Altium weighs on IT as reporting kicks up a gear (SGM, EHL, BHP, COH, ALU, WSA, OZL, COL, ABP)

Local reporting dominated the session today broken up by sporadic updates on the virus situation…reporting a mixed bag while the coronavirus continues to escalate - I had a chat with Livewire Markets about the virus and impact on markets last week (available here). On the session today, stocks ebbed and flowed, closing marginally lower however there were a few standouts on the stocks level. Altium (ALU) hit hard, down ~8% although finished up from session lows while earth moving equipment supplier Emeco (EHL) put on more than 6%% after a decent first half update

US Futures were trading lower during out time zone as they come back from their President’s day holiday. The defensive utilities best on ground today while he IT stocks were dragged down by ALU

Reporting schedule available here: CLICK HERE

In the below recording I cover: ALU, BHP, COH, EHL, SGM, OZL, WSA, COL – CLICK HERE

Overall, the ASX 200 fell -11pts / -0.16% today to close at 7113. Dow Futures are trading down -97pts/-0.33%

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE

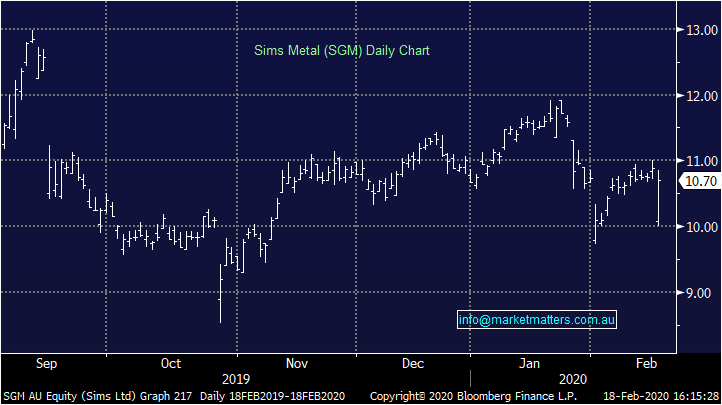

Sims Group (SGM) -1.65%: Another session where the market got this one wrong initially and sold the stock off aggressively after they report 1H20 earnings (or lack of!). The result was in line with downbeat expectations, an underlying EBIT loss of $23m is not positive, however they had guided a while back to a loss of between $20-$30m. Weak scrap metal prices the issue here, while Sims are also investing aggressively on improving operational efficiencies. Guidance was maintained although they reinforced the caveat of being market dependent. Stock down 6% early, closing down just a little over 1.5% by the end. We remain optimistic on this turn around play. We hold SGM in the Platinum Portfolio.

Sims (SGM) Chart

Emeco Holdings (EHL) +6.67%: All okay, revenue a tad below, profit a tad above, deleveraging remains a core focus, they talked up strong free cash flow generation expected in 2H and they also mentioned dividend, first time I’ve read that! EHL remain cheap (<10x), largely a consequence of carrying higher debt levels however they have clear strategy of delivering, have strong free cash flow generation and if all goes to plan, they should start paying dividends by FY22, not ‘that’ far into the future. We hold EHL in the Platinum Portfolio.

Emeco Chart (EHL)

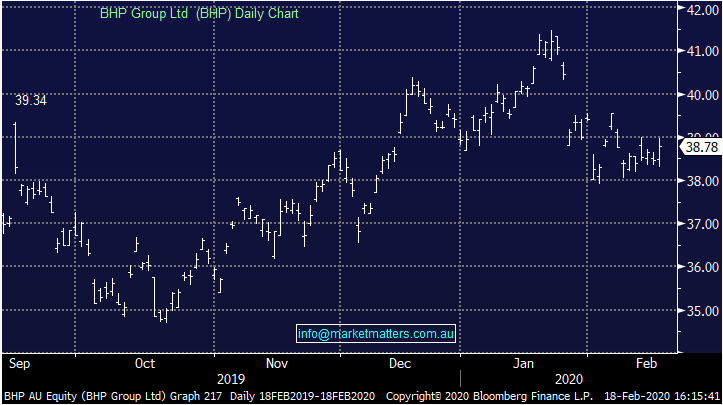

BHP Group (BHP) +0.81%: 1H20 numbers out this morning. Revenue climbed 3% on the first half of 2019, while net profit jumped nearly 30% thanks to a commodity price tailwind in iron ore. The $US5.2b profit was around 2% below expectations for the half. The biggest miss was the dividend, with BHP reducing its payout ratio to around 63% after running at around 70% for the past few years. This equated to a $US0.65 dividend while BHP maintained production and cost guidance for the full year.

BHP Group (BHP) Chart

Within the announcement today, BHP included a lot of forecasts which are always worth a read…Harry looks at key elements below, however the full run down is available here.

Some key economics points:

· Noted growth slowed in 2019 focussing on the drag of lowered trade in the year, but expects growth to pick up marginally towards around 3-3.25% in the current year.

· Set up a bear case for China growth at 5.5% which included re-escalating trade war and lingering virus effect set to be partly offset by a reasonable stimulus injection.

· India’s expected revival has seen delay’s although economic headwinds are expected to be near their peak. India will likely become the world’s biggest importer of iron ore in the next few years given there are no resources in the country

On the commodity front:

· Noted strength in China’s demand last year was resilient, expecting levels to plateau and then decline later in the decade. They expect the long run price to shift towards a higher-cost producer supporting the iron ore price in the medium term although volatility remains for now

· Coking coal appears constructive according to BHP and despite the volatility, it seems reasonable to suggest that met coal prices can sustain above long run marginal cost

· Copper demand was weaker than expected in 2019 although a structural deficit looks set to open up as the decade progresses with prices set to trend higher to support more production

· Oil has seen an estimated 0.2Mbpd drop in demand as a result of the virus, putting pressure on prices. As natural supply slides over the decade causing a slide up the cost curve, oil looks reasonable compelling in the medium to long term

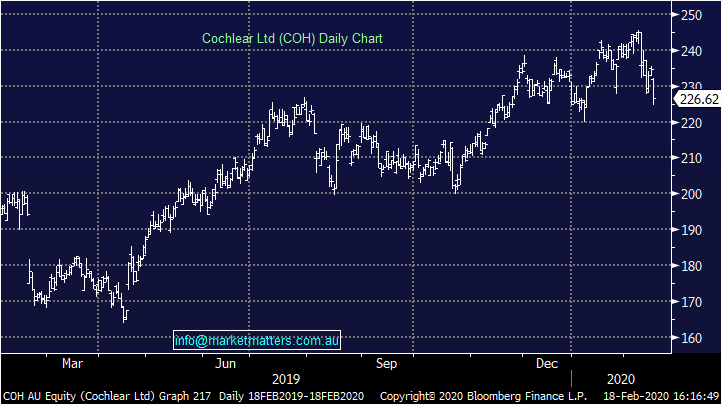

Cochlear (COH) -3.39%: Hit again today and rightly so. High P/E growth oriented business struggling to grow the top line. They already downgraded last week, and today they reported 1H NPAT still a little light on at $132.7m while they’ll need to do around $150m in the 2H to meet expectations. That’s achievable given they do have a 2nd half skew to earnings, however they have some work to do!

Cochlear (COH) Chart

Altium (ALU) -7.91%: Reported light and the stock was hit as a consequence today. We covered this yesterday (click here) however guidance that suggests achieving bottom end of consensus goes against their usual ‘beats’ and subsequent SP rally. Those betting on the beat were left disappointed today. A volatile session and big range today, ~$35 low to $40 top.

Altium (ALU) Chart

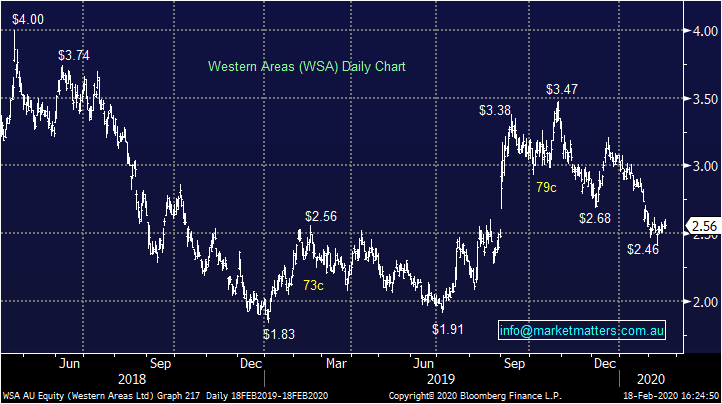

Western Areas (WSA) +0.39%: 1H20 scorecard which was a beat at the profit line although revenue was slightly below expectations which implies a better operational outcome although need to dig deeper on that. The Interim dividend of A$0.01, fully franked was the 1st interim dividend since 2015!! Strong free cashflow of A$40.6m increasing cash at bank to A$184.9m with no debt. They maintained guidance. We hold WSA in the Platinum Portfolio.

Western Areas (WSA) Chart

Oz Minerals (OZL) -0.30%: FY19 results today and they were a slight miss, about 2% at the profit line with OZL printing NPAT of $164m v $170m exp. The dividend was inline while operating cash flow was very strong at $511m. Cash on hand was also good at $134m. A volatile session today overall, I was surprised to see it up early on however it finished up near unchanged on the day is probably about right. We hold OZL in the Platinum Portfolio.

Oz Minerals (OZL) Chart

Coles (COL) -0.95%: They released a half year trading update just 10 days ago so no real surprises here, although it was still a bit messy given the demerger happened not quite 18 months ago. EBIT for the half was up marginally on a comparable bases to $725m which was a little light compared to market expectations. The supermarket business saw 6% growth at the EBIT line but despite the standout 2nd quarter, the supermarkets business still lags Woolworths in terms of margins which are running at 3.8% vs 4.7% for their main competitor. Liquor was disappointing, as was previously flagged, with EBIT down 10% for the half. The dividend at 30cps was pretty much in line with expectations, as was the result for the most part however there was an underpayments curve ball thrown into the mix, with Coles expecting up to $20m worth of remuneration to be paid in the second half, and that put a dampener on the result and the share price today.

Coles (COL) chart

Abacus (ABP) +3.05%: largely in line result today although the stock traded higher as fears eased around the retail exposure. The office book saw rental growth of 3.2% with a slight increase in occupancy. Self-storage saw revenue per available square meter (REVPAM) up a little over 1% while occupancy ticked marginally higher. Abacus also completed the purchase of an additional $150m worth of assets in the half. The retail book saw significant occupancy growth, up more than 10% to 96.8% though the WACR softened. Overall, DPS guidance was maintained and the market was pleased with the result.

Abacus (ABP) Chart

Stay on top of Reporting Season with live updates

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking the 'CONTACT' button bellow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only

1 topic

9 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Commodities

What ASX rare earths stocks could Trump buy?

Livewire Markets