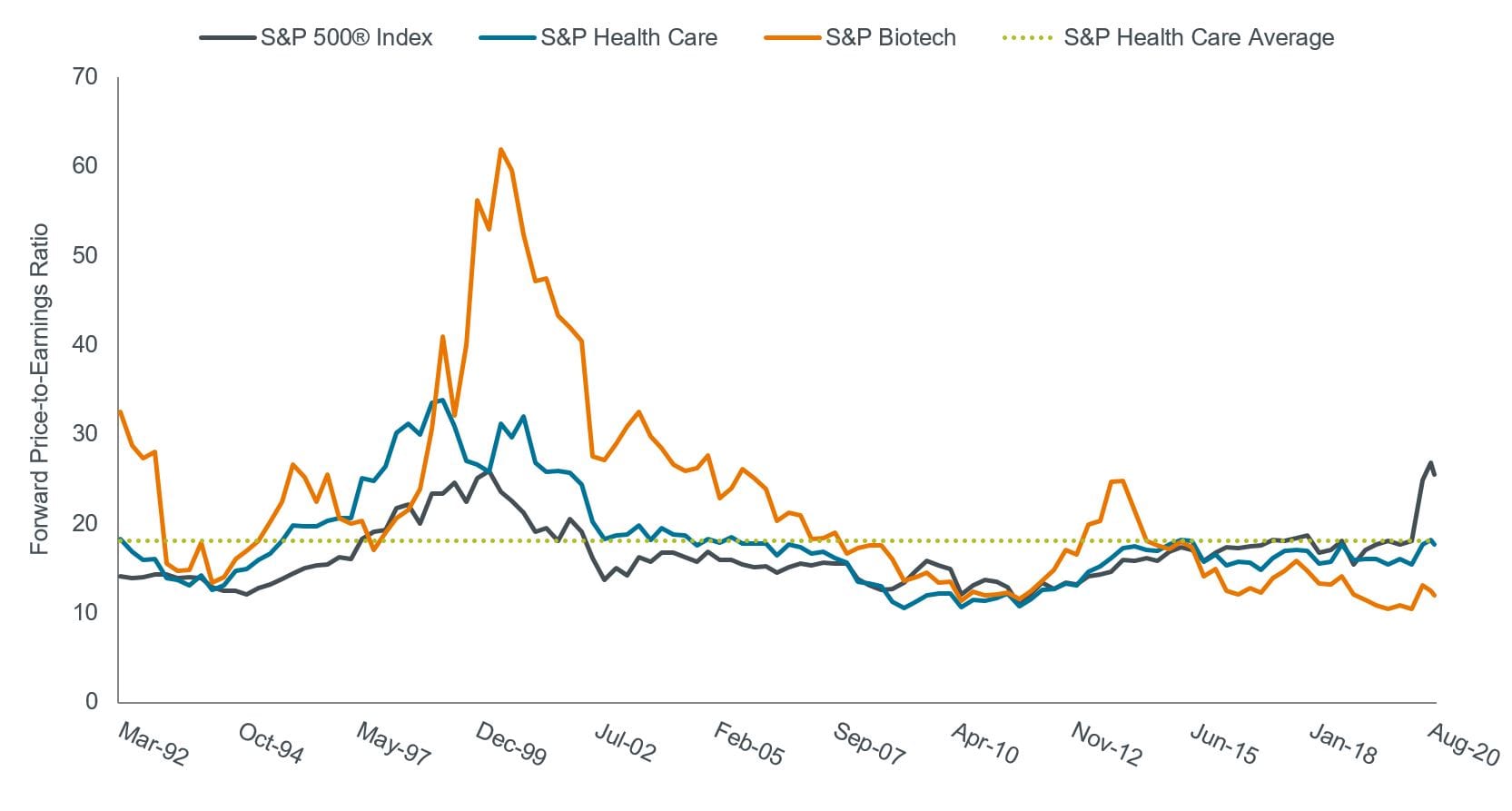

Even as these scientific advances are being made, the sector trades at a substantial discount to the broad market. We believe advancing science, attractive valuations and rock-bottom interest rates could lead to an uptick in merger and acquisition (M&A) activity, especially as many large-cap pharmaceutical and biotechnology firms suffer from aging drug franchises that face looming generic competition.

Healthcare at a discount

Source: Bloomberg, Janus Henderson Investors. Data are quarterly from 31 March 1992 to 30 September 2020. The S&P Health Care sector comprises those companies included in the S&P 500 that are classified as members of the GICS health care sector. S&P Biotech comprises stocks in the S&P Total Market Index that are classified in the GICS biotechnology sub-industry.

Policy risk wanes

The 2020 U.S. election outcome could also prove to benefit healthcare in the coming year. Unlike other Democratic candidates, President-elect Joe Biden has proposed only moderate changes to the U.S. healthcare system, such as expanding the Affordable Care Act (which could drive increased demand for medical care). At the same time, although the balance of power in the 100-seat Senate remains undecided thanks to two runoff races, at best, Democrats can achieve only a simple majority. As such, the Party’s ability to pass sweeping legislation will likely be limited since Senate procedural rules generally require 60 votes to close debate.

That’s not to say pressures for healthcare reform will completely dissipate. Drug pricing remains a focal point not just in Washington, D.C., but also in the private market. Amazon, for example, recently announced an online pharmacy with a new savings card program and free shipping for Prime members. But we believe initiatives that help improve price transparency in drug distribution and compete away fees that add to consumers’ out-of-pocket costs represent a positive development. In fact, while average net prices for prescription drugs have remained relatively flat in recent years, consumer out-of-pocket costs have continued to rise.

Addressing this imbalance could help protect incentives for innovation while improving patient affordability – a win-win, in our view.

Keep your portfolio in good health

Stay up to date with all of our latest insights by clicking the follow button below and you'll be notified every time we post an update on where we are finding the most compelling ideas from around the world.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andy Acker is a Portfolio Manager at Janus Henderson Investors responsible for managing the Global Life Sciences and Biotechnology strategies since 2007 and 2018, respectively. He also leads the firm’s Health Care Sector Research Team. Andy was assistant portfolio manager on the Global Life Sciences strategy from 2003 to 2007. He joined Janus in 1999 as a research analyst focused on companies in the biotechnology and pharmaceutical industries. Prior to this, he worked as a strategy consultant for the Boston Consulting Group and as a health care analyst for Morgan Stanley Venture Partners.

........

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

1 topic

Andy Acker is a Portfolio Manager at Janus Henderson Investors responsible for managing the Global Life Sciences and Biotechnology strategies since 2007 and 2018, respectively. He also leads the firm’s Health Care Sector Research Team. Andy was...

Expertise

Andy Acker is a Portfolio Manager at Janus Henderson Investors responsible for managing the Global Life Sciences and Biotechnology strategies since 2007 and 2018, respectively. He also leads the firm’s Health Care Sector Research Team. Andy was...

Expertise

Comments

Comments

Sign In or Join Free to comment