How will COVID change the world?

The COVID-19 pandemic and associated shutdowns of economic activity are an enormous negative growth shock that is causing unprecedentedly deep recessions almost everywhere. But the contraction phase of the crisis has also been comparatively short-lived, and our forecasts incorporate a recovery from H2 2020 as shutdowns are slowly lifted. Nevertheless, the long-term consequences of the crisis will be profound, including a permanent loss of output, labour market scarring, lower equilibrium real interest rates, and an altered balance between monetary and fiscal policy. The inflation implications are less clear as near-term disinflationary impacts could give way to either much lower or much higher inflation depending on how policymakers react.

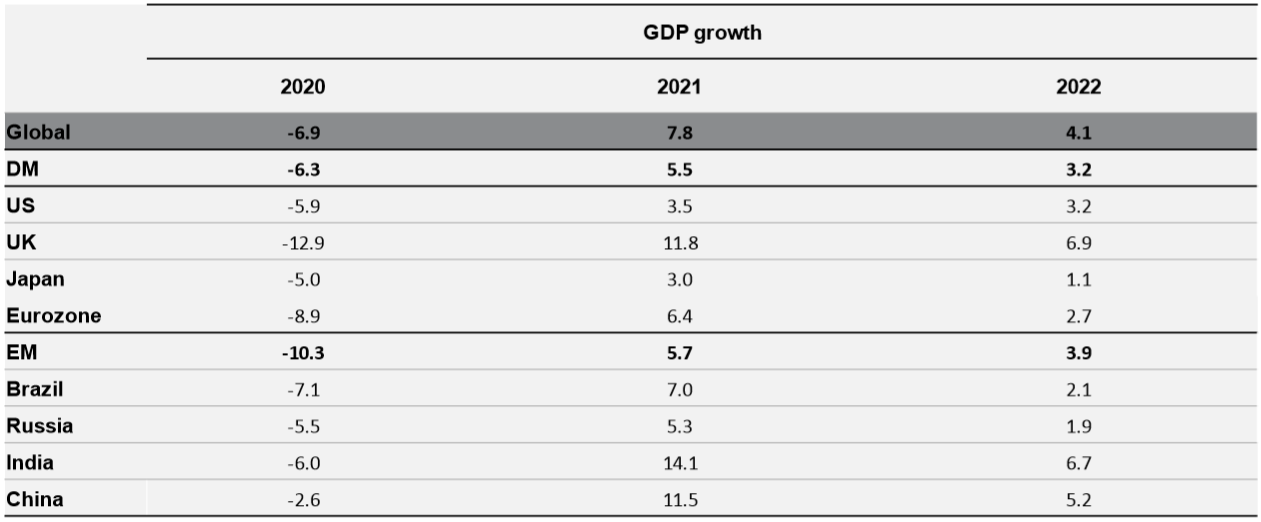

Global forecast summary

Source: Aberdeen Standard Investments (July 2020)

With Q1 GDP data now available for most economies, it looks like the global economy contracted close to 5%. But the full force of lockdowns, at least outside China, wasn’t felt until late in the quarter and at the start of Q2. Hence the second quarter could be perhaps twice as bad again. Recent PMIs and a sharp labour market deterioration imply deep contractions almost everywhere. All told, we forecast a peak-to-trough hit to global GDP of about 13%, and a year-average contraction of 7.4% in 2020. This is much worse than the 2008-09 Global Financial Crisis (GFC), and comparable the Great Depression.

However, with new infections bending lower in many economies, attention is turning to the exit strategy and the nature of the recovery. The lifting of lockdowns has proceeded quicker than we initially expected, prompting upward revisions to our forecasts. We incorporate a recovery in Chinse GDP from Q2, and recoveries in GDP elsewhere from Q3 – although the absolute trough in activity in many economies was April or May. At a global level, this means GDP growth of 7.8% in 2021.

Nevertheless, the cyclical rebound is set to be partial. We expect permanent output loss relative to the pre-crisis trend, as behavioural changes and labour market scarring mean some activity is never recovered.

Moreover, uncertainties about the forces buffeting the global economy remain high, and our baseline forecast is only one of several plausible scenarios. A longer-lived shock, or a ragged “W” shape to the recovery as lockdowns are re-imposed, is a greater risk to our baseline than a “V” shaped recovery.

Fiscal policy has taken the lead responding to the coronavirus shock. The appropriate policy response is to increase healthcare funding, help households and firms bridge the cash flow shock from the sudden stop in activity, and limit the breaking of labour market matches. Admittedly, the Chinese policy impulse is weaker relative to the GFC. But the global fiscal policy response totals 3% of GDP of structural loosening, twice as large as last time around, with more coming.

While it is true that monetary policy cannot offset the huge economic disruption from lockdowns, central banks have shown once again that they are not “out of ammunition”. Monetary easing has helped smooth the financing of the huge fiscal measures while also providing independent support to the economy by providing bridging finance to prevent a liquidity shock becoming a solvency crisis. However, even more powerful policies are available: helicopter money is an appropriate and effective tool that central banks could deploy.

On a country and regional basis, the hit to activity and subsequent rebound will depend on incidence of the virus, success in lifting lockdowns, and the size of policy responses. China was “first in” to the crisis but also first out. Official data suggesting the industrial sector rebounded strongly in March and April offer a glimmer of hope for other economies, but re-occurrence of the virus in certain provinces, and the slower recovery of services, have less encouraging read across.

Elsewhere in the EM complex, some important countries have been slow to respond to the danger (Mexico and Brazil); have under-resourced health systems (India and Indonesia); or are vulnerable to balance of payments crises (Columbia, Egypt, South Africa and Turkey). Capital controls are likely to ratchet up, especially if the IMF ends up overwhelmed by requests for assistance to manage external funding pressures.

The US public health response has been haphazard, while testing and contact tracing has not expanded to make exit plans work effectively. Meanwhile, the failure of Congress to adequately subsidise firms to keep employees on payrolls means a catastrophic increase in unemployment is underway.

Across the largest economies in Europe, the German health response has been more effective than that of France, Italy and Spain. Similar divergences are playing out in fiscal responses, amplified by the weakness of coordination efforts and failure to mutualise risk. Both will condition the timing and success of exit strategies, though the European economy is so heavily integrated that all will suffer amidst the fragmentation.

Finally, our attention is turning to how the world will change in the longer term as a result of the pandemic. More activist fiscal policy, funded in times of crisis by monetary policy; deeper cleavages in the Sino-US relationship; a bigger, more intrusive state, especially when it comes to surveillance; further moves towards deglobalisation; more economic activity taking place online; and a shift in the politics around climate change, are all potential long-term outcomes of this crisis.

The above wire is an extract from our recent Global Economic Outlook, The Great Shutdown, which you can see in full here

Access original research from around the world

I lead a global team of economists and researchers providing projections and scenario analysis for the global economy, while also undertaking fundamental empirical research on topics at the intersection of economics, politics, policy and markets. Stay up date with all my latest insights by clicking the follow button below..

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jeremy Lawson is Head of the Research Institute at abrdn. He joined Standard Life in 2013 from BNP Paribas in New York where he was a Senior US economist. Previously, he has worked the OECD and the Reserve Bank of Australia.

Featuring

Jeremy Lawson,

abrdn

Jeremy Lawson is Head of the Research Institute at abrdn. He joined Standard Life in 2013 from BNP Paribas in New York where he was a Senior US economist. Previously, he has worked the OECD and the Reserve Bank of Australia.

........

Issued by Aberdeen Standard Investments Australia Limited ABN 59 002 123 364 AFSL No. 240263. This document has been prepared with care, is based on sources believed to be reliable and opinions expressed are honestly held as at the applicable date. However it is of a general nature only and we accept no liability for any Standard Investments Client Services on 1800 636 888, at or from your financial adviser. This document has been prepared without taking into account the particular objectives, financial situation or needs of any investor. Investments are subject to investment risk, including possible delays in payment and loss of income and principal invested. It is important that before deciding whether to acquire, hold or redeem an investment in a Fund that investors consider the Fund’s PDS, the Fund’s appropriateness to their own circumstances, objectives and financial situation and consult financial and tax advisers. You must not copy, modify, sell, distribute, adapt, publish, frame, reproduce or otherwise use any of this material without our prior written consent. Past performance is not a reliable indicator of future results. All dollars are Australian dollars unless otherwise specified. Indices are copyrighted by and proprietary to the issuer.

4 topics

Jeremy Lawson is Head of the Research Institute at abrdn. He joined Standard Life in 2013 from BNP Paribas in New York where he was a Senior US economist. Previously, he has worked the OECD and the Reserve Bank of Australia.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets