Timeless principles for building wealth

As investors, we are all looking for an edge in earning outsized returns. Here I identify 3 simple portfolio management principles that are essential in any investor’s toolkit, and briefly outline how they can all be brought together into a simple cohesive strategy.

1) Compound (Reinvest) your returns

Would you rather be given $10,000 immediately... or wait 12 months to receive $1,000 that has been earning 1% each day, compounded (reinvested)?

If you selected the second option, congratulations, you would be given close to $38,000.

This simple exercise highlights the vast difference between compounding (reinvesting) your returns and consuming (not reinvesting) your returns.

The key drivers of compounding interest

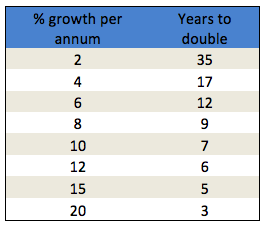

Mathematically, the key metrics that influence compounding returns are: a) the level of returns (%) and; b) the compounding frequency.

The profound wealth-building effects of a higher interest rate are neatly summarised in the table below.

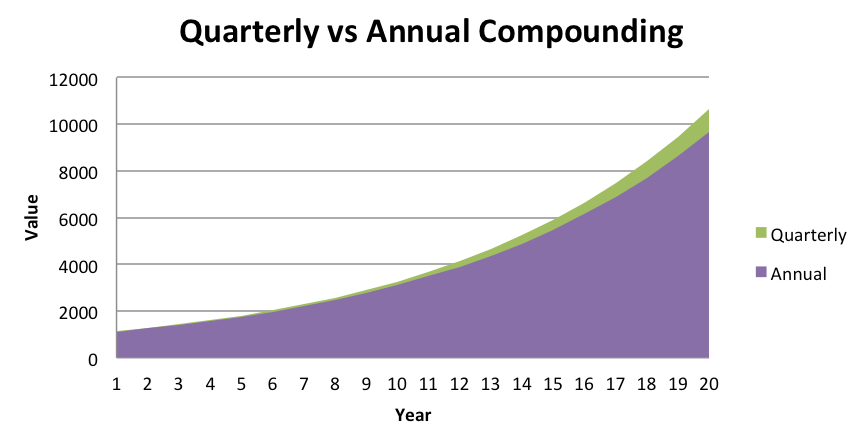

The effect of compounding frequency are illustrated by this example: Compare 2 funds which both earn 12% per annum, where fund A distributes once a year and Fund B distributes four times a year.

If the investor in fund B is able to reinvest the quarterly distribution, this leads to an extra relative return of almost 4% over Fund A; assuming the investor is able to earn the same incremental return on the reinvestments.

A simple way for investors to benefit using this principle is to reinvest your portfolio earnings, whilst giving thought to investing in assets that provide distributions or dividends at regular points during the year.

2) Avoiding losses - let winners run but cut losses quickly

Research has shown that most individuals are risk avoiders when handling gains, and risk takers when dealing with losses. Practically speaking, this means that individuals are more willing to speculatively hold a losing investment in the hope of the loss diminishing, than to hold a winning investment with the hope of further upside.

In a nutshell, this means that a person’s strategy for managing uncertainty will often clash with the strategy needed to objectively manage the risks in an investment situation. This leads to a negative asymmetric return, in the sense that investors tend to let their losses run while limiting their gains. Investors need to fight against this primordial, behavioural urge by cutting losses short and letting profitable trades run.

Limiting losses is the single largest factor in achieving sustainable returns. For example, a loss of 20% requires a gain of 25% to get back to even; whilst a 50% loss requires a 100% gain to breakeven. Conversely, by avoiding exposure to market losses, an investor can outperform the market without full exposure to the market's upside.

An allocation to non-equity asset classes should be explored to protect portfolio returns. Investors should think practically by focusing just as much on the downside just as much as the upside of an investment.

3) Reduce volatility

The ASX200 total return index (XJOA) has had a mean return of 9.7% per annum over the last 25 years, however, in just 3 of those years has the return fallen within 2% of this value.

When it comes to compounding returns, volatility has a detrimental effect due to negative compounding returns during certain periods. This impact is known as volatility drag. When comparing two investments with the same average returns but differing volatility, the higher volatility investment will exhibit a lower geometric (compounded) return, due to negative compounding over multiple periods.

If investors can utilise a strategy that can lower volatility without sacrificing too much return over time, it will likely lead to a better outcome. If investors cannot hold onto their investments through the volatility, they will never achieve the 'average' returns.

High volatility environments can often lead to poor decision making by investors. For example, selling in periods of despondency (the lows) and buying in periods of where confidence is high (the highs).

What can investors do to mitigate the effect of volatility in their portfolio? Structurally, investors are able to dampen portfolio volatility by investing across asset classes; for example in fixed interest, cash or alternatives.

Tying it all together

To conclude, we have demonstrated the benefits of reinvesting your returns, avoiding losses and reducing volatility in your portfolio.

We believe the ideal method of tying these 3 concepts together is utilising the power of a multi-asset portfolio to achieve consistent, sustainable returns.

We should all strive to achieve robust, sustainable returns, not ‘beat the market’. By diversifying their portfolios across asset classes or by utilising an investment manager who shares this philosophy, an investor has a far better chance of achieving a consistent, sustainable return that will build wealth year-on-year without the fear of volatility and potential losses.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Emanuel is the Principal of Datt Capital, a boutique Melbourne-based investment manager focused on identifying high growth and special situation opportunities.

5 topics

Emanuel is the Principal of Datt Capital, a boutique Melbourne-based investment manager focused on identifying high growth and special situation opportunities.

Expertise

Emanuel is the Principal of Datt Capital, a boutique Melbourne-based investment manager focused on identifying high growth and special situation opportunities.

Expertise

Comments

Comments

Sign In or Join Free to comment