a2: could the milk be starting to turn?

We are long-term investors and as such we do not tend to focus on the 6 monthly results cycle like many investors out there.

That’s not to say we ignore it but we look through a different lens.

We are not interested in whether it is a slight “beat” or “miss” in terms of profit expectations, rather, are there any insights that strengthen (or weaken) the long-term opportunity set and the ability of the company in question to take advantage of it?

In that regard, we think the upcoming results of a2 Milk in late August, and over subsequent periods, will be worth keeping an especially close eye on.

Since 2008, a2 Milk (and other global infant formula (IF) brands) have benefited enormously from the melamine scandal in China which tainted the reputation of local IF producers and led to imported IF growing from single digit market share to around half of the market.

On top of this, a2 Milk did an exceptional job of grasping this opportunity through branding, packaging, managing the daigou and other sales channels, maintaining and growing margins.

CEO Geoffrey Babidge, and his team, deserve a major pat on the back, and investors (including our funds) have been very well rewarded along this journey.

The past though is just that, the past, and stock prices reflect future growth expectations so investors should always be looking forward.

Below are some of the aspects the market appears to be considering at least, and some that we have been pondering for a while but which, as yet, do not seem to be overly concerning the market:

Short-term

- Covid-19 caused a large acceleration of online/daigou sales in February as many bricks and mortar stores were closed and Chinese consumers stockpiled their pantries with staples including cans of IF.

- Pantry de-stocking – post the surge above it was natural to expect a period of softer sales as consumers work through the cans they stocked up on. a2 Milk noted this in their April update though overall guided to strong numbers for the FY20 year, as overall online was a benefactor.

Medium-term

- The Chinese government’s policy is to promote its domestic food industries, including domestic IF. Covid-19 may have helped in this regard given China’s relative success in containing Covid-19 cases, compared to the rest of the world (NZ is obviously an exception here though whether Chinese consumers make that distinction is questionable). The imported food chain appears to have become less desirable, driven in part by the news of cases linked to a market that had imported salmon. In the IF space you can also see this through the strong growth in the likes of Feihe which is a Chinese producer of premium organic IF.

- Birth rates: for us, the key question from Covid-19 was not the short-term pantry stocking/online sales spike above but what would it do to birth rates over next year or two? Interestingly, this was not a question we heard from any other investors/analysts. Our initial thought was that potential parents would be marginally less keen to bring a child into a world with a current pandemic and the resultant uncertainty and potential strain on hospitals, etc not to mention the economic impact from Covid-19. It was with interest that we read this article that seemed to back up that view (albeit from a global perspective not China). Only time will tell how many parents delayed or even decided permanently against having a child and the resultant impact on overall IF demand.

Longer-term

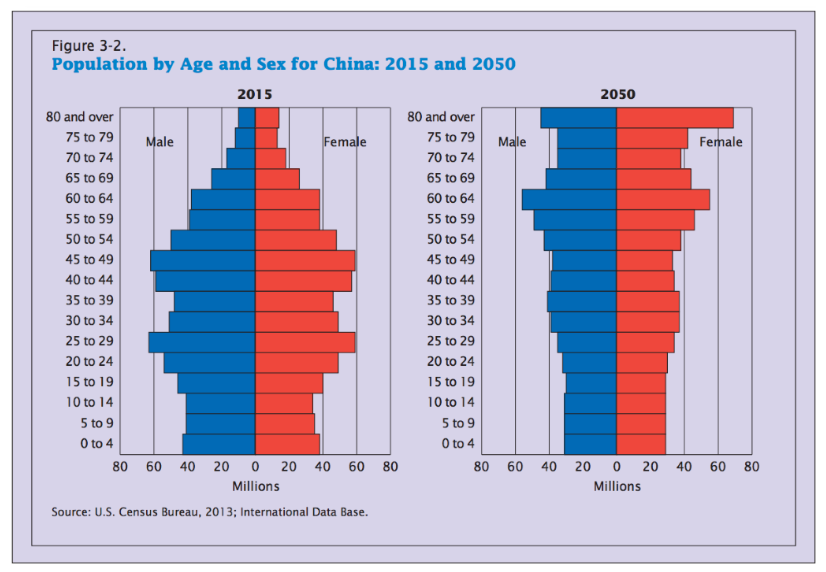

- Birth rates (again): Before Covid-19, the birth rate in China had already hit a seven decade low in 2019¹. The one-child policy, which was introduced in 1979, worked as intended but has significantly constrained the current population of females of potential childbearing age. The picture below shows 2015 on the left so the largest bar of 25-29 will now have shifted up to 30-34. This would seem to suggest that the downward trend in birth rates looks set to continue. Unlike most forecasting, population data cannot be argued with, though are investors reflecting this in their models or just relying on the standard terminal growth rate of 2-3% per annum for ever?

- Margins: a2 Milk have done a fantastic job of managing supply channels and protecting/growing margins along the way. This is always easier in an expanding market for imported IF. It is likely to be more challenging in a Chinese market which could be shrinking overall, with domestic production pushing to gain back a larger share of the pie and increased marketing spend required to compete in the bricks and mortar stores.

- USA and other growth areas: while a2 Milk is far from just a China IF story the margins from producing IF are so much higher than liquid milk that that part of the business dominates from a valuation perspective. The key question will be how quickly that success can be replicated with other geographies/products over time.

We definitely do not have all the answers here, but we will be watching closer than usual to see how these areas play out over the next few reporting periods.

¹See (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

........

Castle Point has taken all reasonable care in the preparation of these articles, however accepts no responsibility for any errors or omissions contained within. Past performance is not necessarily an indication of future performance. Opinions expressed in these articles are our view as at the date of issue and may change

3 topics

1 stock mentioned

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Comments

Comments

Sign In or Join Free to comment