Central banks banking governments

Central banks globally have clearly been buying a lot of government bonds over the last decade. But just how much the world’s central banking powers own of their own government’s stock of financial obligations is astounding. And that includes the US Federal Reserve.

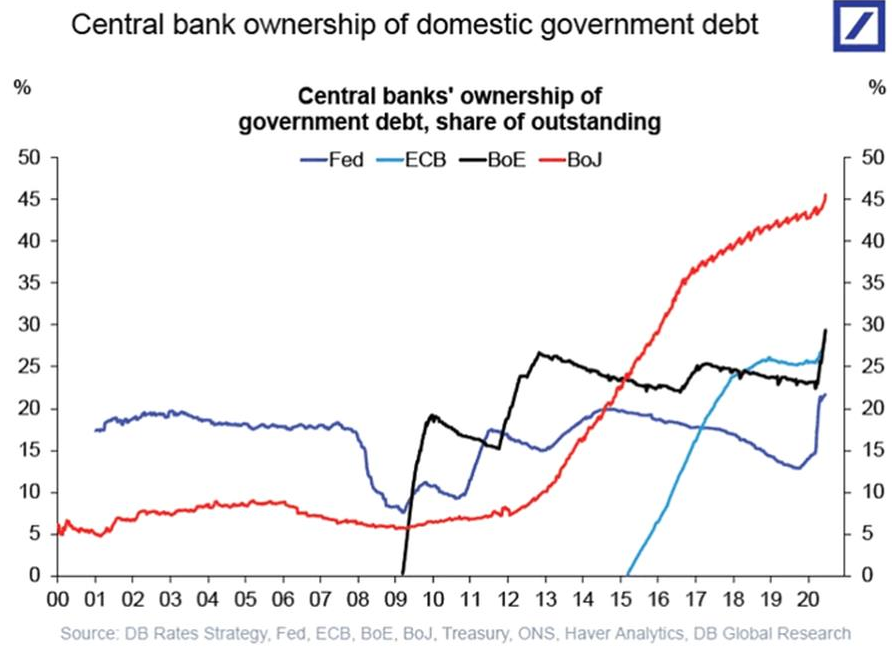

Last year when we spent time in various cities and regions talking to clients, advisers, and friends, we would point to Japan as a case of a central bank becoming extremely involved in the financial markets. In particular, the Bank of Japan (BoJ), was the largest owner of Japanese government bonds and equity exchange traded funds (ETFs). This situation has become even more extreme this year and the BoJ now owns close to half of the government’s debt.

But BoJ’s friends around the world are catching up. The European Central Bank (ECB) and Bank of England (BoE) have increased their respective holdings of government borrowings to 30%, up from low 20% levels earlier this year.

Perhaps the most remarkable move has been in the US. The US Federal Reserve (Fed) owns almost a quarter of the US government’s obligations, around double the level it started the year. That comes after the Fed’s influence in the US government bond market had been steadily decreasing for more than five years.

When the central bank steps in to buy the risk-free asset in an economy, private investors trade their holdings for cash. That cash must be redeployed, and it finds its way into risk assets, first corporate bonds (which the Fed is also buying) and then it can leak into equities. While we remain concerned about the potential for a strong economic rebound, there are other market participants that vehemently argue a “V-shape” recovery is happening. The resolution of that debate may not matter nor be driving markets now. The flood of central bank liquidity has proven far more powerful in the short term even if we believe economic fundamentals remain highly uncertain with the potential for continued repression. We think it is prudent to stay cautious and patient, including employing capital protections in our strategies for our investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Christopher is a co-founder and portfolio manager at Montaka Global Investments. Before establishing Montaka in 2015, Christopher has worked with LFG, the Lowy family's private investment firm, One East Partners and Goldman Sachs.

3 topics

1 stock mentioned

Christopher is a co-founder and portfolio manager at Montaka Global Investments. Before establishing Montaka in 2015, Christopher has worked with LFG, the Lowy family's private investment firm, One East Partners and Goldman Sachs.

Christopher is a co-founder and portfolio manager at Montaka Global Investments. Before establishing Montaka in 2015, Christopher has worked with LFG, the Lowy family's private investment firm, One East Partners and Goldman Sachs.

Comments

Comments

Sign In or Join Free to comment