A page from the Chinese commodity playbook

Nikko AM

Amova AM

China has had a significant impact on the supply side in two key global commodities during 2016. Going forward, look out for further actions from China on the supply side of commodities.

For years, several of China’s primary industries have been plagued with oversupply. These oversupply issues were evident from the vast coal fields spread throughout China through to the steel and aluminum industries in eastern China to the aging oilfields of Petrochina and Sinopec, which in turn has led to poorer profitability. In the past, excuses like social security and national interests have always existed for not rationalizing these sectors but in 2016, China went out and did something different. China’s action in 2016 had a profound impact on commodity pricing and the rules by which the commodity industry participants play by.

During 2016, China took various actions, more directly in coal but more subtly in the oil and gas sectors, which had a significant impact on production.

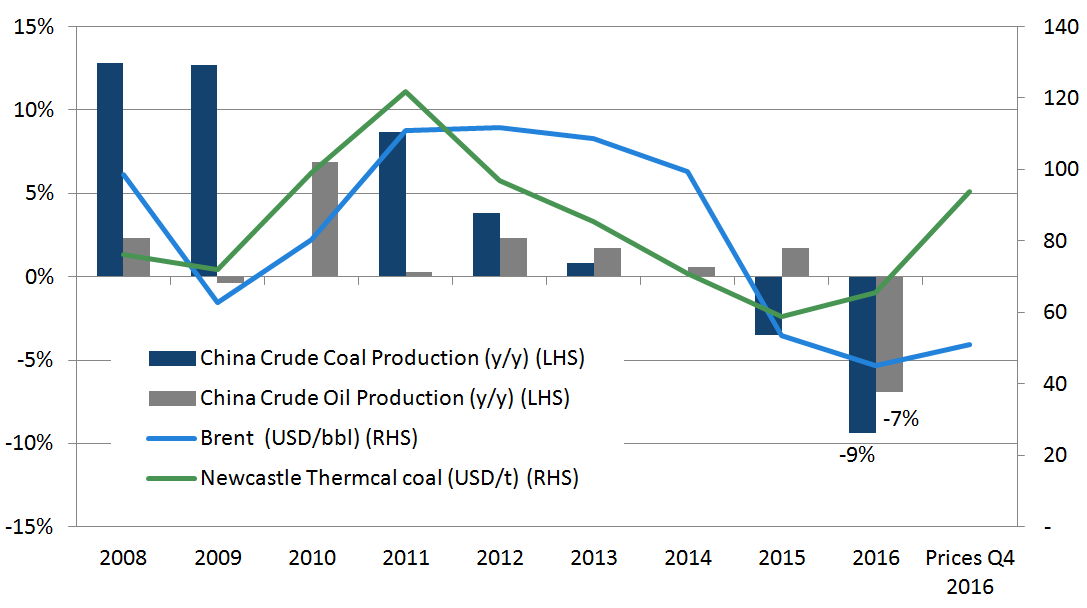

Image 1: Chinese coal and oil production

Source: NDRC, Bloomberg

What happened in Chinese coal?

For the last five years, coal mining profitability in China (and globally) has been on the downtrend. Combined with diminishing demand from alternative sources of power and increasing coal supply, the outlook for the Chinese coal miners seemed increasingly uncertain.

In mid-April last year, a subtle directive was issued, in which working days for all coal mines was reduced to 276 days a year from 330 days. The price impact was not immediate; from April to June 2016, thermal coal prices were relatively muted, but afterwards, port inventories and stockpiles at the power producers needed replenishing and coal prices reacted. By November, when the 276 day rule had been fully executed, coal production was down 12% year on year and coal prices had almost doubled. The Chinese government had a new problem that it had not faced in four years, what do to do about high domestic coal prices?

By mid November, the National Development and Reform Commission (“NDRC”) called a meeting with the top ten Chinese coal producers and laid out its game plan. The plan was simple, the NDRC established a target range of coal prices and when the coal prices were above this, the producers were allowed to increase production, and when the prices are below this, the producers have to cut back production.

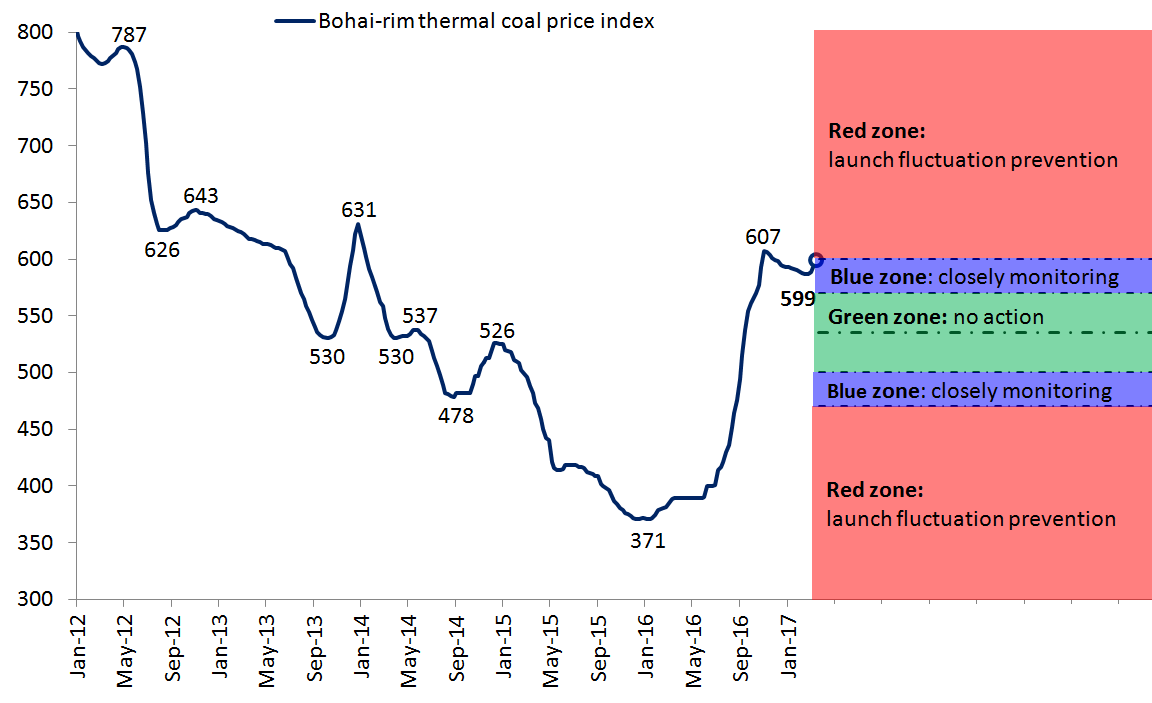

Image 2: 276 day rule takes full impact on coal prices

Source: CQ Coal, Citi Research

With these actions, the NDRC solved two problems, the low profitability of its coal mines was eliminated overnight and the use of coal would be reduced, thus helping it hit its power mix requirements.

So from here on into the foreseeable future, coal pricing will be dictated and controlled by the NDRC.

What about Chinese oil production, what happened there?

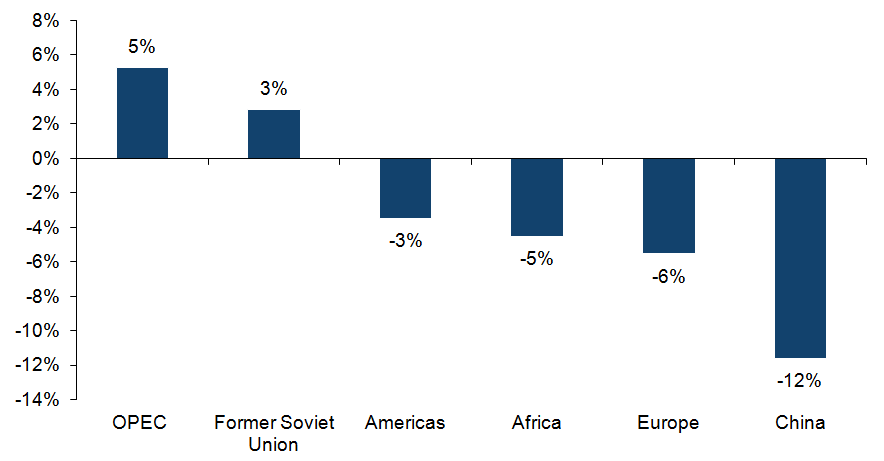

Which oil producing block cut oil production the most in Q4 2016. Answer –

China.

China is a relatively small producer of oil, at 4% of global supply in 2016. However, its production decline of 0.5 million barrels per a day from Q4 2015 to Q4 2016 is sizeable compared to OPEC’s proposed production cuts 1.2 m barrels a day. Whilst most journalists have written about OPEC’s proposed cuts, China’s production cuts have not been given much press coverage. What happened here? China crude self-sufficiency has taken a backseat. Rather than focusing on production growth, Chinese SOEs were encouraged to improve efficiency and profitability. Hence, this has encouraged the closure of high cost, uneconomic wells - even at the expense of production volume.

With the release of China’s 13th 5 year plan, China’s ambition for growing oil production looks relatively subdued with flat production an optimistic outcome.

Global Oil Production Q4 2015 vs Q4 2016 year on year production changes

Source: IEA Oil Market Report

What cartel is next? – Steel and Aluminium

The results of the China’s action in coal and oil are still in the early days and their determination and ability to control the coal market is yet to be fully tested.

What commodities sectors could be next for the China? Commodities that stand out next are steel and aluminium. China has laid the ground work for steel with its 13th five year plan for the steel industry. With capacity reduction targets, frameworks for new capacity additions to only replace obsolete capacity and increasing the state owned enterprise share of production to 60% (from the current levels of 35%), the steel capacity and production from China looks likely to be restricted.

Aluminium could be a story for later this year. The Ministry of Environmental Protection released a draft air pollution prevention plan which requires aluminum smelters in Hebei, Shandong, Henan and Shanxi to suspend aluminum smelters and alumina refineries to suspend production from the end of 2017.

Unintended Winners

China’s policies in the last year have had a series of “unintended” winners. The most obvious winners from China’s coal policies were the seaborne coal exporters. Whilst China has restricted its domestic coal production, Chinese imports of coals increased 25 percent year on year leading to a significant increase in profits for Australian and Indonesian exporters of coal. However, it has become pretty clear that the fate of these unintended winners is clearly in the NDRC’s hands.

Contributed by: Chu Kit Kwa, Equity Analyst. Original blog here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies.

In April 2021, Yarra Capital Management acquired Nikko Asset Management’s Australian business and assumed responsibility for the distribution of Nikko Asset Management’s funds in the Australian market.

4 topics

Nikko AM

Amova AM

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In April 2021, Yarra Capital Management acquired...

Expertise

Nikko AM

Amova AM

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In April 2021, Yarra Capital Management acquired...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management