Commonwealth budget tracking better than the government’s forecast profile

Authored by Kieran Davies, Coolabah Capital Investments.

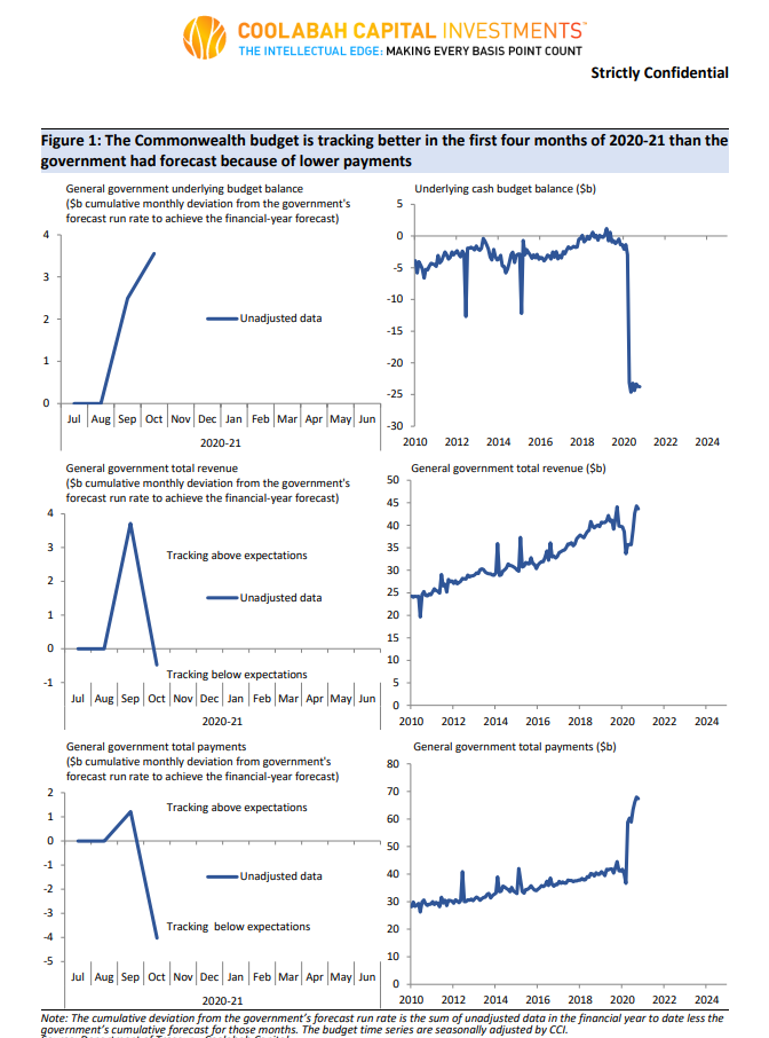

In this new report, we review our real-time tracking of the Commonwealth budget. Treasurer Frydenberg is expected to publish a budget update this week, with the Mid-year Economic and Fiscal Outlook (MYEFO) reportedly due on Thursday. Treasury’s strong preference would be to publish no change to the outlook given the full budget was released in October, but we think it will trim its forecast for an underlying cash deficit in 2020-21, revising it by about $11bn from $214bn to around $203bn (or from 11.0 to about 10.4% of GDP), with an additional windfall in 2021-22 if iron ore prices stay high.

The anticipated revision reflects the net of:

- A better-than-expected starting point of about $3.5bn. On CCI’s seasonal adjustment, the underlying budget has averaged about $24bn per month in the four months to October and is tracking about $3.5bn better than the government had expected. This reflects underspending across nearly all types of expenditure, with welfare payments peaking in July and grants and subsidies looking to have peaked in September. Revenue has rebounded to pre-virus levels and is broadly in line with government expectations.

-

A large $9bn windfall from an improving economy with less spending on the JobKeeper welfare payment. The JobKeeper payment was estimated to be paid to about 4 million recipients by Q3 2020, 2.25 million by Q4 2020 and 1.75 million by Q2 2021 at a cost of $65bn for 2020-21 as a whole. However, the treasurer recently said that about there were 0.7 million fewer participants than expected in October. Assuming this improvement is maintained into Q1, it would reduce the total cost of this key stimulus measure by about $9bn for 2020-21.

- Windfall company tax of $1.5-2bn from high iron ore prices. The price of iron ore is near $US150/t, well above the budget’s conservative assumption that it would fall to $US55/t by Q2 2021. If the MYEFO assumes a similar rate of decline from this higher starting point then iron ore would deliver a windfall company tax gain of about $8bn (the windfall is tempered by the recent appreciation of the exchange rate). This would boost taxes by about $1.5‑2bn in 2020-21, with the rest paid in 2021‑22. There should also be a minor windfall from higher than assumed prices for LNG producers.

- A temporary increase in spending of about $3.5bn. There are increased costs from the extension of the JobSeeker Coronavirus Supplement to welfare recipients and the HomeBuilder subsidy for the housing industry to Q1 2021. The extension of the welfare supplement should cost $3.2bn, while the housing subsidy costs around $0.2bn.

While mindful that some of the underspend in early 2020-21 could reflect timing issues given the sheer scale of the government’s fiscal stimulus, CCI’s tracking and seasonal adjustment of the monthly budget data suggests there is a risk that the deficit turns out better than the expected MYEFO revision, barring a setback on the health front. On the downside, Australia’s trade relationship with China continues to deteriorate and creates additional uncertainty around the outlook for trade and the broader economy. Once the MYEFO is published, the Australian Office of Financial Management should update its funding task for 2020-21, where it previously estimated Treasury bond issuance of around $240bn.

Download the full report here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

1 topic

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment