TOL - 16th Dec, 2020

Has there ever been a better time to buy unloved value stocks?

Which of the two Australian stock markets will you be invested in over 2021? The expensive one, trading on record multiples and very high expectations? Or the normally priced one based on low expectations? Returns over 2021 and beyond may be quite different depending on your choice.

The dot.com bubble market from 1998 to early 2000 was famously described as “two-tiered”, but at the end of October 2020 the price difference between popular stocks and unloved stocks was even wider than at the peak of March 2000.

How would you invest if you were given a second chance of allocating to different stocks in March 2000? What if there was an even better relative starting point for unloved value stocks?

In the US we now have a 195-year record of factor returns. Using dividend yield as the valuation factor, work done by a group led by Professor Goetzmann at Yale School of Management, has extended backwards the relative returns of value and growth from 1871 to 1825 on the NYSE. Together with the database of Kenneth French and the work of Cowles (also at Yale), this now gives a 195 year history of relative style returns: 1825 to 2020.

“The further backward you can look, the further forward you are likely to see” – Winston Churchill

While these academic analyses appear to have been done very carefully and thoroughly, the 19th century data should probably be treated with some caution - the three series do not use the same value definitions and it is probably best to focus on volatility/drawdown evidence, rather than cumulative very long-term returns (as any systematic errors will not matter as much over one decade, but they might accumulate over very extended periods).

With these provisos, this history shows that while low P/E and high dividend yield stocks have outperformed their expensively priced peers by more than 3% annually (about 50,000% over the full period), this outperformance has been punctuated by many significant drawdowns against value stocks. Long-short underperformance of at least -30%, for example, has occurred once every 14 years on average, but each of these was first fully reversed and followed by new all-time records for value.

The divergence in prices to Oct 2020 has been the equal greatest in that history (equalling the under-performance of low multiple value stocks to 1904). In Australia, the divergence is the greatest since at least the 1970s and probably since the 1930s.

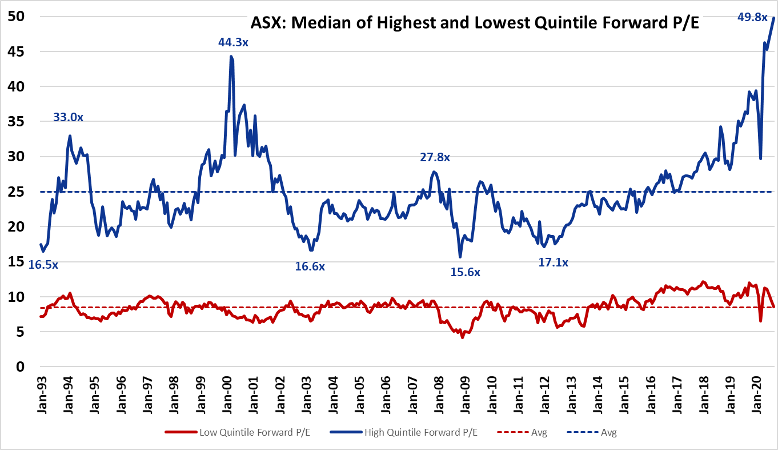

Companies with high cashflows, dividends, net assets and earnings relative to their price have been shunned, while investors have chased popular concept stocks to record multiples across the Australian, global and EM stock markets. In each case the prices of value portfolios have underperformed dramatically despite these value portfolios recording faster earnings growth over the last cycle. This disconnect between relative earnings (value portfolio better than growth) and prices (growth portfolio higher than value) has by mathematical necessity opened a up a wide gap in multiple, as shown in the chart below.

Median forward P/E of highest and lowest quintiles of forward P/E ratios across ASX200. Source: CSFB; Jan 1993 to Sep 2020

Ever-rising multiples – which is just paying more and more for a dollar earnings – is not a sustainable process. The reversal from the October extremes started in November, but it is impossible to forecast the timing of these cycles, of course. If almost 200 years of history are any guide, however, we may expect that:

- the initial reversals of the divergence will be dramatic and volatile, but

- the reversal of the high P/E bubble will take several years to normalise, and

- this cycle will end like all the others since 1825 with value setting new all-time relative records.

History has taught us that markets will repeatedly ignore valuations for extended periods, but that the inexorable laws of valuation gravity always reassert themselves. Assets expensively priced on optimistic scenarios disappoint. In each of those prior episodes, investors had a narrative that purported to explain why it was different this time. Is it this time?

One thing investors can't ignore in 2021

The above wire is part of Livewire's exclusive series titled "The one thing investors can't ignore in 2021." The series will culminate in the release of a dedicated eBook that will be sent to readers on Monday 21 December. You can stay up to date with all of my latest insights by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets Research with Royal & Sun Alliance in Australia, (previously Tyndall Investment Management) and a tutor/lecturer for the School of Mathematics and Statistics at the University of Sydney. Philipp has a BSc (Hons) from The University of Melbourne, a Graduate Diploma in Economics and a PhD from the University of Sydney. Philipp specializes in interest rate sensitive companies and is fluent in German.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

1 topic

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets...

Expertise

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets...

Expertise

Comments

Comments

Sign In or Join Free to comment