Defensives: Perception vs Reality

Are Australian bond-like proxies going to suffer a bondcano moment? Certainly, stocks that have defensive characteristics have been sold down in recent months. And bond bears would have it that they are collateral damage from rising US yields. However, we believe this is a false narrative. Hence, we need to go back to first principles to sort out perception and reality.

The valuation of domestic cashflows are not based on overseas interest rates

In recent months, the aggressive sell-off in Australian bond-like stocks looks like they are more correlated with the rising US bond yields rather than Australian bond yields. Fundamentally, this should never happen.

No rational investor would buy an Australian asset and fund it with US debt. Otherwise, there is a huge basis risk in terms of the cash flows generated from an asset in one country and the finance cost associated with another country.

US interest rates drive US asset valuations.

Australian interest rates drive Australian asset valuations.

Zimbabwean interest rates drive Zimbabwean asset valuations.

You get the idea.

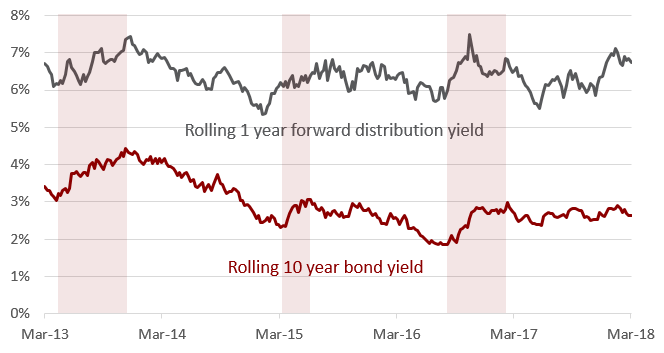

To illustrate how Australian interest rates affect the pricing of Australian bond-like stocks we use Spark Infrastructure (SKI) as an example. The chart below plots the rolling 1-year distribution yield of SKI against the Australian 10-year bond yield over the last five years. Given the heightened fear of an Australian bondcano event in recent months, we have also shaded historical bond sell-off periods (light red) to provide perspective.

Chart 1. Spark Infrastructure 1-year forward distribution yield versus Australian 10-year bond yield

Source: Factset

Historically, when SKI’s yield was rising (that is, share price was falling) it mirrored rising Australian bond yields. This implies that the stock market is not very good at forecasting, but is generally good at marking to market with interest rates in real time. This is a hallmark of an efficient market.

However, for the first time in five years SKI’s yield has skyrocketed while there is no evidence of an Australian bond sell-off. Is this an example of an efficient market or a mispriced opportunity?

Our view is that SKI’s valuation being priced off US interest rates is fundamentally incorrect.

On a technical note, the bond experts will recognise that SKI’s cash flows resemble a variable interest rate security. If you believe interest rates are going to rise in the future then SKI future cashflows will also rise. Given that SKI owns monopoly assets, the regulator sets its cash flows based on a return on capital that is largely influenced by interest rates. The valuations of variable interest rate securities simply should not change that much from interest rate movements.

Valuations are not solely driven by the interest rate

With so much media attention on interest rates (risk-free rates), many commentators are confusing risk-free rates with discount rates. Valuations are driven by an asset’s discount rate which is comprised of two components: the risk-free rate and a risk premium, where the risk premium reflects the riskiness of cashflows given that assets are not riskless.

Changes in both interest rates and risk premium drive valuations, not just one of these in isolation. Sure, rising interest rates will put upward pressure on the discount rate but if it is countered by a wide and shrinking risk premium then valuations can be preserved.

Alternatively, if risk-free rates are benign and the underlying asset yield rises it implies the risk premium has expanded. The million-dollar question for investors is whether the wide risk premium represents a disconnect between perception and reality of greater risk.

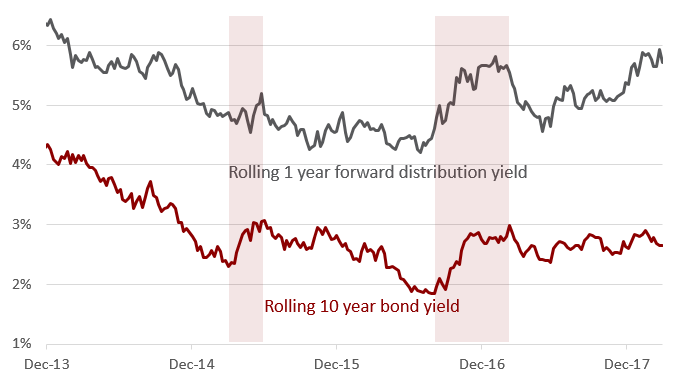

Let’s use another bond-like stock, Sydney Airport (SYD), as an example. The following chart plots the rolling 1-year distribution yield of SYD versus the Australian 10-year bond yield since its corporate restructure from Macquarie Airports in late 2013.

Chart 2. Sydney Airport 1-year forward distribution yield versus Australian 10-year bond yield

Source: Factset

Like SKI, the recent rise in SYD’s distribution yield also looks like SYD’s share price has been priced off US interest rates, which we know is fundamentally incorrect. The recent sell-off has been so dramatic that the yield spread is at the highest level over the last five years.

Chart 3. Sydney Airport yield premium versus Australian 10-year bond yield

Source: Factset

The only feasible explanation for SYD’s widening yield premium is that the business may be under stress. The first thing that came to our mind regarding risk was SYD’s gearing levels given its historical relationship with Macquarie Bank. Maybe SYD’s balance sheet under pressure?

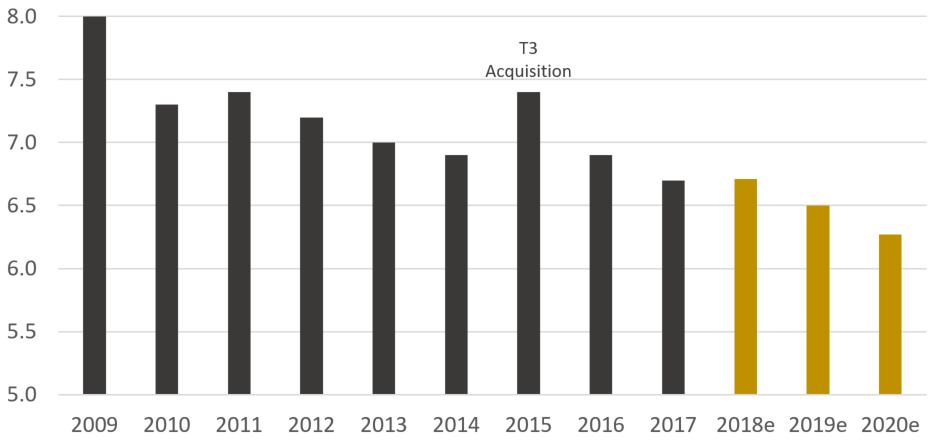

Chart 4. Sydney Airport net debt / EBITDA ratio

Source: Factset

SYD used to be highly geared when it was owned by Macquarie Bank. Not anymore. Over time its leverage ratio has been falling and is expected to continue in the future. The improved balance sheet has been confirmed over the last few months by Moody’s and Standard and Poor’s which upgraded SYD’s credit rating to Baa2 and BBB+ respectively. If the deleveraging continues SYD will be on a path to receive an A credit rating by early 2020s.

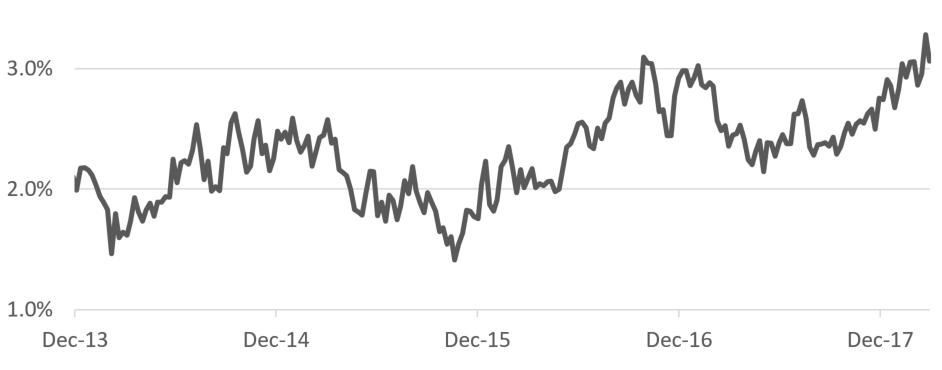

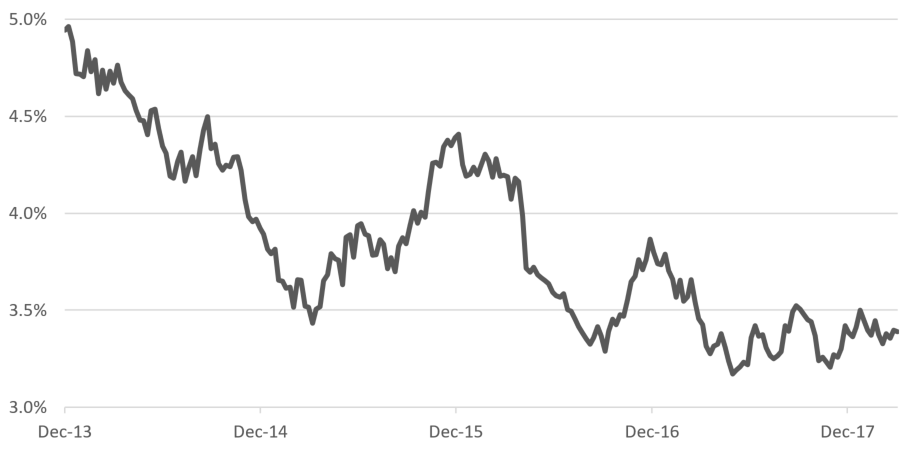

Maybe debt funding costs have skyrocketed? Like Australian bond yields, Australian BBB corporate interest rates have fallen over time and has been relatively benign over the last few months.

Chart 5. S&P/ASX Corporate Bond BBB interest rate

Source: Factset

Further, SYD’s debt refinancing risk is low because there is no significant debt maturity in the next couple of years. As a sign of conservative management, SYD is paranoid about managing its debt. To ensure that its average debt maturity is long dated (around 8 years) and most of the interest rate risk on their debt is hedged (about 93%) they purposely overpay on their debt cost (5% interest rate versus the equivalent Australian BBB interest rate of 3.4%). Not many companies take an extremely long-term view on managing their debt.

In summary, when leverage ratios are falling with a benign debt funding environment, risk also reduces. Bond experts will recognise that securities which are deleveraging command a shrinking risk premium.

If the balance sheet is not under stress, maybe the high yield premium is due to the growth outlook deteriorating?

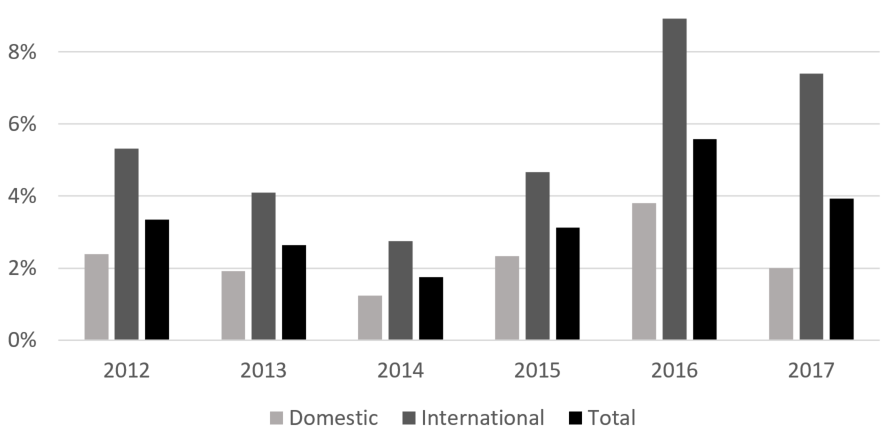

SYD’s profitability is directly linked to the number of passengers traveling through the airport.

Chart 6. Sydney Airport passenger growth

Source: Sydney Airport

Prior to 2016, total passenger growth was growing around 3% per annum. From 2016, total passenger growth was +4% per annum. The step change in growth has predominantly been driven by international passengers. The elevated passenger growth over the last couple of years have driven EBITDA growth by 9% per annum.

There is a lot to like from SYD’s exposure to future passenger growth. And the outlook has become clearer and better since 2015 for four main reasons.

1. China

China’s recent five-year (2016-2020) plan highlights 50 new airports to be built including Beijing’s new mega airport, which is due to open in 2019. More airports will allow the growing Chinese middle class a greater opportunity to travel. With 10% of Chinese nationals holding a passport it highlights significant untapped travel demand.

Over the past five years, Chinese visitors have consistently grown by more than 15% per annum and now represent about 8% of SYD’s total international passengers. Importantly, China and Australia signed an open skies agreement in 2016, which means that current passenger growth from China is likely to be sustained.

2. Terminal 3 (T3) optimisation

SYD has three terminals where terminal 1 (T1) is dedicated to international travel and terminal 2 (T2) and 3 (T3) are dedicated to domestic travel. In 2015, when SYD bought Qantas’ T3 lease it was processing about 10 million passengers versus 15 million passengers travelling through T2. In our view, there is enormous scope to increase T3’s asset utilisation.

3. Terminal 4 (T4)

SYD has proposed a new terminal, T4, which is expected to be built around mid-2020s. Qantas is expected to operate both its international and domestic services from T4. Hence, the new terminal will free up valuable capacity in T1 for more international passengers.

4. Western Sydney Airport (WSA)

WSA is expected to be built by the mid-2020s and serve around 3 million passengers (in comparison SYD served 16 million international and 27 million domestic passengers in 2017). Notably, around 80 percent of WSA passenger demand would be for domestic use.

On the surface, it may seem like a competing airport would crimp SYD’s profits. However, SYD suffers capacity constraints during peak periods. Hence, by diverting domestic passengers to WSA, SYD can free up valuable capacity during peak times for more international flights.

With a growing mix shift to international passengers, SYD’s operating outlook is brighter than ever. In the long term, it is foreseeable that SYD could process more international passengers than domestic passengers. It’s not hard to do the maths on SYD’s future profitability when international passengers deliver 4x more revenue than domestic passengers on a largely fixed cost base. Given the leverage to international passengers, by the time WSA is built SYD’s future profits could be double last year's profit.

With a stronger operating outlook, SYD’s yield premium over bonds should at the very least narrow not expand.

To sum up, in early 2014 when Australian bond yields were around 4%, SYD had a 6% distribution yield but had a weaker balance sheet and tepid growth expectations. Currently, Australian bond yields are under 3% compared to SYD offering a similar yield of 6%, but with a strengthening credit and operating outlook.

Can you spot the disconnect between the perception of fear and the business reality?

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

4 topics

2 stocks mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment