A better bet than Aussie housing

Nathan Bell

Investsmart

Investing in Australian residential property has been nothing short of a goldmine in recent years. Charlie Munger, Warren Buffett’s business partner, would call it a lollapalooza effect, where several forces, such as low interest rates, the rapid development of the Chinese economy and an influx of foreign buyers, have culminated in extraordinary residential property price rises.

When people are crying after ‘winning’ an auction, you can safely bet that any margin of safety buying Australian property today has disappeared. This isn’t the case in the US, though. Although the US stockmarket and home prices in major American cities have fully recovered since the GFC, the homebuilding industry hasn’t.

There are three major tailwinds that should kick the industry into overdrive over the next decade, however, and we’ve invested in a home builder whose historical returns share more in common with technology stocks such as Facebook and Google (now Alphabet) than an old-fashioned, cyclical home builder.

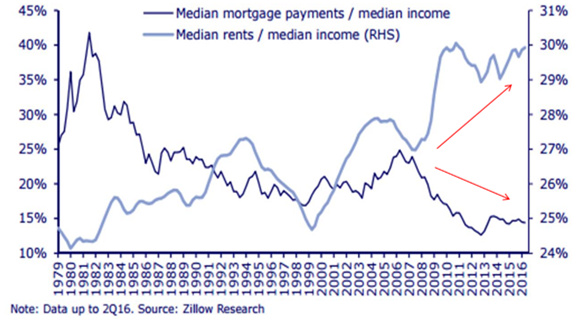

1. Cheaper to buy than rent

Unlike in Australia, where mortgage repayments are consuming a high proportion of incomes despite pygmy interest rates, in the US it’s much cheaper to buy than rent (on average see Chart 1 below).

Although it’s becoming increasingly difficult to buy a home in major US cities such as New York, Los Angeles and San Francisco, where prices are very high – as with Sydney and Melbourne – in more regional areas, where many home builders focus, the cost of building a home remains affordable by historical standards.

Chart 1. US median mortgage payments and rents as a % of median income

Source: Zillow Research

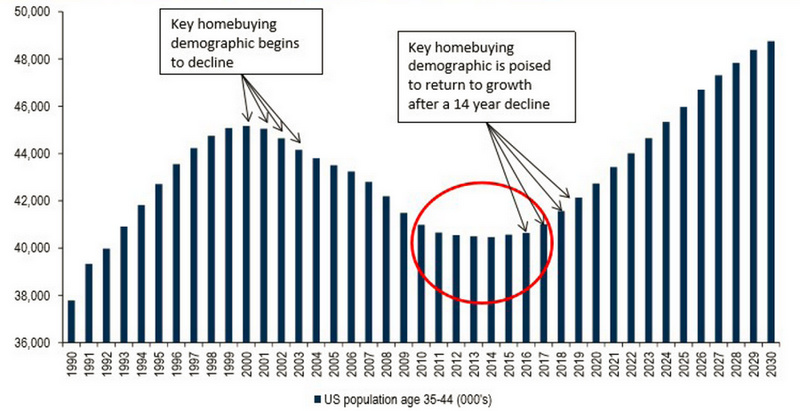

2. Population tailwind

Unlike in many countries where demographics are going to become more unfavourable as the population ages, the Millennial cohort in the US will be the country’s largest ever, even exceeding the Baby Boomers.

Chart 2, below, shows the large increase expected over the next 13 years. In the red circle, you can see that the age group of 35- to 44-year-olds has only just started to grow again. With many people deferring major life decisions due to the severity of the GFC, we expect people in this demographic to increasingly start families and buy homes, cars and baby seats as they move out of from their parents’ garages and basements.

Chart 2. US population of 35-44 year olds

Source: BofA Merrill Lynch

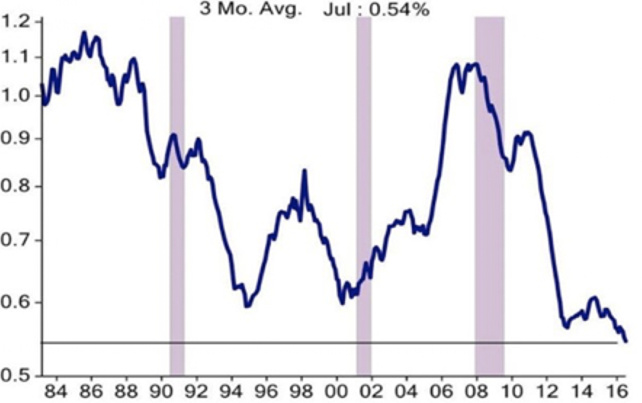

3. Low inventory

Lastly, the number of US homes available for sale as a percentage of the population is at its lowest level in at least three decades, as Chart 3 shows. Housing starts are running at about 1.1 million, compared with a long-term average of 1.4 million. Given the expected growth in the Millennial population and obsolescence of the existing housing stock, other estimates put the future requirement at 1.6 million. If that’s correct, the current deficit of new homes being built could further stimulate demand over time as the industry plays catch up following the slow recovery since the GFC.

Chart 3. US existing houses for sale as a % of US population

Source: ISI Group

NVR changes its spots

If the only way to benefit from these trends were to buy a highly leveraged home builder that flirted with bankruptcy at the first sign of a recession, we’d pass. But NVR is a different cat.

Paul C. Saville watched the original incarnation of home builder NVR go broke before becoming chief executive in 2005. Unlike executives at virtually every other listed home builder on the planet, he learned from the experience and constructed a way to protect the company from recessions.

Instead of dangerously leveraging the balance sheet to accumulate land for development, NVR lays down 10 per cent of the purchase price for an option on future development. This means the balance sheet isn’t highly geared, allowing the company to buy back 75 per cent of its shares on issue over the past 20 years. That’s a remarkable feat for any company, let alone a home builder, which is why earnings per share has increased by 26 per cent a year over the same period.

In 2009, NVR was the only listed US home builder to make a profit and post respectable shareholder returns through the GFC. With US housing stock now reaching record lows, interest rates still low and the Millennial population – the country’s largest ever – reaching a median age that suggests its members will soon start having families, the company is well placed to benefit from an increase in building. And if housing doesn’t pick up, we expect the company to buy back plenty more shares.

In summary, this is a remarkable company operating in an unpopular sector with insiders that have skin in the game. It’s just one example of looking for value where others aren’t, which will be key to earning a satisfactory return in a market flush with more money than good investment ideas.

Nathan Bell is Head of Research at Peters MacGregor Capital Management.

Disclosure: Peters MacGregor Capital Management Limited holds a financial interest in NVR through various mandates where it acts as investment manager.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

5 topics

Nathan Bell

Portfolio Manager

Investsmart

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

Expertise

Nathan Bell

Portfolio Manager

Investsmart

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

Expertise

Comments

Comments

Sign In or Join Free to comment