Fallen angels and upside surprises

While the month-end reports for February will indicate the ASX Small Ordinaries finished the February reporting period dead flat, it would be difficult to find any smaller cap investors this month that would summarise the reporting period as dreary.

While global equity markets faced their own return to a ‘more normalised’ level of volatility through the beginning of February, the ASX reporting season in the small and mid-cap space served up some equally sizeable price action movements of its own.

Within the small and mid-cap space this reporting period, the majority of companies that experienced fairly material share price movements could ultimately be categorised into one of three broad categories:

1) ‘Low Expectation’ Businesses Delivering Upside Surprise

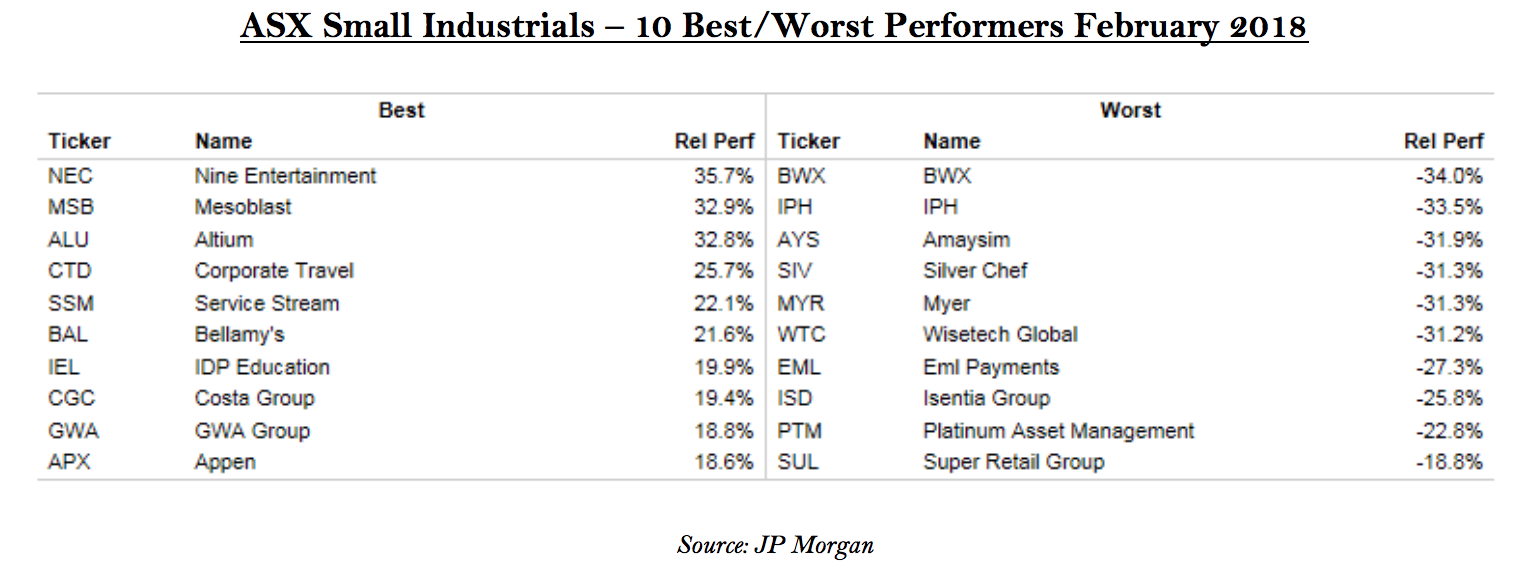

The bulk of businesses in this group generally entered the reporting period with relatively low overall growth expectations, either as a function of operating within more structurally challenged industry sectors or being broadly recognised as a business in the more mature, lower-growth stage of their corporate lifecycle. As a consequence, valuations of these businesses are typically below the average market multiple and the growth hurdle required to generate a re-rate in their underlying valuation is equally fairly low. This season saw re-rates from a number of these businesses including Nine Entertainment, GWA Group, The Reject Shop, Accent Group and HT&E.

We typically see more of these ‘lower expectation’ names aggressively re-rate at the later stages of a market cycle when market valuations are already stretched and the market is struggling to find options to deploy capital into more traditional value-type companies. While quality of business is often compromised in this later stage, the re-rates experienced by a number of these businesses following slightly better than expected outlooks can be fairly stellar. Nine Entertainment, for example, saw its market capitalisation increase by more than +35% this month after reporting top line revenue growth of +9.7% - its first positive uplift in revenues in two and half years.

We are expecting this trend toward the lower quality/value end of the market to continue to some degree this year. Ultimately a good number of these businesses aren’t overly well-owned institutionally, are not demanding from a valuation perspective and, in some cases, are demonstrating the ability to string together some degree of earnings momentum – a characteristic that the market continues to be prepared to pay increasingly higher multiples for.

Of course, expectations work both ways and a reasonable collection of smaller cap growth businesses that came into February with high expectations for continued growth ultimately missed these hurdles and were dealt with severely. Organic skincare manufacturer BWX Limited, for example, saw its share price fall -34% over the month after posting revenue growth of +79.2% for the half (the market broadly unimpressed with some early signs of compression in overall gross margins).

2) The ‘Fallen Angels’

The BWX experience fits neatly into the second category of ‘Fallen Angels’ – essentially higher growth / higher PE businesses that for a long period enjoy widespread market support and an equity valuation that assumed significant continued growth for multiple periods to come. An unfortunate part of the equity market cycle for these businesses is ultimately growth rates taper and the flood of growth capital that had chased the earnings growth momentum then aggressively tends to move on equally quickly.

This season saw a number of Angels fall back to earth, the most obvious casualties being Domino’s Pizza (-18%), WiseTech Global (-31%), IPH Limited (-35%) and the aforementioned BWX. While valuations can compress rapidly in these stocks, we tend to steer clear of trying to pick a near-term bottom of the share price through these de-rating cycles, even if the future earnings stream becomes available at a vastly discounted prices to just one month prior. In our experience, it is very difficult to gain a sense near-term of where the broader market will ultimately re-base earnings expectations (and the appropriate multiple one should be paying for those earnings near term) and, as a consequence, we can find ourselves in the situation of ‘trying to catch a falling knife’.

These businesses also unfortunately have a tendency to then ultimately suffer from the Australian ‘tall poppy’ syndrome where any number of media commentators, short sellers and others will gather vocally to kick in the proverbial boot on the way down. The Australian market appears to relish the tribulations of a fallen champion and in many cases the next wave of negative press involves forensic analysis of CEO remuneration structures, board disputes, personal share sales or operational issues that aren’t overly material to group earnings but nevertheless garner headlines. That is a difficult situation for us to want to get involved and we tend to simply keep a watching brief on these businesses until the near term noise subsides.

3) The Rich Get Richer

This hasn’t been a season, however, where simply lower-quality value businesses have re-rated and high expectation businesses have sold off – at the other end of the spectrum has been the collection of high growth businesses that delivered on their underlying expectations and subsequently enjoyed a further expansion in multiple and share price. We witnessed a number of examples this month of expensive businesses growing even more pricier as continued earnings growth drove valuations even higher. Members in this camp include the likes of A2 Milk (+47%), Altium (+33%), IDP Education (+28%) and Corporate Travel Management (+26%), all of which reported stellar results this month.

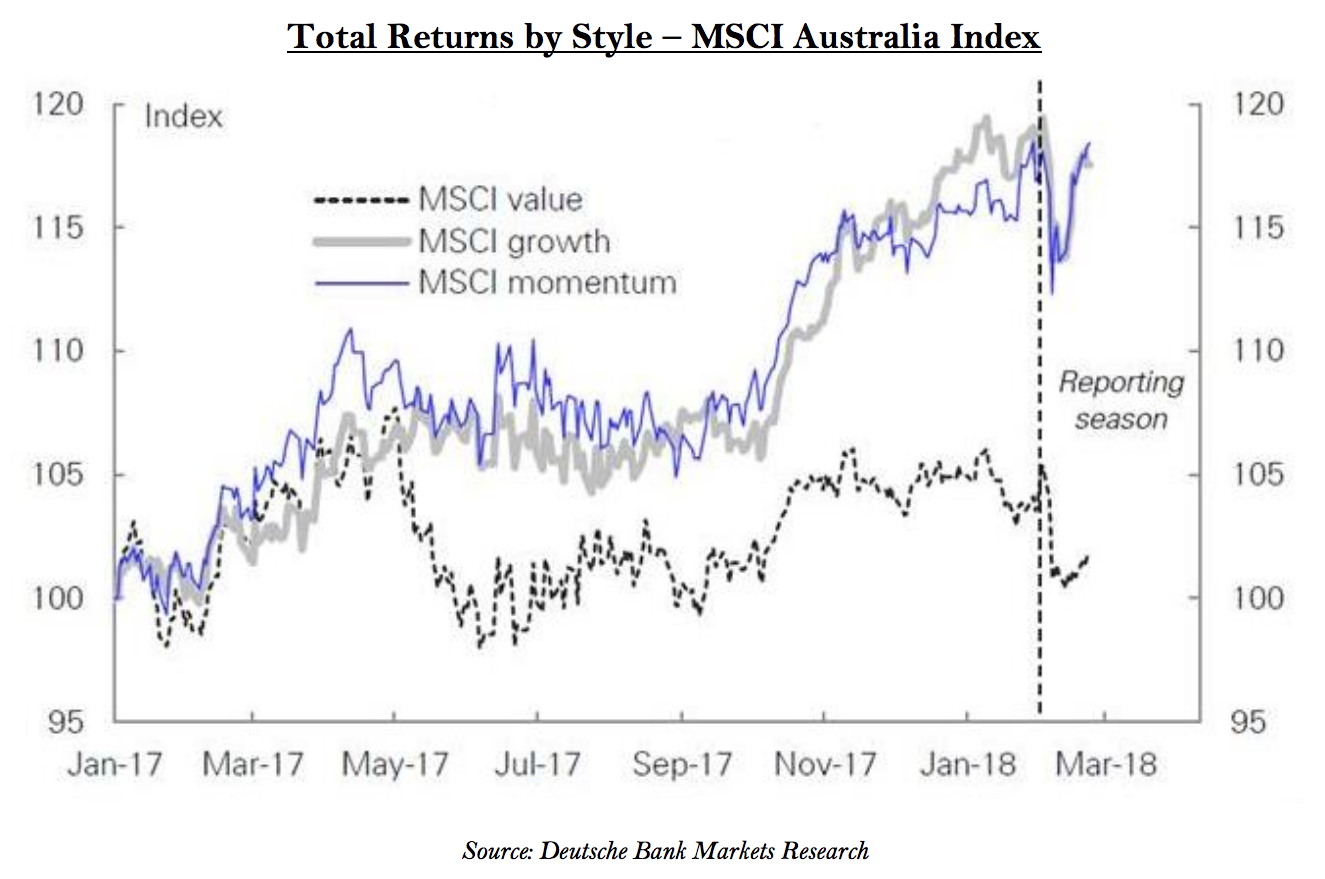

The delivery of earnings growth is continuing to be very much rewarded in this market and, in some cases, aggressively so. Ultimately the Australian market has completely reversed the impact of the ‘Reflation Trade’ of 2016 where higher growth businesses had been sold off in anticipation of a rally in lower-quality cyclical businesses as global growth rates began to climb. What has likely caught a number of market participants by surprise is the resurgence back towards growth businesses at the exact same time as the global growth thesis comes into fruition. Growth, as a style, has largely shrugged off the recent rise in Australian and US bond yields in recent weeks and continues to be well supported by the market.

Indeed, while equity markets globally were sold off at the start of the month in response to rising inflation expectations (the sell-off occurring largely irrespective of sector, company or style grouping – we discussed these ‘low dispersion of returns’ in our January Letter), the vast bulk of higher growth names in Australia ultimately regained their footing quickly through the month, recouping the vast bulk of losses experienced in the opening weeks. Somewhat surprisingly, it has been the cyclical and value businesses that have broadly lagged in performance, despite confirmation of an arguably higher inflation environment.

The learnings of the experience of all three categories above is ultimately the market continues to heavily favour earnings momentum wherever it can find it (though it will be equally quick to move on once the momentum turns). While the overall bias of solid performances in the small and mid-cap space this season again continued to favour the higher quality / higher growth businesses, we are seeing renewed interest in some of the more cyclical type companies with lower valuation multiples that are displaying an ability to add earnings growth near term as the underlying economic cycle improves.

Contributed by Ophir Asset Management from the February Letter to Investors

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

9 stocks mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why my mum might help pop the CBA bubble

Elston Asset Management

Equities

Is the end of globalisation the end of global equity investing? The follow up...

Arteqin Capital Limited

Education

Missing the first double on this biotech star

Livewire Markets