Commercial vs. residential property - a different way to invest

Steven Bennett

Charter Hall

Given the notable rise in residential values over recent years, the sector has drawn an increased amount of attention as a real estate investment class. Australia’s real estate sector as a whole has benefited from accommodative interest rates and strong population growth. Despite these similarities, the characteristics of the residential sector and the commercial real estate sector are quite different; primarily driven by the different investor and occupier profiles.

Residential property typically has a lower capital price compared to the other commercial real estate classes. A commercial office, industrial or retail asset typically requires significantly more capital to acquire and maintain. As such, direct investment in commercial property is undertaken by a fewer number of investors who have the required knowledge or financial capacity to purchase multi-million-dollar assets; and the capacity to undertake the day-to-day management.

Managers such as Charter Hall have dedicated teams to undertake the full suite of operations required to invest and manage Australian commercial property. This includes development, capital transactions and asset management and leasing teams. The decision-making process, therefore, requires more people and stages for checks and balances. This due diligence process and other barriers to entry tend to reduce the levels of speculative activity.

How and why the cycles differ

Most importantly, the residential and commercial property sectors have different types of tenants and demand drivers. Because of this, the cycles between residential and the other real estate sectors are typically different. As widely reported in numerous media publications, Australia’s residential market is currently under increased attention with concerns around potential oversupply, growing vacancy and the subsequent pressure on rental yields. However, Australia’s office vacancy rate has been trending downward over recent years. The national office vacancy rate has reduced from 12.3% in December 2015 to a six-year low of 8.4% at December 2018. This is forecast to gradually decline over the years to 2021 (1). At December 2018, the Sydney CBD office vacancy rate reached its lowest point since the 2000 Olympics and the Melbourne CBD office market reported its lowest vacancy rate on record.

Both office markets have generated significant levels of rental growth. Over the past two years, the Sydney and Melbourne market generated amongst the strongest rental growth rates globally. Prime effective office rents in the Sydney market have increased by 34.1% (15.8% p.a.). While lower levels of vacant space supported significant secondary grade effective rental growth of 38.3% (17.6% p.a.). Over the same period, both prime and secondary effective office rents in Melbourne climbed strongly: 22.4% (10.6% p.a.) and 35% (16.2% p.a.) respectively. On a global level, over the two years to 3Q18, the Sydney and Melbourne CBD office markets provided the second and fourth highest rental growth rates.

The lease profiles between residential and commercial are also markedly different. Commercial real estate leases are usually longer, typically ranging from 3 to 20 years. These commercial leases usually benefit from fixed annual or market related annual rental increases. Further, these leases tend to be to quality tenants which generally have low risks of defaulting. These include tenants such as Commonwealth or State government agencies or well-regarded corporations. Good managers undertake comprehensive tenant analysis and target quality tenants through economic cycles.

Due to the different occupier and investor mandates, the various real estate sectors will typically follow varied cycles.

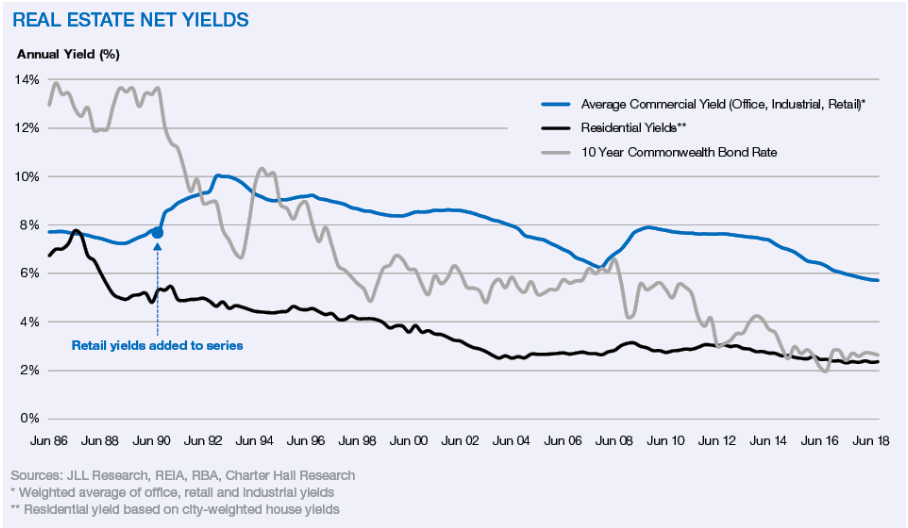

There’s no right or wrong answer as to the ‘right’ type of property to invest in; the correct allocation will be unique to each investor. However, current net rental yields for commercial property are compelling on a relative basis.

(1). JLL Research

Never miss an update

Stay up to date with the latest news from Charter Hall by hitting the 'follow' button below and you'll be notified every time I post a wire.

Charter Hall Group (ASX:CHC) is one of Australia’s leading fully integrated property groups, with over $28.4 billion of high quality, long leased property across the office, retail, industrial and social infrastructure sectors. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Steven is CEO of the Direct Property business within Charter Hall.

2 topics

Steven Bennett

Direct CEO

Charter Hall

Steven is CEO of the Direct Property business within Charter Hall.

Expertise

Steven Bennett

Direct CEO

Charter Hall

Steven is CEO of the Direct Property business within Charter Hall.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets