A makeover for China’s cosmetic industry

Joohee An

Mirae Asset Management

The cosmetic industry is consistently trying to adapt products against dynamic and fiercely competitive environments in the hope of capturing that extra edge in market share, similar to that of the fashion industry in the previous article (“Guochao” – The Rise of Homegrown Chinese Labels).

With the rise of e-commerce, there is a drastic improvement in production efficiency, shrinking the inception-to-sale lead time to as short as two weeks in 2019. The short lifespan was exhibited when a popular face mask took China by storm in 2019, and a competitor was able to launch a very similar product in as short as two weeks following the wave of demand for this hot product.

The advantage of an ultra-short product lifecycle strategy translates to a positive Return-on-Investment (ROI) endeavour for companies that are successful in execution. Aided by polished marketing operations, a handful of domestic beauty product companies found a profitable and fast-growing niche in the middle of the premium spectrum. Their products are gradually filling the previous void in supply between the high-end Multi-National Corporation (MNC)/foreign brands and the mass-market domestic brands. Thus, the apparent market share gain in POS sales value terms is the result of organic up-trading.

Premiumisation: The Key to the Growth of Domestic Brands

Due to the lack of enduring domestic Chinese brands, the competition among local beauty product companies is much higher than those seen among MNCs. This is especially true in the premium segment, where brand equity grants the highest pricing power. In the premium segment, consumer awareness of brand equity is central to their product choice. Consumers that fall within the premium MNC market category have a stronger sense of brand loyalty, and regardless of whether a competitor delivers an identical product offering, the consumer would generally tend to stick to the original brand.

Premium MNC consumers have attached their consumption decision to the brand itself, and unless the quality of these products drops significantly, the switching cost between brands will remain high. The premium MNC market has high barriers to entry, making it difficult for competitors to close in on market share. The most notable example is Proya’s Ocean Skincare line of products, which essentially mimics that of La Mer’s products. Despite Proya’s marketing and product advantage over its domestic peers, it barely created any material effect on La Mer’s sales.

Domestic brands are agile in their approach in providing mass-market products, being able to replicate products of competitors effectively with speed to deliver demand-driven trends. These companies may find it difficult to penetrate the premium MNC market but remain competitive in the mid-tier space.

Domestic Segment Trend: Consolidation and Premiumisation

According to Euromonitor, the beauty product market in China had RMB360bn in aggregate sales in 2017, of which 74% was sales in the mainstream segment. Tencent’s 2019 domestic beauty products report found that domestic producers had 56% of the overall beauty product market share by value in 2018.

As of 2019, colour cosmetics sales only account for a tiny proportion of annual sales of Proya and Marubi; this could be a potential growth driver in the future. Despite colour cosmetics only comprising of a small portion of sales, Proya has delivered strong colour cosmetics growth for 2019. Colour cosmetics grew 482% YoY in 2019 and is now 5.3% of 2019 sales, up from 1.2% of sales in 2018. On the other hand, Marubi’s 2019 colour cosmetics sales declined 5.8% YoY, accounting for 1.4% of 2019 sales.

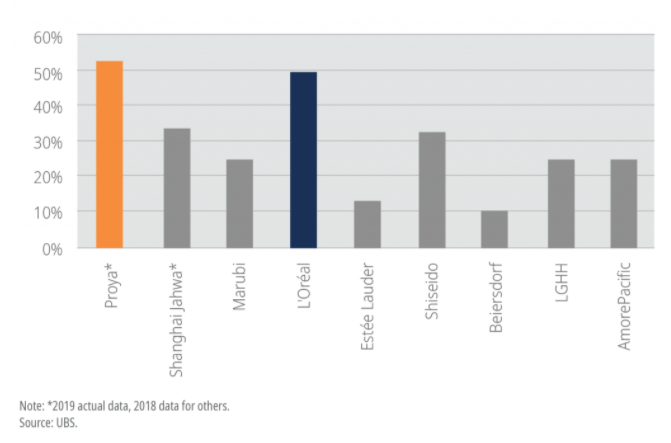

With the new era of internet shopping, there is an increasing number of consumers who are moving online to save time and money. From a pricing perspective, consumers are able to compare competitors and check reviews of products, allowing them to make informed decisions on their purchase. In terms of e-commerce as a percentage of the People’s Republic of China (PRC) sales, we can see from Exhibit 1. that Proya, Shanghai Jahwa, and Marubi make up a significant portion of sales, comparable to its global competitors L’Oréal, Estee Lauder and Shiseido.

Exhibit 1 - E-commerce as a percentage of PRC sales

Domestic Penetration

Chinese domestic cosmetic brands have seen a makeover in the past decade. They have created a presence in the mid-tier range, even though the penetration into the premium MNC market is still relatively low. Companies are increasingly engaging with their consumers and are learning from industry leaders the meaning of value creation for customers. The journey for Chinese domestic players is still growing at a full-speed, whereas they follow leading players and are yet to lead the market to a premiumised MNC level. They are, however, adapting to changes in consumer behaviour and successfully tapping into a mid-tier niche.

The question remains in sustainability. Maintaining traction against competitors and consistently innovating products to capture consumer interest will be the barriers most face. In the long-term, we believe if Chinese domestic cosmetic brands strive to reach the iconic success of multi-national cosmetic brands, they will need to be seen as an aspirational and trend-setting leader on a global scale.

Seize the opportunity

Mirae Asset seek to capitalise on the growth in the middle-class consumption across Asia and focus on high-quality companies with solid long-term growth prospects. Click the 'FOLLOW' button below for more insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

It's an exciting time to invest in Asia. Over the last 14 years, I've experienced first hand the growth and evolution of equity markets across the region.

We're seeing a shift in global production and consumption. In Asia, Consumption Growth is wide-ranging and the main driver of investment returns. I focus my investment efforts in companies that directly benefit from this long-term trend.

I manage around AUD2b in AUM. My immediate team and I are based in Hong Kong. We work collaboratively with colleagues in our Mumbai and Shanghai offices and also regularly travel to meet with business stakeholders and decision makers across the region.

We are proud to be a Fund Manager from Asia - investing in Asia's future.

........

Mirae Asset Global Investments (HK) Limited content shared through Livewiremarkets.com is neither an offer to sell nor solicitation to buy a security to any person in any jurisdiction where such solicitation, offer, purchase or sale would be unlawful under the laws of that jurisdiction. Investment involves risk.

The information in the material contribution is based on sources we believe to be reliable but we do not guarantee the accuracy of completeness of the information provided.

The material contribution through Livewiremarkets.com has not been reviewed by SFC and shall only be circulated in countries where it is permitted.

This material contribution is intended solely for your private use and shall not be reproduced or recirculated either in whole or in part, without the written permission of Mirae Asset Global Investments. Whilst compiled from sources Mirae Asset Global Investments believes to be accurate, no representation, warranty, assurance or implication to the accuracy, completeness or adequacy from defect of any kind is made. The division, group, subsidiary or affiliate of Mirae Asset Global Investments which produced the underlying content shall not be liable to the recipient or controlling shareholders of the recipient resulting from its use. The views and information discussed or referred in reports through Livewiremarket.com are as of the date of publication, are subject to change and may not reflect the current views of the writer(s). The views expressed represent an assessment of market conditions at a specific point in time, are to be treated as opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. In addition, the opinions expressed are those of the writer(s) and may differ from those of other Mirae Asset Global Investments’ investment professionals.

The provision of content through Livewiremarkets.com shall not be deemed as constituting any offer, acceptance, or promise of any further contract or amendment to any contract which may exist between the parties. It should not be distributed to any other party except with the written consent of Mirae Asset Global Investments. Nothing herein contained shall be construed as granting the recipient whether directly or indirectly or by implication, any license or right, under any copy right or intellectual property rights to use the information herein. Content may include reference data from third-party sources and Mirae Asset Global Investments has not conducted any audit, validation, or verification of such data. Mirae Asset Global Investments accepts no liability for any loss or damage of any kind resulting out of the unauthorised use of this document. Investment involves risk. Past performance figures are not indicative of future performance. Forward-looking statements are not guarantees of performance. The information presented is not intended to provide specific investment advice. Please carefully read through the offering documents and seek independent professional advice before you make any investment decision. Products, services, and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries, and/or distributors of Mirae Asset Global Investments as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction.

Australia: Mirae Asset Global Investments (HK) Limited (“Mirae HK”) is exempt from the requirement to hold and Australian financial services license in respect of the financial services it provides in Australia. Mirae HK is authorized and regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws, which differ from Australian laws.

1 topic

Joohee An

Senior Portfolio Manager

Mirae Asset Management

It's an exciting time to invest in Asia. Over the last 14 years, I've experienced first hand the growth and evolution of equity markets across the region. We're seeing a shift in global production and consumption. In Asia, Consumption Growth...

Expertise

Joohee An

Senior Portfolio Manager

Mirae Asset Management

It's an exciting time to invest in Asia. Over the last 14 years, I've experienced first hand the growth and evolution of equity markets across the region. We're seeing a shift in global production and consumption. In Asia, Consumption Growth...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets