Beyond earnings torpedoes

Sam Ferraro

Following its 5% to 10% miss on consensus earnings for 1H, Domino’s fell by around 15% from peak to trough last week. The market has little tolerance for earnings misses from growth stocks. Even after the price decline, the stock is still trading on well above 20 times 12 month forward consensus EPS.

A journal article published over a decade ago (Don’t let an earnings torpedo sink your portfolio by Douglas Skinner and Richard Sloan) still resonates today for earnings misses from growth stocks. Their evidence attributed poor returns from growth stocks on average, to an asymmetric market reaction to earnings surprises. Even though growth stocks are at least as likely to report negative earnings surprises as positive surprises, the reaction to negative surprises is much larger. They conclude that investors’ expectations for the prospects for growth stocks are excessively optimistic.

It is well understood that even small revisions to the expected future cash flows for a growth stock has an amplified effect on its price. In this post, Evidente explores another channel through which a growth stock can sink your portfolio; the discount rate or expected returns.

Growth stocks share a key attribute with long dated government bonds; they have long duration in that a larger share of the future cash flows are expected in the more distant future. The present value of those distant cash flows thus accounts for a larger share of a growth stock's price.

In the same way that the price of such bonds is more sensitive to changes in the yield to maturity than for short dated bonds, so growth stocks are more sensitive to changes in discount rates or expected returns than value stocks, controlling for expected future cash flows. Moreover, the math underlying the Macaulay duration formula says that the bond price-yield sensitivity is greater at lower yields. Growth stocks should therefore have higher duration during periods of low expected stock returns or when market sentiment is high.

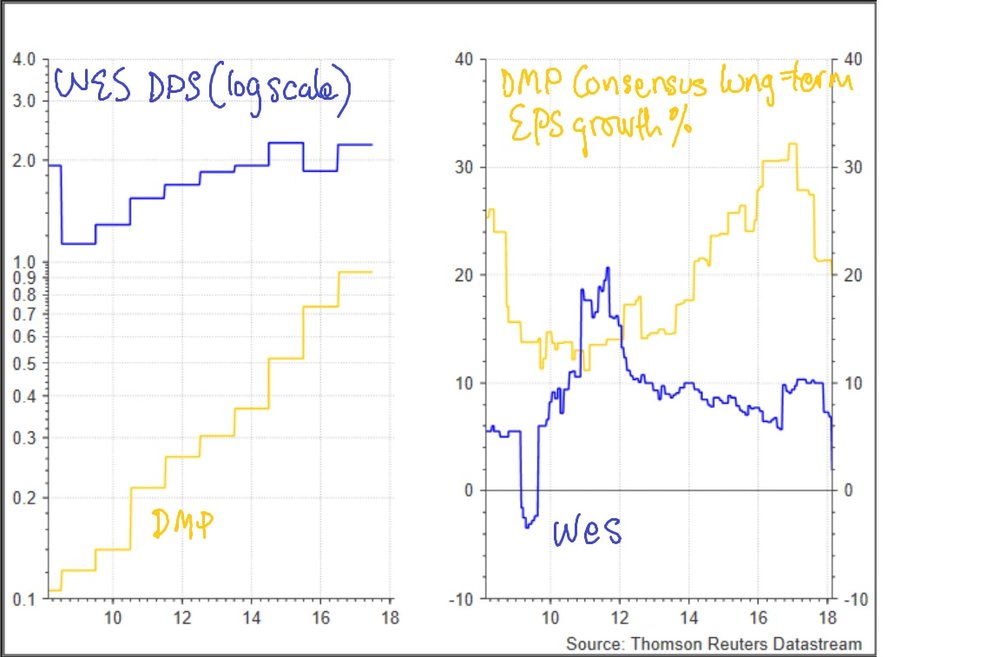

I compare DMP with Wesfarmers, which has a low growth profile. In the past decade, DMP has posted compound annual growth in its dividend per share of over 20% pa well above WES (less than 2% pa); see left panel below. In recent times, both stocks have had earnings misses which have led to analysts downgrading their growth prospects; see right panel below.

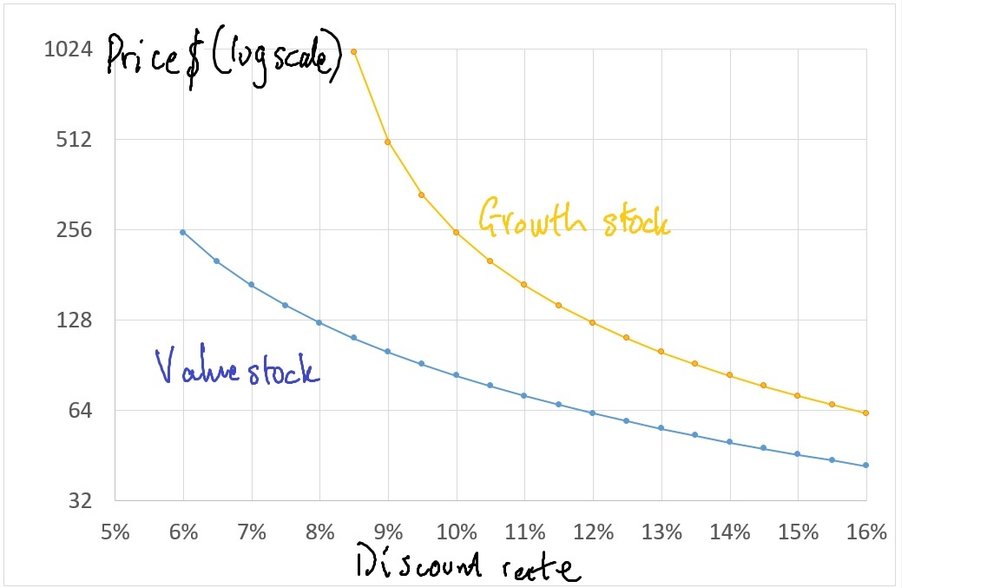

I use the Dividend Discount Model to depict the non-linear, inverse relationship between a stock’s price and its expected return. The perpetuity model says that an asset’s price is equal to the next period’s dividend divided by the discount rate minus the dividend perpetuity growth rate. Both the low growth and high growth stocks are assumed to pay a dividend of $5 in the next period.

For a value stock, a 200 basis point increase in the discount rate to 8% is associated with its price halving to $125. The relationship becomes flatter or less sensitive at higher expected returns; a 200 basis point lift in the discount rate to 16% lowers the stock’s price by less than 20% (see chart).

The steepness of the curve for the high growth stock confirms that its duration is higher, with the yield more sensitive to changes in the discount rate. A rise of only 50 basis points in the discount rate to 9% is enough to reduce the valuation by half to $512. To put the discount rate effect in perspective, subject to the assumptions used for the risk free rate and risk premium, a small rise in the stock’s beta from 0.8 to 0.9 is enough to generate a 50 basis point lift in the discount rate to 9%.

The long duration of growth stocks means that their DCF valuations are awfully sensitive to inputs used, notably expected future growth rates and discount rates. If discount rates are constant, that would not pose as much of a problem. But in my last post which drew on the work of John Cochrane from the University of Chicago, the evidence suggests that discount rates appear to account for most of price variation at the aggregate level, largely thanks to the fact that the market risk premium moves around a lot. Time varying discount rates thus pose a challenge to traditional capital budgeting and stock valuation models based on DCFs because a constant market premium is almost always used (of around 6%).

Mr Cochrane indicates that analysts, portfolio managers and those engaged in capital budgeting massage their cash flow forecasts up in good times and massage them down in bad times, which probably compensates for using artificially constant discount rates. Nonetheless, the fact that discount rates move around quite a bit and growth stock valuations are particularly sensitive to variation in expected returns thanks to their high duration, suggests that the output from DCF models should be treated with a grain of salt.

Insights from behavioural finance and institutional biases can help shed light on why the industry continues to rely heavily on DCFs in their decision making process, despite the sensitivity of inputs used. First, modelling a DCF valuation can offer a sell-side analyst a competitive advantage. A detailed and granular model provides scope for sensitivity and scenario analyses, which some PMs have a strong appetite for. Second, when billions of dollars are at stake, stakeholders assign a greater level of precision to DCF valuations than is warranted. Third, the DCF valuation framework is considered by many to be more intellectually rigorous than other valuation techniques. Fourth, the availability heuristic causes people to turn their attention to what is directly observable. It so happens that the output of the DDM is easy to interpret and directly observable, while discount rates are not. Fifth, the view that a stock has an intrinsic value helps to anchor our expectations and filter out what we consider to be irrelevant information.

At present, growth investors should be particularly cautious because the expected market return from the ASX200 appears to be low by historical standards (see chart). The fact that the expected return is comparable to the levels that prevailed during the credit boom suggests that market sentiment remains bullish despite the recent market turbulence. For investors in stocks like DMP, not only do they need to be cognisant of revisions to future growth prospects (ie. earnings torpedoes), but they should also be wary about spikes in the market risk premium. This probably represents the main channel in which growth investors should think about how macroeconomic developments can influence their portfolio construction.

Market reactions that exceed the size of the negative earnings surprise for growth stocks such as DMP, reflect a downgrade to the stock's future growth prospects but also likely a lift in expected returns. As this post has shown, even a small rise in the discount rate for high duration assets can have an amplified effect on their price. Against this backdrop, such price reactions do not necessarily represent strong buying opportunities.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Sam Ferraro,

2 topics

2 stocks mentioned

Sam Ferraro

Expertise

Sam Ferraro

Expertise

Comments

Comments

Sign In or Join Free to comment