Has COVID-19 triggered a market ‘melt-up’?

Global stocks have staged a relentless rally in recent months even in the face of arguably the worst economic conditions since the Great Depression. While there are many potential explanations for this apparent disconnect, low global bond yields and a “don’t fight the Fed” mentality seem the strongest factors.

Shake it off – global stocks remain resilient

As seen in the chart below, after a spectacular 34% decline over February and March, the S&P 500 has enjoyed an equally spectacular 44.5% recovery to its recent high on 8 June. As at the time of writing (23 June), the S&P 500 was only 8% below its peak level on 19 February.

Source: TradingView.com

Why has the market rebounded?

Let me suggest a few factors:

- Backwards recession. Unlike previous U.S. recessions, where the economic data gradually gets worse before it bottoms, this recession has maximum weakness front-loaded (due to the lockdowns). The worst economic data was arguably priced during the February/March collapse, meaning markets have been able to focus on the better news flow of ‘flattening the curve’, re-opening hopes and prospects for a vaccine.

- Undeserved recession. Unlike previous recessions, caused by excess debt and/or inflation, the economic weakness is not considered a ‘necessary part of the adjustment’ – rather it is an undeserved consequence of dealing with a medical emergency. Accordingly, there has been less reticence on the part of governments and central banks to provide timely and massive assistance. Compared to the financial crisis, for example, policy has been much more pro-active than reactive.

- Lead sector resilience. The lead sector during the recent bull market, technology, just so happens to be least affected by the lockdowns. This compares starkly with the financial crisis, when the then-dominant financial sector was worst affected.

- Day traders. I’m less convinced of the importance of this factor, though many have noted the strong growth in the number of U.S. retail accounts during the market rebound. With sports gambling sidelined, many unemployed sitting idly at home, the emergence of free and easy-to-use trading platforms, and a rising market after a spectacular collapse, it’s easy to understand why retail participation has increased. While the correlation may be clear, it’s still not obvious which way the causation runs – are day traders causing a rising market or the other way around?

What about valuations?

Of course, a rising market together with falling earnings has meant that price-to-earnings (PE) valuations have increased considerably. As I’ve previously alluded to, the U.S. market risked trading at PE valuations not seen since the late-1990s dotcom bubble if market prices held up while earnings fell.

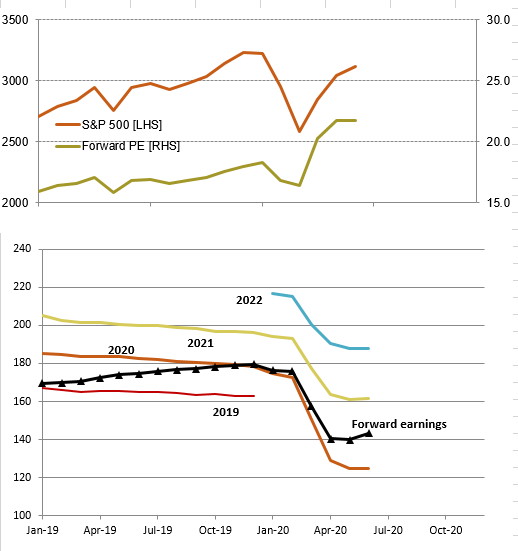

The current situation with respect to the all-important U.S. market is outlined in the chart below. As evident, forward earnings have declined in recent months in line with downgrades to the expected level of market earnings in 2020 and 2021. Along with the rising market, it has meant the market’s price-to-forward earnings ratio has increased to around 22 times earnings, compared with 19 at the market peak in mid-February.

S&P 500: Prices, earnings and valuations

Source: Bloomberg

In recent weeks, however, there’s been some stabilisation in analyst earnings expectations (as surveyed by Bloomberg). Whether this lasts remains to be seen (more downgrades could come during the likely bleak Q2 earnings reporting season and/or if significant new lockdowns are imposed). But as it stands, 2021 earnings are presently expected to rebound by 30%, after a decline of 23% this year, leaving the level of earnings close to that of 2019!

To my mind, this still seems overly optimistic, but if it holds, then at an S&P 500 level of 3,117, the price-to-forward earnings ratio at year-end (since at year-end forward earnings will equal then-expected 2021 earnings) will be 19.3 – which is still well above its long-run average, and close to what it was at the market peak in mid-February.

If earnings expectations don’t decline further, however, forward earnings should continue to gradually rise through 2021, which could help lower PE valuations further – provided this is not offset by continued strong equity price gains.

Do low bond yields justify higher valuations?

Another factor to consider is the still incredibly low level of bond yields, and central bank commitments to keep yields very low for as long as necessary to encourage economic recovery. Indeed, U.S. 10-year government bond yields have dropped from an already very low 1.8% p.a. at the start of the year to only 0.7% p.a. (as at 23 June).

Helping in this regard is the fact that global inflation also remains very low – in a sense, low inflation allows central banks the ability to engage in extreme monetary measures with as yet little apparent cost (at least in terms of their key mandate, consumer price stability!).

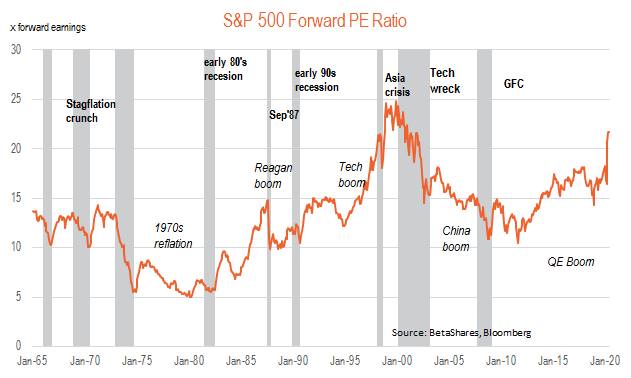

Low bond yields, if sustained, raise questions marks over what the fair-value PE ratio might be going forward. As seen in the chart below, the outright S&P 500 PE ratio is now at its highest level since the dotcom bubble. That suggests caution.

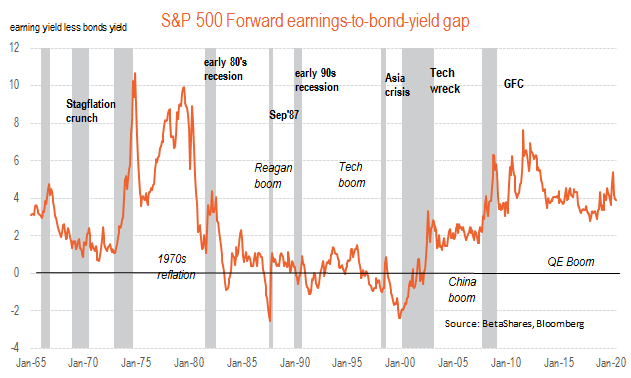

But on the other hand, given the structural decline in interest rates, equity valuations relative to bond yields are not so obviously expensive from a long-run perspective. As seen in the chart below, the forward-earnings yield (inverse of the forward PE ratio) to U.S. 10-year government bond yields is currently around 4% p.a., which is at the lower end of its range of recent years, but only modestly below its post-GFC average of 4.3% p.a. and still well above the 55-year average of around 2.5% p.a.*.

An equity melt-up?

All up, given likely persistent low bond yields, and the market’s apparent comfort with current high equity valuations, investors need to be open to the possibility of a potential equity market re-rating or ‘melt-up’. By way of example, if U.S. 10-year bond yields held for a while at 1% p.a., and the equity-to-bond yield gap returned to its 55-year average of 2.5% p.a., the U.S. S&P 500 could potentially hold a PE valuation of 28!

Indeed, this was a medium-term risk I considered possible prior to the virus crisis, but had thought what now appears a devastating U.S. recession would not see this arise anytime soon. But we need to be open to the possibility that extreme and persistent monetary stimulus (unburdened by the fear of inflation) could have brought forward an impending market re-rating.

Of course, rising equity prices are good news for investors who currently own stocks. But the reality is that high valuations are effectively also lowering longer-run expected equity returns – as adjustment to the fact long-run bond returns have also been lowered.

Never miss an insight

Each week I will publish my latest thoughts on the macro events shaping the ETF landscape. To be the first to read my insights, hit the follow button below.

*Forward earnings estimates prior to the late 1980s are based on estimated trends in reported earnings estimates.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

2 topics

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment