9 keys to successful investing - and why they are more important than ever amid COVID

As an investor it’s very easy to get thrown off by the ever-present worry list surrounding investment markets that relates to economic activity, profits, interest rates, politics, etc. Or by the perennial predictions of an imminent crash. Or by talk of the next best thing that’s going to make you rich.

The investment world is far from predictable and neat. It’s well known for sucking investors in during the good times and spitting them out during the bad times. Investing has become more difficult in recent years reflecting a surge in the flow of information and opinion. This has been magnified by a digital media where everyone is vying for attention and the best way to get this attention is via headlines of impending crisis. This all adds to uncertainty and potentially erratic investment decisions.

Against this backdrop, I have written regularly over the years about nine key things for investors to bear in mind in order to be successful. But how does the coronavirus pandemic impact these? This note reviews each in view of the pandemic.

1. Make the most of the power of compound interest

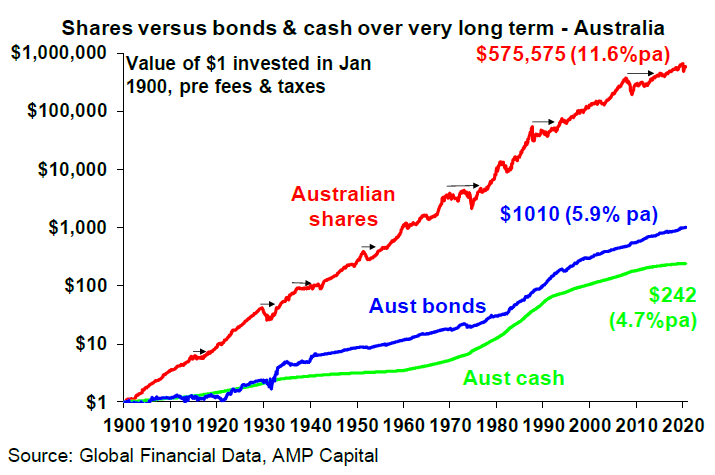

The next chart is one of my favourites and shows the value of one dollar invested in 1900 in Australian cash, bonds, and equities with interest and dividends reinvested along the way. That one dollar would be worth $242 today if it had been invested in cash.

But if it had been invested in bonds it would be worth $1010 and if it was allocated to Australian shares it would be worth $575,575. Although the average return on shares (11.6% pa) is just double that on bonds (5.9% pa), the magic of compounding higher returns over long periods leads to a substantially higher balance. The same applies to other growth assets like property.

So, the best way to build wealth is to take advantage of the power of compound interest and have a decent exposure to growth assets.

Of course, the price for higher returns is higher volatility but the impact of compounding higher returns from growth assets is huge over long periods.

The coronavirus pandemic does nothing to change this, any more than previous setbacks like WW1 and Spanish Flu, the Great Depression, the 1973-74 bear market, the 1987 crash or the GFC did. The collapse in interest rates and earnings yields means the returns seen over the last 120 years will likely be a lot lower over the next decade. But this partly reflects the collapse in inflation (so in real returns thangs are not quite so bad).

And without getting into forecasting, shares offering a dividend yield of 3.5% (4.5% with franking credits) should provide superior medium-term returns and hence grow wealth far better than bonds where the 10-year yield is 0.85% pa (which is the return you will get over the next ten years).

2. Don’t get thrown off by the cycle

Investment markets constantly go through cyclical phases of good times and bad. Some are short and sharp, some can spread over many years. But all eventually set up their own reversal – eg as falls make shares cheap and low interest rates help them rebound.

The trouble is that cycles can throw investors off a well thought out investment strategy that aims to take advantage of longer-term returns. But they also create opportunities. Looked at in a longer-term context the roughly 35% plunge and then rebound in shares associated with coronavirus was just another cyclical swing – albeit it occurred faster reflecting the unique nature of the shock which saw a faster than normal hit to economies and then faster than normal deployment of fiscal stimulus and monetary easing. The key was not to get thrown off when markets plunged into March.

3. Invest for the long term

Looking back, it always looks obvious as to why things happened. But that’s just Harry Hindsight talking! Looking forward no-one has a perfect crystal ball. As JK Galbraith observed, “there are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” Usually, the grander the forecast the greater the need for scepticism as such calls invariably get the timing wrong or are dead wrong.

If getting markets right were easy, then the prognosticators would be mega-rich and would have stopped doing it. Related to this many get it wrong by letting blind faith – eg “there is too much debt” – get in the way of good decisions. They may be right one day, but an investor can lose a lot of money in the interim.

The problem for ordinary investors is that it’s not getting easier as the world is getting noisier. This has all been evident through the coronavirus pandemic with all sorts of forecasts as to what it would mean, most of which provided little help in actually getting the market low back in March let alone the rebound.

Given the difficulty in getting market moves right in the short term, for most it’s best to get a long-term plan that suits your level of wealth, age, tolerance of volatility, etc, and stick to it.

4. Diversify

Don’t put all your eggs in one basket. Having a well-diversified portfolio will provide a much smoother ride. For example, global and Australian shares provide similar returns over the very long term but in the March quarter, this year global shares in Australian dollars fell less than half as much as Australian shares.

Similarly, income investors who just had a few Australian bank stocks would have been hard hit by bank dividend cuts earlier this year whereas those with a broader exposure to high dividend-paying companies would have seen their dividend income hold up a lot better.

5. Turn down the noise

After having worked out a strategy that’s right for you, it’s important to turn down the noise on the information flow and prognosticating babble and stay focussed. The trouble is that the digital world we live in is seeing an explosion in information and opinions about economies and investments. But much of this information and opinion is of poor quality. As “bad news sells” there has always been pressure on editors to put the negative news on the front page of newspapers but there was hopefully some balance in the rest of the paper.

But in a digital world each story can be tracked via clicks so the pressure to run with sensationalised and often bad news headlines is magnified. Hence clickbait. This has gone into hyperdrive through the coronavirus pandemic – with a massively stepped-up flow of economic information (eg the Australian Bureau of Statistics now publishes key jobs reports three times a month and there is now a focus on weekly economic statistics). This may be of use in providing timely information on how the economy is traveling but it’s also added immensely to the flow of information and often it's contradictory.

This is all leading to heightened uncertainty and shorter investment horizons which in turn can add to the risk that you could be thrown off well-thought-out investment strategies.

The key is to turn down the volume on all this noise. This also means keeping your investment strategy relatively simple. Don’t waste too much time on individual shares or funds as it’s your high-level asset allocation that will mainly drive the return and volatility you will get.

Here are several tips to help turn down the noise:

- Put the latest worries in context – the global and Australian economies have had plenty of worries over the last century or so – from wars to depressions to pandemics - and yet long-term investment returns have been fine

- Recognise that it's normal for markets to swing from one extreme to another;

- Focus on only a few reliable news services and turn all “notifications” on your smart device off.

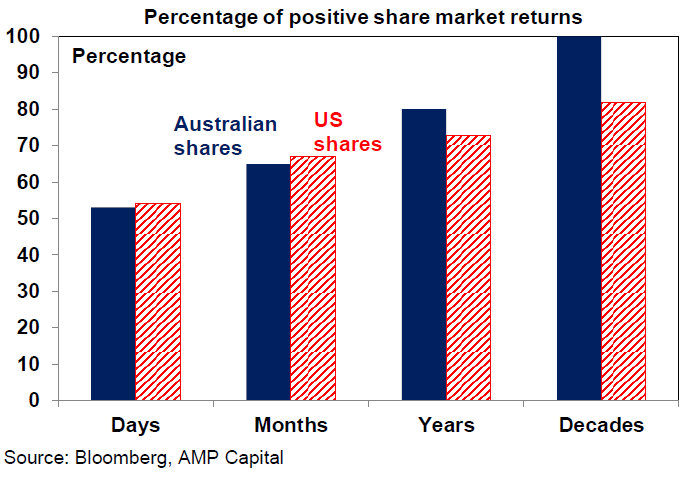

- Don’t’ check your investments so much – on a day-to-day basis it’s a coin toss as to whether the share market will rise or fall but the longer you stretch it out between looking at your investments the more likely you will get positive news. See the next chart.

6. Buy low, sell high

The cheaper you buy an asset (or the higher its yield), the higher its prospective return will likely be and vice versa, all other things being equal of course. So as far as possible it makes sense to buy when markets are down and sell when they are up. Unfortunately, many do the opposite, ie buying after a big rally and selling after a collapse…which just has the effect of destroying wealth.

Selling at the panic low point in March would not have been a good move as it would have just locked in a loss – but of course, it might have felt easy in the midst of the panic at the time. Again turn down the noise!

7. Beware the crowd at extremes

It often feels safe to be in a crowd and at times the investment crowd can be right. However, at extremes the crowd is invariably wrong – whether it’s at market highs like in the late 1990s tech boom or market lows like in March. The problem with crowds is that eventually everyone who wants to buy in a boom (or sell in a bust) will do so and then the only way is down (or up after crowd panics).

As Warren Buffet has said the key is to "be fearful when others are greedy and greedy when others are fearful". And coronavirus does nothing to change that.

8. Focus on investments with sustainable cash flow

If it looks dodgy, hard to understand or has to be based on obscure valuation measures then it’s best to stay away. If an investment looks too good to be true it probably is. By contrast, assets that generate sustainable cash flows (profits, rents, interest) and don't rely on excessive gearing or financial engineering are more likely to deliver. Again, the coronavirus hit does nothing to change this.

9. Seek advice

Given the psychological traps, we are all susceptible too (like the tendency to over-react to current investment market conditions or to pay more attention to information and opinion that confirms our own views) and the increasing complexity of investing that makes it anything but easy, a good approach is to seek advice via an investment service or a coach such as a financial adviser, in much the same way you might use a specialist to look after your plumbing or medical needs.

As with plumbers and doctors, it pays to shop around to find a service or adviser you are comfortable with and can trust. Even I have a financial adviser to help deal with the complexity of investing.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

1 topic

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment