Was January 26 the cycle peak?

Vimal Gor

Pendal Group

There are two attitudes you can take to the February 2018 “flash crash”. The first, and overwhelmingly the most popular, is that this was a technically driven correction in the markets, exacerbated by carry monkeys such as the short-VIX crowd, and that the pause since then has provided a refresh in a bull trend that remains well and truly intact. The second view, and much closer take to ours, is that the highs seen in the S&P 500 index on 26th January will be the highs of this cycle and the ensuing volatility marked the beginning of a protracted period of adjustments needed to realign asset valuations with a new reality.

I suppose there could be a third attitude which is that the February crash signaled “game over” and equity markets are going to be taken round the back of the bike sheds for a kicking, and normally I would be the first to voice that position, but not right now. Not yet.

As Q1 drew to a close, we were hearing a mix of optimism and caution among our client base, with questions ranging from “shouldn’t you be less bearish given the tax deal struck in the US?” to “why has LIBOR-OIS widened to crisis levels and does this mean we’re on the doorstep of the next market meltdown?” Certainly a lot has happened over the last three months, some of which have been obvious (US tax reform) and others less so (LIBOR-OIS), and a lot is still going on (threat of trade wars, Facebook probes). In this month’s newsletter, I’ll try to piece together the bigger picture as we see it, what it means for markets and asset allocation, and how we’ll position for our views.

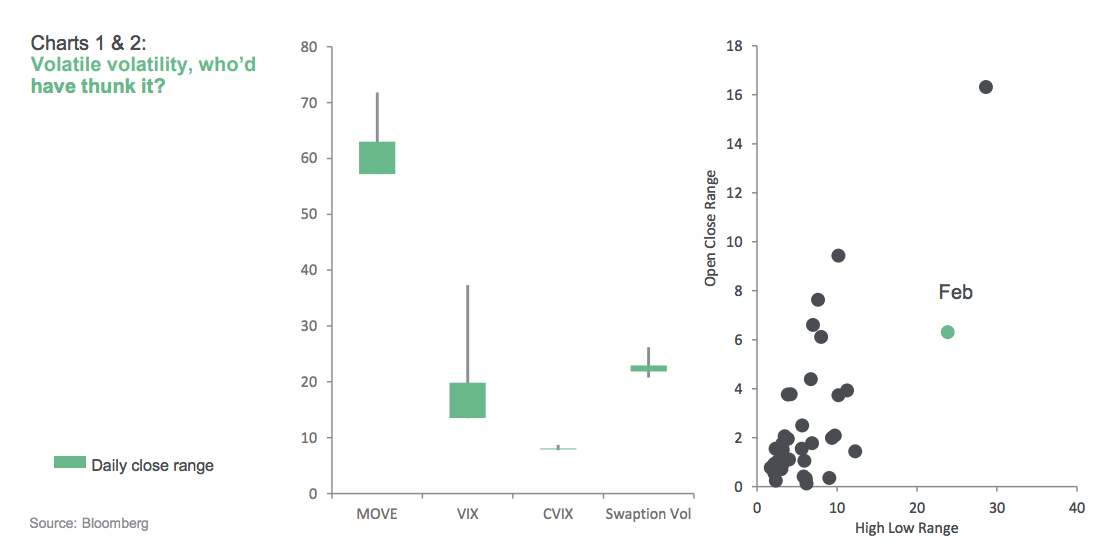

For a short while after the February sell-off, the market was back in buy-the-dip mode. This mentality can be seen in the disparity between large intra-month ranges in markets versus small open-close ranges of the month. Even the VIX, which saw intraday highs in the 50s, ended the month only around six points higher than where it had started.

Against market consensus we viewed the February market moves as a foreshock before the main earthquake. This view is being backed up as new sources of volatility have emerged over the course of this month, including new trade tariffs which prompted Cohn’s resignation, Tillerson and McMaster being told “you’re fired!”, and renewed instability led by the FAANGs. But one way or another, we think the S&P would have eventually found its way back down to the key technical levels on which it is now poised.

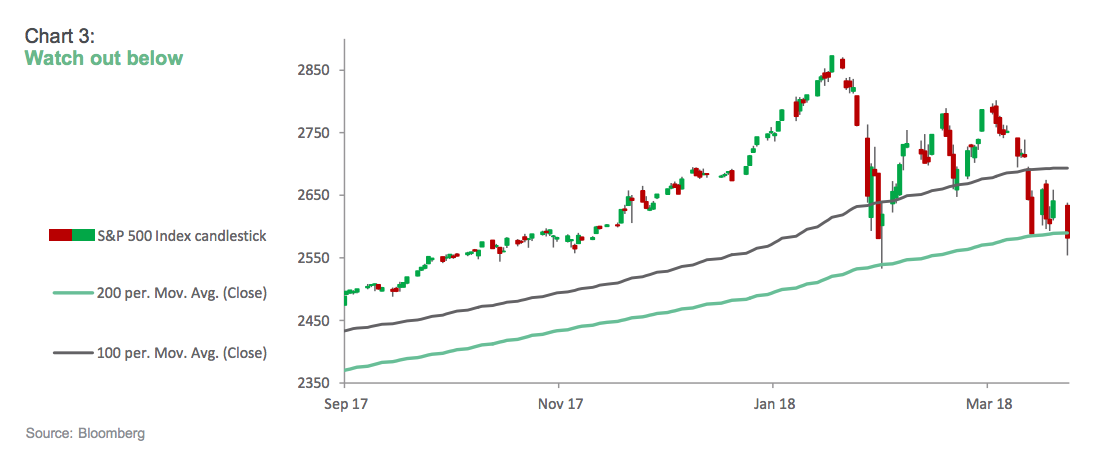

Chart 3 shows that despite the February dip being bought, the subsequent rally has failed. The market’s near-term focus has shifted from looking for the next new high to wondering whether the technical supports will hold (as at time of writing on Tuesday 3rd April, they look like they have broken). Also different to February, larger intra-day ranges are being accompanied by larger high-close ranges, which is typical of a rising volatility environment.

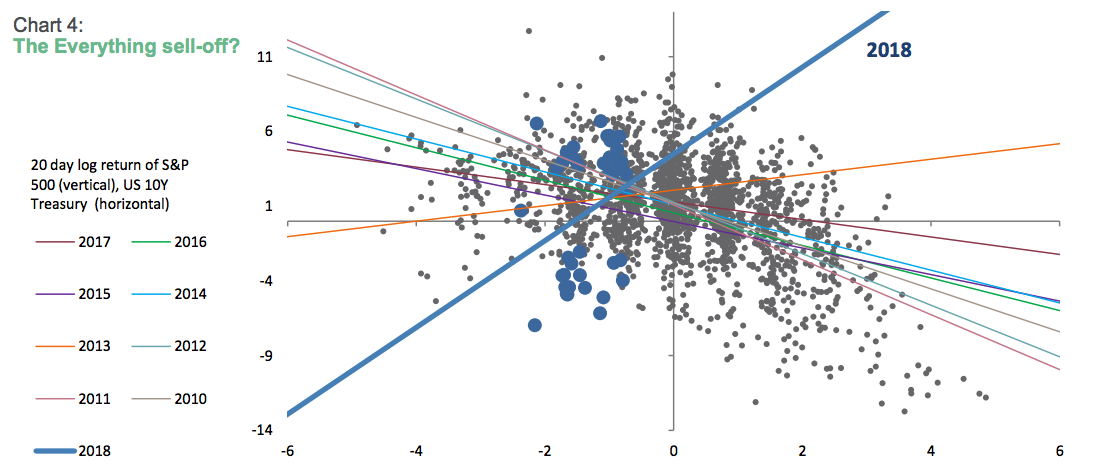

But those who rush to bonds for protection are facing an added challenge. As chart 4 shows, for most of this cycle, bond and equity market moves have been negatively correlated with each other. The exception was 2013 and the explanation was the Taper Tantrum. This correlation has flipped to positive in 2018, leaving no place to hide for a traditional balanced portfolio. In this new environment volatility, as an asset class, is the only clear winner.

In a way, 2018 is experiencing Taper Tantrum II, a supercharged version, as not only are central banks stepping back from extraordinary liquidity provision, they are also trying to normalise interest rates. The US Federal Reserve’s interest rate hiking cycle is well and truly underway because the economic picture clearly justifies it. Other central bankers are getting anxious not because their economies are in danger of overheating, but because when the cycle turns (led inevitably by the US), they are going to need some dry powder in their policy tool box.

The return of volatility looks to be inevitable

Regular readers will know that we have been calling for a normalisation from the extreme (low) volatility environment for some time. We were too early initially, and last year, we found a smarter way to structure our positioning for this view that afforded us the ability to wait it out. This is important because such views are difficult to time, but our investors rely on us to not only grow but also to protect their assets. If we’re late, we might as well go home.

Chart 5 shows the main reason for our belief that volatility is headed higher. While the market focus is on central bank’s rate hikes, our interest is on the action in the balance sheet. Here central banks are taking away the punch bowl, be it the sell-down of the Fed’s balance sheet or the reduced pace of buying from the ECB and the BoJ. As we’ve shown previously, changes in this global liquidity picture is closely mirrored in market volatility.

The intuitive explanation for this relationship is that through the deployment of their balance sheets in massive size, central banks implicitly provided a “put” for asset valuations, whose strike price is only very slightly out-of-the-money. When central banks become the marginal buyer in the market on government and mortgage-backed securities, private investors are crowded out and down the risk curve.

This is the much-lauded portfolio rebalance effect, and it pushes up asset prices on all other investments until their yields converge on the riskfree rate. Obviously, this pushes end investor’s portfolios further and further out the risk spectrum, as they chase falling yields, due to the lack of moral hazard in the market.

Not only is it economically appropriate right now to wind back this extraordinary liquidity provision, it is vital if central banks want to re-establish their role as lenders of last resort. Central banks should absolutely step in to end a crisis but they should also not get in the way of a normal economic cycle. We strongly believe that the central bank put should be much further out-of-the money and we think that’s a view that’s shared by the new Fed Chairman, Jerome Powell.

The low volatility picture has also been helped by incredibly benign inflation outcomes. When inflation is low and stable, it is a sign that there is a high degree of economic certainty, which is a necessary ingredient to feed risk appetite.

However, inflation expectations are starting to tick higher (at least in the US) and coupled with the likelihood of seeing a net drain on global liquidity by early next year, the return of volatility looks to be inevitable to us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

3 topics

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Commodities

What ASX rare earths stocks could Trump buy?

Livewire Markets