BHP: ‘$40 over the next few years’

On Tuesday, we hear from the fifth biggest stock on the market, BHP. In this wire, we select of a few notable views from the brokers including a big call from Shaw and Partners’, and provide some recent commentary from Livewire contributors on the ‘The Big Australian’.

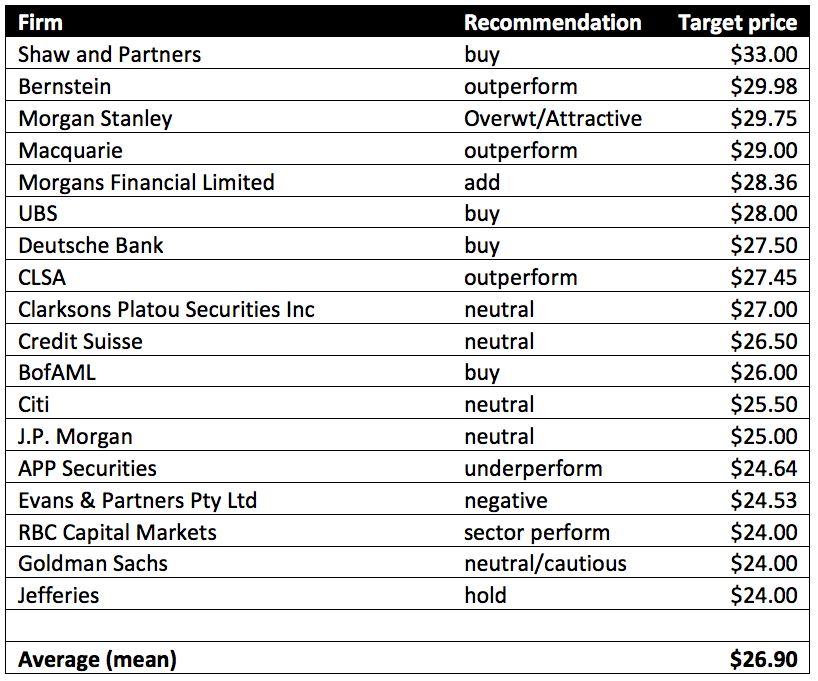

Source: Data from Bloomberg

What the brokers are saying

The mean price target across Bloomberg's coverage of brokers is $26.90, which is 5.0% above the current price of $25.62. There are a few outliers at the top end of the range, with Shaw and Partners as the most bullish on the street. They give a $33 target, but call for ‘$40 over the next few years’ in a recent report that cited five key reasons for their view.

Firstly, historical precedent: "BHP has been in a tight corner before – the mid-1980’s and again in the late 1990’s – with these precedents highlighting an element of déjà vu." Secondly, the upside scenarios of its 4 'crown jewel assets' (iron ore, copper, energy, met coal). Thirdly, delivering greater return on invested capital by addressing underperforming assets. Fourthly, they argue that divestments are expected to continue or even ramp up.

Lastly, the market conditions are on BHP's side: "Current favourable economic activity - the most synchronised for a decade or so yet the least dependent on China – should translate to improved market balances and by extension commodity pricing. We see this particularly in copper and oil markets whilst iron ore and coal prices are likely to see upgrades vs very low consensus pricing decks."

Also at the upper end of the range, Macquarie has a $29 target, recently focusing on the Spence system: “Approval of the Spence Growth Option extends the life of the Spence system by 50+ years and is the first step in BHP’s strategy of unlocking latent capacity within its existing assets. The extension project does not meet a 15% IRR on our forecasts and contributes immaterial NPV to our group valuation. However, we note that significant upside to our valuation and estimates exists under a more bullish (US$3.00/lb) long-term copper price scenario, under which we value the Spence system at ~US$1.8bn.”

Morgans is relatively bullish, with a target of $28.36, and recently highlighted key candidates that may surprise or disappoint during the upcoming August results season, highlighting potential for positive news around capital management from BHP (BHP): (VIEW LINK)

Goldman is close to the bottom end of the range, but has recently increased the target to $24 (from A$22.50) following the June quarterly results and currency and commodity deck update.

BHP would be worth more as a group of midcaps

Martin Conlon, Head of Australian equities at Schroders Australia, reiterates his bull case for resources at Livewie Live 2017: “For the most part, we still think that’s where the best value is in the market. Price to book and other measures, would all tell you there’s no way these things are expensive versus history. You are still buying the best resource companies at 1.5 to 2.0 times book value. There is no way that is super expensive”:

On the subject of small caps, he argued that investors are moving down to the small end of the market ‘to get their risk’, leaving the opportunities at the big end relatively unappreciated. Posing the question of what would happen if BHP was broken into a suite of South 32’s, he told the audience: "Like South 32, there’s more appetite for the smaller things. I guarantee that for the most part that if you broke up the conglomerates into smaller companies, most of them would go up."

What could activist investors mean for BHP?

Matt Haupt from Wilson AM recently posted a video on Livewire discussing the implications of Elliott Management’s recent proposal for BHP: "Elliott Management has proposed a collapsing of BHP's dual-listing structure in the UK and divestment of its onshore oil and gas assets in the US. We believe there is merit to Elliott Management's proposal, and if BHP were to act, it would create an opportunity for franking credits to be delivered to shareholders.": (VIEW LINK)

Is the sector finally hotting up?

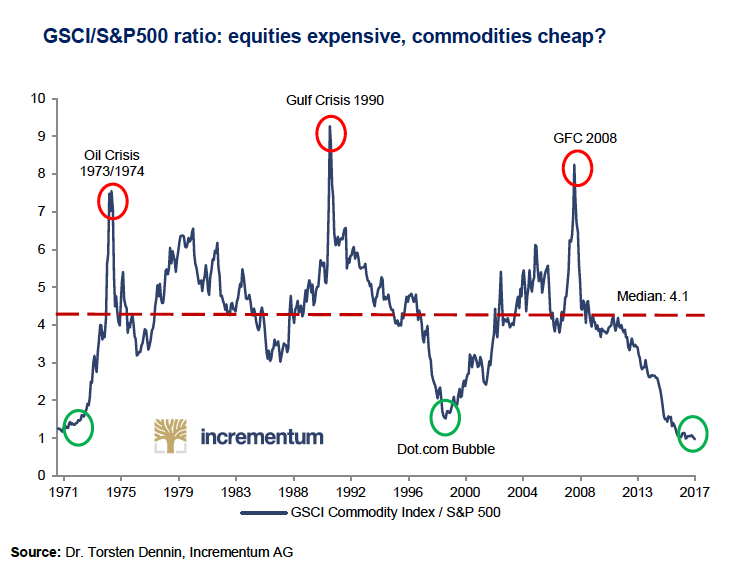

James Gerrish from Shaw and Partners / Market Matters also asked if the sector was turning a corner, a few months ago: “According to a number of different measures, commodities are now cheap, in fact they are the cheapest they have been relative to the S&P 500 in history". On BHP, he wrote: "We hold BHP from ~$24, which in hindsight was a tad early, however we remain comfortable with our 7.5% holding" (VIEW LINK)

Subscribe to Livewire

Join 65,000 other Livewire users by subscribing at no cost here, and also receive the 'Trending on Livewire' email each morning at 7am: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

1 stock mentioned

3 contributors mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment