How to use the VIX to protect your portfolio

Scott Shuttleworth

Vega Capital

Today I wanted to provide some depth on how we use VIX products to manage risk in The Vega Fund portfolio. As far as we know, we’re the first fund in Australia to hedge in this particular fashion and hence some clarity is warranted. It’s not the only tool in our risk management toolkit, but we do use it on a daily basis.

What is the VIX?

The VIX is an index which attempts to measure the market's expectation of annualised volatility over the next 30 days. Simply put, if the VIX is at 10 then the market as a whole is anticipating annualised volatility of 10 per cent.

The VIX is typically negatively correlated to stock market movements, for example, as stocks fall the VIX will usually rise and vice versa. Because of this, it can be a useful tool for hedging.

How do we trade it?

We can’t own the VIX directly but you can enter derivatives on it – for example, VIX futures or options. There are also some indices linked to the VIX however we don’t use those at The Vega Fund. Credit Suisse’s ending of trading in the VelocityShares Daily Inverse VIX Short-Term Exchange-Traded Note shows why we don’t engage in these products.

There are no direct/spot VIX products largely because there are no other investors there to take the other side of a long spot VIX trade (since it’s almost a guaranteed winner). For example, say the VIX is at 10, it’s almost guaranteed that at some point the VIX will be higher than 10 and hence the long holder will realise a profit for no risk. Hence most of the time there is a cost to entering into any derivative contracts on the VIX.

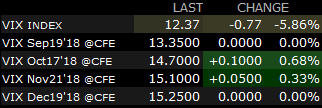

One of the ways to go long or short the VIX is to enter into a futures contract. If long, this usually comes with a cost. For example, say the VIX index was at 10, I would generally expect the next month’s VIX future contract to be at say 11.5. This means that you’re effectively paying an additional say 1.5 to be exposed to the index (in dollar terms, $1,500 per contract). We can see that in the below spread of options (albeit, the here VIX/Sep 19'18 Future is 0.98 or $980).

Future month’s being at higher prices to current months is the normal state of VIX markets and is referred to as contango. It can invert (which generally occurs after a market correction, a state known as backwardation) but this is quite uncommon.

You could also short the VIX and earn that 1.5 spread but noting that if the market has a blip and the VIX goes to 30, you might be exposed to a lot of downside per contract.

Margin capital is also required for each contract. Current rates are circa $8,800 in margin per contract (this can vary from broker to broker) and can increase or decrease over time.

We can also enter into call or put options on the VIX. Keep in mind that these are usually very expensive.

Trading strategies

Obviously if an investor has a view that future volatility will increase, the VIX can be a good way to profit from this view (but remember to take implied costs into account as noted above).

At The Vega Fund, we generally use the VIX futures for hedging purposes (i.e. we have a portfolio which is long the market and exposed to large increases in volatility). So by going long VIX products which are negatively correlated we can offset this risk to a more manageable level.

But we also generate returns from the VIX by buying more if it as it falls (i.e. buying more protection when the market becomes relaxed) and selling off our VIX positions as it rises (i.e. selling our protection when the market becomes fearful). Simply put, as contrarians, we’re buying VIX low and selling it high.

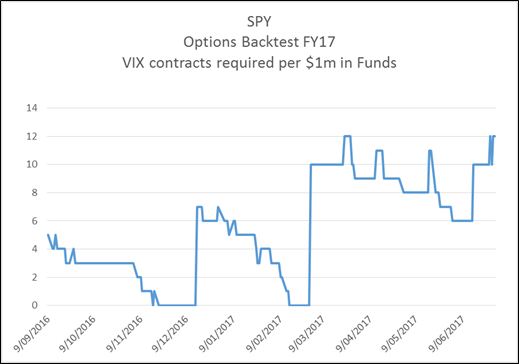

We determine the number of VIX future contracts we need via a dynamic formula which is updated daily. It’s a little beyond the scope of this blog but generally speaking, we end up holding between 6-12 VIX long futures contracts for every $US1m in funds under management. After a 10-30% correction or if our strategy is trading lightly, this might reduce down to between 1-5. This strategy has proven effective in dealing with most market hiccups in backtests (including August of 2011).

The below table shows the number of VIX future contracts held in the portfolio for every $US1m in funds under management during a FY17 backtest trading options on the SPY so you can see what this looks like.

Don’t forget trading costs

Generally speaking, the more you trade the less you’ll make in the markets since commissions eat up returns. Even trading costs of 0.1% per month can add up to 1.2% over the year (high fee hedge funds charge 2% for an entire year’s worth of portfolio management…is trading worth 60% of that?). Hence when employing our dynamic hedging algorithm, we take care not to let it adjust too frequently.

Summing it up

Due to its negatively correlated returns, the VIX can be a particularly useful product in which to protect a portfolio from downside risk.

It’s important to understand its characteristics so as to manage its implicit and direct costs but there are few products which capture risk as well as the VIX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

11 topics

Scott Shuttleworth

Founder and Portfolio Manager

Vega Capital

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

Expertise

Scott Shuttleworth

Founder and Portfolio Manager

Vega Capital

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management