Gold – and the Very Large Debt Elephant in the Room

Gavin Wendt

MineLife

It's worth reflecting upon the staggering level of international debt. Financial crises are invariably caused by debt. The Bank of International Settlement (BIS) has recently warned that a new financial crisis is looming. Part of this is simply its job and it's routinely warning against this. But it does have a point.

Claudio Borio, the chief economist of the BIS, is a perennial pessimist, but that's what he's paid for. What he argues is rather simple and elegant. Since the financial crisis, debt/GDP ratio has simply kept rising.

A big part of the reason is the financial crisis itself, which crashed GDP almost everywhere. GDP functions as the denominator in the debt/GDP ratio – and a decline automatically whacks the ratio higher. The BIS argues that the main cause of the rising debt/GDP ratio is interest rates being too low - with an implicit critique of central banks.

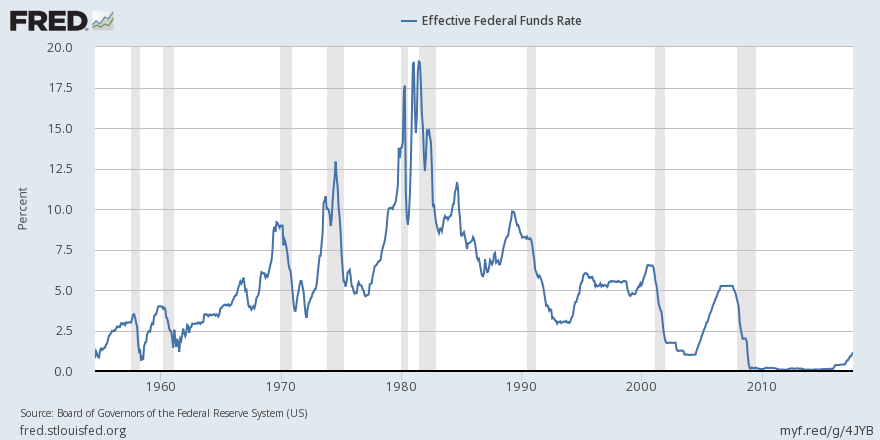

These interest rates are so low because central banks in general and the US Federal Reserve in particular, are steeped in Phillips curve thinking. That is, they take their clues for rising interest rates from the real economy. If unemployment gets too low, this must automatically mean that inflation risks are rising and it's time to start tightening monetary policy. By and large, this is indeed how the Fed operates.

But what if the inflation never really materializes? The BIS argues that technology and globalization are strong deflationary forces, strong enough to tilt central banks into a false lull. The result is that the Fed has kept rates way too low for way too long, which has inflated the debt/GDP ratios.

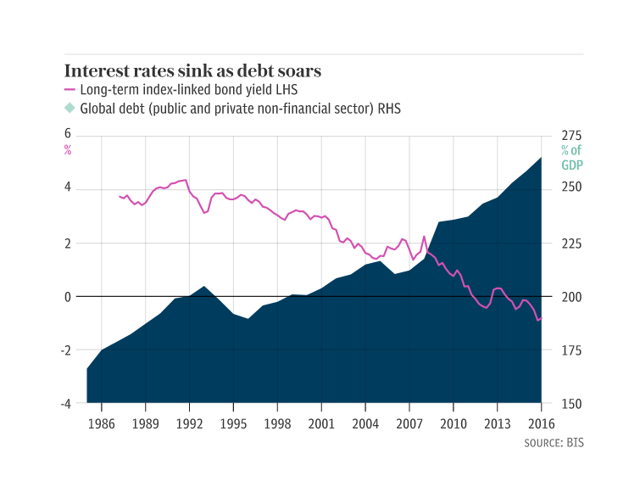

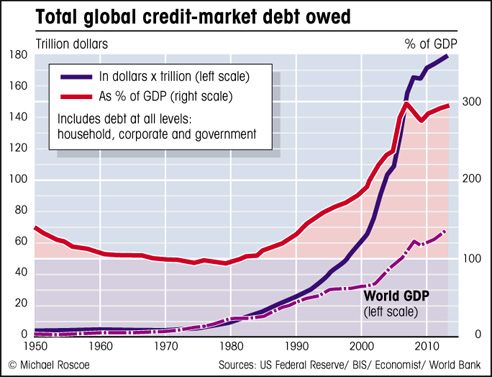

The chart above is a little outdated, given that total global debt now stands at $217 trillion. The fact that it captures the longer term trend however is very important, because it highlights a fundamental problem with the global economy since the 1980's, namely the fact that it takes more and more debt to produce an extra unit of global GDP.

And there is one more piece of information which we need to look at, which explains why the disproportionate accumulation of debt compared with economic growth has not caused a financial catastrophe thus far, but it may yet do so, which is the evolution of interest rates.

As we can see from the two charts, the steady downward path in interest rates starting during the 1980's is basically correlated with the explosion of the gap between global debt and the global economy. Regardless of whether we want to assume that the constant lowering of interest rates happened in response to the explosion in debt in order to help us cope, or whether lower interests caused the explosion in debt, the bottom-line is that the trend which started almost forty years ago has now come to an end.

The world's borrowing capacity will no longer be expanded by significant interest rate declines, because there is nowhere left to go with this trend. The trend did continue for a few years past the point where interest rates flat-lined, because there was still a lot of opportunity to re-finance old debt at the current lower rates. But that trend is also more or less played out at this point in time.

The problem is that unless the debt pile is expanded further, we are unlikely to experience much economic growth in the future. If the debt pile keeps expanding on the other hand, we will soon have an interest payment crisis - given that there is no longer any significant interest rate relief coming as it did in the past four decades. Either way, at some point, something will have to give here.

Which brings us inevitably to gold. The primary cause of the global financial crisis was insolvent banks and massive debt in all segments of society. This has yet to be addressed in any sustainable manner. The financial position of banks and even more so western sovereign nations in many instances is in a far worse state than during 2008, whilst political instability is real and poses risks to markets and risk assets. Investment and savings diversification remains an important consideration.

There is presently a buying opportunity in gold, with various triggers for upside. After trying to convince the markets all was well as it looked to adopt a more hawkish and aggressive economic stance over recent times, the US Federal Reserve has reverted back to its dovish persona. Rate rises are done for 2017, with tepid economic data spooking the Fed – although it won’t admit as much. As readers will know, I’ve had my doubts regarding the reliance of US growth for some time.

Accordingly, I maintain confidence in my base-case gold price target range for the yellow metal during 2017 of between $1200 and $1300/oz, with the potential for further upside.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

5 topics

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets