TOL - 17th Nov, 2020

A vaccine for COVID derangement syndrome

COVID Derangement Syndrome (CDS) is a nasty affliction that causes investors to misprice stocks. Some sufferers have it so bad they will buy or sell without regard to price. Symptoms include selling low, buying high, regret and FOMO. Even mild cases can result in sleepless nights.

At Monash Investors, we have been working on a cure for CDS. Just like the vaccines under development by Big Pharma for COVID-19, we have been testing our cure and it is showing promising results.

CDS is a disease of perception, so the cure is to provide a framework that creates clarity of thought. This framework allows investors to think more clearly about the impact of COVID-19 on a business’s future earnings. Applying this clarified earnings outlook to the investor’s valuation model results in a CDS free target price for the stock. Problem solved.

If the investor does not have a valuation model he should seek professional help, otherwise the disease will just have to run its course.

All jokes aside

Seriously though, interpreting the effect of COVID-19 on businesses and their valuations has been critical for investors this year. It has involved the complex interaction of the disease playing out, governments responding, consumer behaviour, and now an imminent vaccine rollout.

For fund managers, the stock market is a harsh and indifferent marker. All that matters are the results, and they are there for all to see. There is more than one strategy to make money in the market and there is more than one way to think about COVID-19. One can always argue the toss, that’s what makes a market. What follows is the way we at Monash Investors have been thinking about it.

The first step is to split COVID-19 impacts into two parts:

- Structural impacts are those that cause long lasting changes to a business.

-

Cyclical impacts are those that cause short/medium term changes to a business.

Then we show how some businesses are subject to both structural and cyclical impacts, and how that changes their outlook through time.

Finally, we give some examples of how we used this framework in our buying and selling of stocks, and what we are currently thinking.

Structural impact of COVID-19

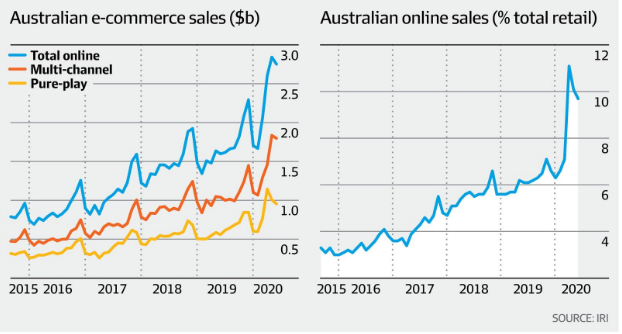

A big class of winners from COVID-19 are online retailers, such as Kogan (ASX: KGN) or Temple and Webster (ASX: TPW) who have benefited from a step change in existing trends. Online sales as a percentage of total retail sales in Australia had already doubled over 5 years prior to the pandemic, but at around 7% were well behind the USA at 12% and the UK at 19%. Across the world, they have grown as consumers become increasingly comfortable with buying online. It is a common observation by retailers that once a customer starts buying online, their frequency of purchase ramps up over time too.

Source: AFR 3 Sep 2020 (VIEW LINK)

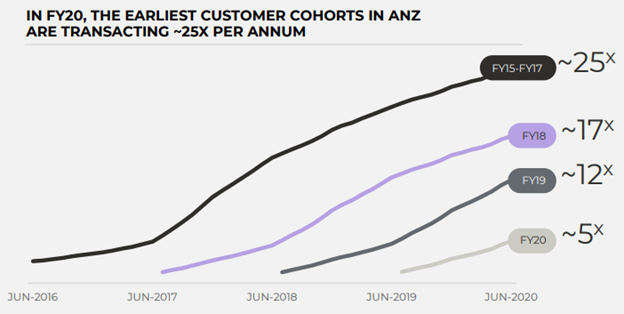

An extreme example of this ramp up effect is Afterpay (ASX: APT) where customer transactions on average increase from 5x per user in their first year, to 25x per annum beyond year 4. As a result, this step change in new online customers permanently brings forward the growth that would have otherwise occurred more slowly.

There have also been structural losers from COVID-19. Shopping centres and ‘bricks & mortar’ based retailers are the other side of the growth in online penetration. Structurally, there are other businesses affected too such as banks, due to the longer term effect on their net interest margin from sustainably lower interest rates, or Challenger (ASX: CGF) on its annuity business.

A knock on effect occurs when companies must issue more equity to support their short/medium term liquidity. The resulting dilution in EPS is permanent.

Cyclical impact of COVID-19

Travel and tourism related companies were obvious COVID-19 losers. They were immediately effected by closed borders, for example Qantas (ASX: QAN), Flight Centre (ASX: FLT) or Ardent Leisure (ASX: ALG). So were companies that provided services not needed in lockdown or due to crowding restrictions. For example, Transurban (ASX: TCL) had few cars, G8 Education (ASX: GEM) had few children, and no one wanted to send their loved ones to Estia’s (ASX: EHE) aged care centres.

The short to medium term impacts on these industries are comparable to a business cycle. Some such as the car dealer Eagers (ASX: APE) have seen their business recover very quickly. Borders re-opening and people travelling by air is taking longer but it’s happening. Parents need to work and they eventually put the infants back in childcare.

Likewise, many businesses were cyclical winners. They benefit over the short to medium term from people working from home (WFH) or by a redirection of money not spent on a holiday. Some examples were JB Hi-fi (ASX: JBH) for home computers and tech, Wesfarmers’ Bunnings (ASX: WES) for home upkeep, and Coles supermarkets (ASX: COL) and Domino’s Pizza (ASX: DMP), from people eating at home more. However, unless structural changes in behaviour take place, these are only temporary benefits.

Bringing it together

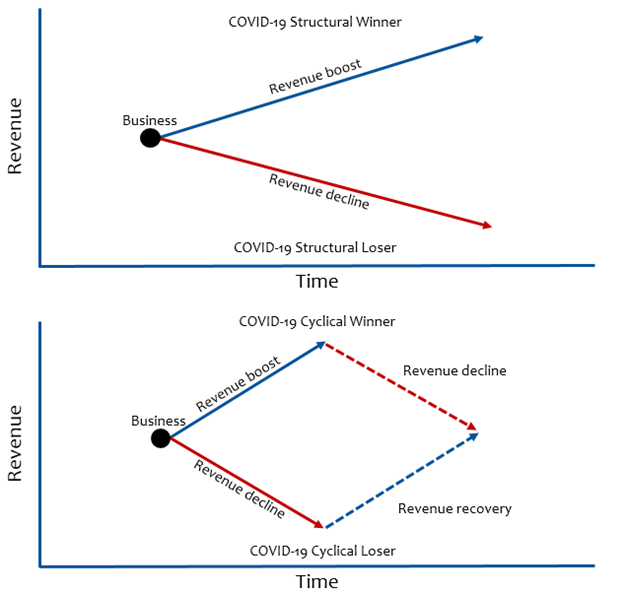

The following charts are an illustration of the business impacts interplaying from being a winner or loser from COVID-19. They are generalisations. The degree by which company forecasts are impacted varies greatly from business to business.

The first chart shows changes in revenue for businesses that are structurally impacted. The revenue effect of being a winner or loser continues throughout the pandemic and beyond, and does not fall back.

The next chart shows the impact over the same period for businesses cyclically impacted by COVID-19. There is a temporary boost (or decline) in revenue until the peak business impact of the pandemic occurs, and then it reverses.

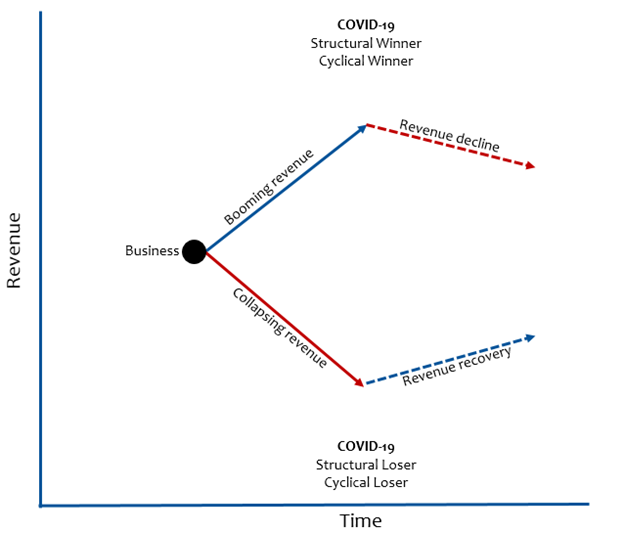

The third chart shows two out of a possible four combinations of the impacts. These are the two most common combinations.

A business that is both a structural and cyclical winner gets a double boost, before having the revenue fall back somewhat. TPW as an online retailer of household furniture is a good example of such a company. Their increased revenue is part structural, because COVID-19 has accelerated the existing trend to online furniture sales that was happening anyway. Their initial boost in revenue is also part cyclical, a result of people redirecting money otherwise spent on travel or entertainment, and will fall back.

FLT is an example of a company that is a loser twice. Structurally, a result of the need to close permanently much of its retail store footprint and due to the shareholder dilution from emergency capital raises; and cyclically, due to the cessation of air travel which will recover in time.

Investment outcomes

Our objective in “modelling” the future of a business is to value it, to see if there is an opportunity for investors to make money.

Calculating a Discounted Cash Flow (DCF) value for a stock is not just an academic exercise. It brings together accounting, spreadsheet and mathematics skills, as well as knowledge specific to a business, its industry and the wider world. Forecasts are by their nature best guesses, and the DCF requires forecasts be made over many years, so the ‘confidence band’ around a calculated target price is large. For well-covered stocks, that margin for error around the target price will typically be larger than its difference to the stock price.

Unpredictable new information can change things completely. The evolution of the pandemic is a great example. It pays to have some perspective and modesty when handling the uncertainty of valuing a stock. At Monash Investors we deal with this by using lessons from recurring business situations, incorporating new information as quickly as we can, and having a relentless focus on the upside/downside to our target prices. We only invest in stocks that have more than 60% upside to our target price or in the case of shorts more than 30% downside, and adjust our positions accordingly.

This approach has served us well generally, but has been particularly successful so far this calendar year. At the time of writing, our funds are up about 22% after fees this calendar year, compared to the total return of the ASX200, which is down about -2%. The following is a sample of the decisions that we made.

Early selling/shorting

In late February, we recognised the language used by the CDC indicated that there was a global pandemic underway, prior to its announcement. See link to previous wire. Incorporating the effect of this into our forecasts led us to sell down some of our retailer holdings that sourced goods from China, such as Lovisa and Kogan (ASX: LOV, KGN). We also shorted Qantas (ASX: QAN), travel agents Flight Centre and Corporate Travel (ASX: FLT, CTD) and casinos Crown, Star City and Sky City (ASX: CWN, SGR, SKC).

More shorting but also some buying

By mid-March the market had fallen over 20% by then, but many stocks had fallen much more.

For some stocks this wasn’t enough, because of their exposure as both structural and cyclical losers. This continued to generate a DCF value well below their already fallen share price. For example we had originally shorted QAN at $5.50, but as it fell it’s weight also reduced and we topped up with more shorting at $5 and $4. At the end of March it was $3.20. We had similar experiences topping up shorts in other stocks.

On the other hand, some stocks that were structural winners had fallen too far. A stand out here for us was Jumbo Interactive (ASX: JIN) which provides online access to lotteries. It had fallen from $13 in mid-February and we were able to establish a large position below $8 per share in March. By the end of March it was back to $9.40.

Buying COVID-19 losers cheaply

Eventually many stocks fell well below our target prices, despite their forecasts incorporating the future effect of COVID-19 on their businesses. As a result, we were covering many of the stocks we had shorted and in some cases going long. For example, we covered our short in QAN at $3.20 in April, and following an update by the company went long in May at $3.60.

COVID-19 winners hitting price targets

There are online based businesses that are both structural and cyclical winners, and they have seen their share prices go up multiple times over the last six months. As a result over the last month or two we have been reducing our holdings, or even exiting as stock have hit our price targets. These include City Chic and Kogan (ASX: CCX, KGN).

The “recovery trade”

The big uncertainty around COVID-19 is how the disease will play out. When will impacted activity recover? How will government influence this? Is there to be an effective treatment or vaccine, and if so, when? Our approach to valuing stocks positioned the portfolio ahead of the recent good news on vaccine progress, across a number of companies.

For example, in August around $7.70 we rebuilt our position in Lovisa (ASX: LOV) a ‘bricks and mortar’ jewellery retailer that had been badly impacted by store closures and a halted store rollout program. The LOV share price jumped 25% on the vaccine news, and since then, following an accretive acquisition, is currently above $11.

Current portfolio positioning

Because we reduce holdings or even exit as they near our price targets we have been net sellers recently. Our cash weighting is now 13% as a result. We are still able to find plenty of companies with more than 60% upside to our price target. The portfolio has a mix of stocks across industries such as healthcare, payment processing, retailing, travel and technology. The main recurring situations that they have in common are organic growth, store or product rollout, accretive acquisitions, or cyclical recovery.

Benefit at every stage of a cycle

Monash Investors Limited invest in a small number of compelling stocks that offer considerable upside and short expensive stocks that are at risk of falling. Want to learn more? Hit the 'contact' button to get in touch or visit their website for further information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

........

This presentation has been prepared by Monash Investors Pty Limited ABN 67 153 180 333, AFSL 417 201 (“Monash Investors”) as authorised representatives of Winston Capital Partners Pty Ltd ABN 29 159 382 813, AFSL 469 556 (“Winston Capital”) for the provision of general financial product advice in relation to the Monash Absolute Investment Company Limited (“MA1) and the Monash Absolute Investment Fund ARSN 606 855 501 (“Fund”). Monash Investors is the investment manager of MA1 and the Fund and is for information purposes only.

The Trust Company (RE Services) Limited ABN 45 003 278 831, AFSL 235 150 (“Perpetual”) is responsible entity of, and issuer of units in, the Fund. The inception date of the Fund is 2nd July 2012.

The information provided in this document is general information only and does not constitute investment or other advice. The content of this document does not constitute an offer or solicitation to subscribe for units in MA1 or the Fund or an offer to buy or sell any financial product. Accordingly, reliance should not be placed on this document as the basis for making an investment, financial or other decision. This information does not take into account your investment objectives, particular needs or financial situation. Monash Investors, Winston Capital and Perpetual do not accept liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information.

Any investment decision in connection with the Fund should only be made based on the information contained in the disclosure document for the Fund. A product disclosure statement (“PDS”) issued by Perpetual dated 12 September 2017 is available for the Fund. You should obtain and consider the PDS for the Fund before deciding whether to acquire, or continue to hold, an interest in the Fund. Initial Applications for units in the Fund can only be made pursuant to the application form attached to the PDS.

Performance figures assume reinvestment of income. Past performance is not a reliable indicator of future performance. Comparisons are provided for information purposes only and are not a direct comparison against benchmarks or indices that have the same characteristics as the Fund.

Monash Investors, Winston Capital and Perpetual do not guarantee repayment of capital or any particular rate of return from the Fund and do not give any representation or warranty as to the reliability, completeness or accuracy of the information contained in this document. All opinions and estimates included in this document constitute judgments of Monash Investors as at the date of this document are subject to change without notice. Perpetual is not responsible for this document.

21 stocks mentioned

1 contributor mentioned

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

Expertise

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

Expertise

Comments

Comments

Sign In or Join Free to comment