2020 Mid-Year Credit Outlook: Australia

Andrew Mayes

Remission or relapse? Inevitable pain for some as government support is unwound and forbearance runs out.

Global markets favour central banks, for now

There is no doubt this economic cycle is unprecedented. A health crisis evolving into an economic (credit) crisis on the back of government-mandated lockdowns. Unprecedented (and justified) levels of government spending - mainly in the form of income support to housebound and furloughed individuals - has probably prevented depression-like conditions.

With lawmakers understandably hesitant to pull the trigger on a second series of lockdowns, they now find themselves with a frighteningly difficult juggling act. Lockdowns and income substitution were incredibly effective the first time around; however, there is a limit to the latter, which then reduces the likelihood of the former.

Risk asset prices have rebounded strongly following a precipitous fall early in the year, with investor preference and central bank intervention favouring defensive assets.

Financial markets either expect a quicker recovery than what the real economy portends, or that central banks will continue to backstop financial markets until the real economy recovers. We would wager the latter.

A disconnect of sorts between financial markets and the evolution of the real economy has emerged (although it is not entirely unreasonable, as there are some who clearly benefit from changes to the way we go about our affairs), which could unsettle the former (and further setback the latter) if their risk appetite wanes.

RBA commits to historically low rates, so expect short-term yields to remain low for longer

Locally, conventional monetary policy has run its course. With the RBA affirming its commitment to maintaining three-year yields at the current level until progress is made toward full employment and inflation within the 2-3 percent target range, short-term rates are likely to remain anchored for at least the next 18-24 months, in our view.

Yields in the longer-end briefly widened on better than feared outcomes and as fiscal support placed upward pressure on term premiums, although this was quickly unwound as central banks globally intervened.

With government balance sheets set to expand further this year, we expect central banks will continue to step in to limit the yield curve steepening too aggressively (although this too will require further expansion of central bank balance sheets).

The RBA has also played down the prospects of negative interest rates, despite the recovery in the AUD in recent months. We don’t expect negative interest rates and would see little to be gained. Central banking is a relative game, however. Larger support programmes in other jurisdictions (particularly in the US and Europe) may overshadow the RBA’s support to date, which in-turn could leave the RBA with a need to be seen to do more.

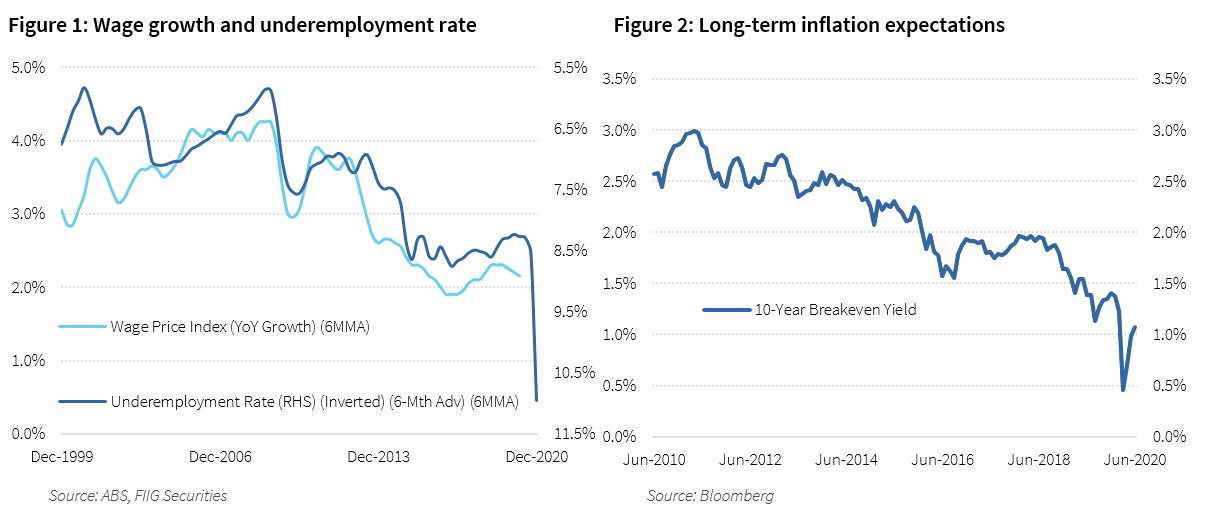

Outlook for wages and inflation fall as spare capacity rises

The inevitable question that arises from lower rates and an increase in the supply of money is whether you have the necessary conditions to trigger an increase in inflation. The question is whether such demand exists in this period of considerable and unprecedented uncertainty. We have previously argued recent monetary (and indeed fiscal) measures are likely to be less supplementary (stimulatory) and more of a substitute for the private sector as it navigates lower income and lower demand as hours worked collapses and spare capacity rises.

To date, credit has yet to respond to the increase in supply of money, and we see little to suggest that will change in the near term Despite a brief increase in credit demand from business at the outset of the pandemic, credit demand from households remains exhausted, which is of little surprise given very high levels of household debt, while their intention to save more in the near term seems clear.

Given considerable slack in the labour market - which will get worse before it gets better, in our view - as well as other impediments to stronger growth (including high levels of household debt and an imminent collapse in migration), we see inflation remain lower in the near term, even more so if the federal government declines the opportunity to extend income support beyond September 2020.

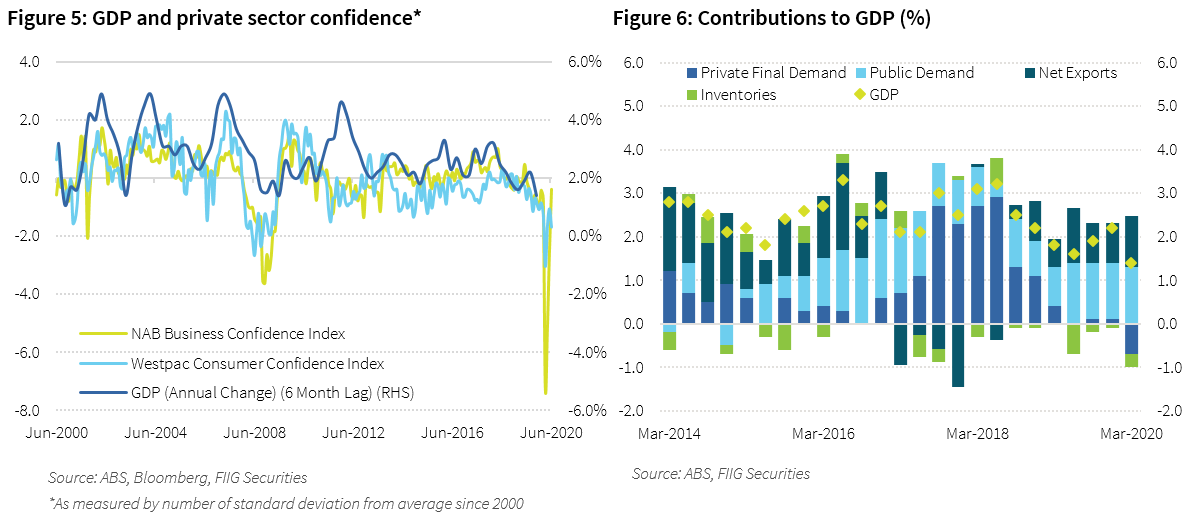

Sharp rebound in economic activity unlikely, although credit outlook improves for some sectors

Notwithstanding better than feared data more recently, significant uncertainty around the recovery in employment and demand is likely to weigh on the private sector for some time. Households and businesses remain overwhelmingly cautious, which clearly has implications for consumption and investment plans for the remainder of this year, as well as the overall health of the economy.

Australia’s private sector has been effectively in recession for the better part of twelve months, with government spending and exports the only bright spots. If the initial response from business to the pandemic was ensuring survival (access to capital and credit), the subsequent response as restrictions are eased will be rightsizing to fit a new economy. In other words, it is highly probable some jobs will simply not return. In reality, the government will have little choice in our view but to extend financial support to business (in particular) and households, as well as to push ahead with reform.

Beyond the obvious casualties (travel, tourism, education, and hospitality), uncertainty has evolved into caution, which will weigh on the outlook for a number of other sectors, including residential property, housing construction, and discretionary retail (consumption). By extension, commercial property also faces a similarly tough outlook, particularly for retail (short-term) and office (long-term), although industrial could be a beneficiary as the imposition of social distancing accelerates a shift toward online retail. The outlook for bulk commodities is mixed, with iron ore one of the first beneficiaries of a turn in risk sentiment, although a broader uptick in global demand will be a necessary precursor to stronger prices for energy-related commodities, including liquefied natural gas and thermal coal.

Fixed income considerations in the second half as virus concerns persist

With short-term interest rates expected to remain near zero for the foreseeable future, investors seeking higher returns will need to increase their exposure to credit or duration. We favour duration over credit, particularly given the uncertain outlook, although we wouldn’t completely discount credit. For example, if you are comfortable with the short-to-medium term viability of Australia’s major banks, as we are, then shifting from lower-yielding tier two instruments into higher-yielding hybrids may be something to explore.

By extension, we continue to emphasise higher quality credits, many of whom have strengthened their balance sheets in recent months. Liquidity in higher-rated credits will also benefit - directly or otherwise - from central bank support.

While the recent recovery in markets has reversed the sell-off at the beginning of the pandemic, opportunities will continue to present themselves, particularly as markets shift their focus toward prospects for the real economy.

For investors with a longer-term horizon and an appetite for increased risk, there are likely to be some compelling opportunities in high yield. Inflation-linked bonds should also provide a hedge in the (unlikely) event inflation rears its head in the near term.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

........

The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights.

FIIG Securities Limited (‘FIIG’) provides general financial product advice only. As a result, this document, and any information or advice, has been provided by FIIG without taking account of your objectives, financial situation and needs. Because of this, you should, before acting on any advice from FIIG, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If this document, or any advice, relates to the acquisition, or possible acquisition, of a particular financial product, you should obtain a product disclosure statement relating to the product and consider the statement before making any decision about whether to acquire the product. Neither FIIG, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice. FIIG, its staff and related parties earn fees and revenue from dealing in the securities as principal or otherwise and may have an interest in any securities mentioned in this document. Any reference to credit ratings of companies, entities or financial products must only be relied upon by a ‘wholesale client’ as that term is defined in section 761G of the Corporations Act 2001 (Cth). FIIG strongly recommends that you seek independent accounting, financial, taxation, and legal advice, tailored to your specific objectives, financial situation or needs, prior to making any investment decision. FIIG does not provide tax advice and is not a registered tax agent or tax (financial) advisor, nor are any of FIIG’s staff or authorised representatives. FIIG does not make a market in the securities or products that may be referred to in this document. A copy of FIIG’s current Financial Services Guide is available at www.fiig.com.au/fsg.

An investment in notes or corporate bonds should not be compared to a bank deposit. Notes and corporate bonds have a greater risk of loss of some or all of an investor’s capital when compared to bank deposits. Past performance of any product described on any communication from FIIG is not a reliable indication of future performance. Forecasts contained in this document are predictive in character and based on assumptions such as a 2.5% p.a. assumed rate of inflation, foreign exchange rates or forward interest rate curves generally available at the time and no reliance should be placed on the accuracy of any forecast information. The actual results may differ substantially from the forecasts and are subject to change without further notice. FIIG is not licensed to provide foreign exchange hedging or deal in foreign exchange contracts services. FIIG may quote to you an estimated yield when you purchase a bond. This yield may be calculated by FIIG on either A) a yield to maturity date basis; or B) a yield to early redemption date basis. Some bond issuances include multiple early redemption dates and prices, therefore the realised yield earned by you on the bond may differ from the yield estimated or quoted by FIIG at the time of your purchase. The information in this document is strictly confidential. If you are not the intended recipient of the information contained in this document, you may not disclose or use the information in any way. No liability is accepted for any unauthorised use of the information contained in this document. FIIG is the owner of the copyright material in this document unless otherwise specified.

5 topics

Andrew Mayes

Expertise

Andrew Mayes

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management