5 reasons hybrids deserve a spot in your portfolio

Australian income investors used to be lucky. From 1980 to the middle of the last decade, they could achieve returns of more than 3% above the rate of inflation simply by investing in totally safe cash term deposits (this was around 1.5% higher than anywhere else in the world). They didn’t need to take investment risk for income

Those days are gone. Term Deposit (TD) rates are now less than the rate of inflation, and income investors are grappling with this new world of having to find income but having to take more risk to get that income. And with the RBA signalling that cash rates will stay low for at least the next 3 years, that problem is not going to go away.

We think the way forward is to find a combination of high income, but higher risk investments, that display uncorrelated return outcomes and have different factors driving those return outcomes. Over a cycle, something will undoubtedly go wrong, but if there is sufficient diversification, the portfolio should still generate returns outcomes well above cash and Term Deposit rates.

How do hybrids fit into a portfolio of income assets?

Hybrids form a very important part of any income portfolio for a number of reasons;

- The credit quality of the issuers, which are mainly banks and other financial institutions, is very high - much higher than a lot of the loan fund alternatives. More importantly, bank income is more diverse than a portfolio of corporate loans, which are entirely reliant on a relatively small number of corporate borrowers paying interest and principal. It will take a very severe recession before the credit quality of the banks becomes concerning.

- Historical returns (and probably prospective returns) of hybrids have not been much lower than equities (refer chart below).

- Return volatility is much lower than equities.

- Unlike many of the loan and bond funds that have been issued on the ASX since 2018, there is an important ‘mark to market’ mechanism. We are now at the beginning of a recession where it is inevitable that some corporate loans will default (to date however, we’re not aware of any write downs in the loan funds). At the same time, there is no market in the underlying loans, very little visibility as to who the loans are made too and an illiquid market in the actual loan vehicle. So, no one has any idea what the “real” NAV should be, let alone whether the loan funds should be trading at a discount or premium to the published NAV. This is not a trivial matter. During the GFC period, the cumulative default rate of “B” rated bonds was over 17%.

- Liquidity of ASX listed hybrids is satisfactory for all small investors.

Why do hybrids work?

The charts below show the risk and return outcomes of ASX listed hybrid market using proprietary data of 20 years from the Elstree hybrid Index and the All Ordinaries Accumulation Index; The way to read the chart is the vertical axis shows the investment needed at any one point to have an amount of $1,000 at 30/6/20. Clearly, lower is better, but as the chart shows you have to go back to 2003 before equities (blue line) materially outperformed hybrids (green line), and clearly hybrids are much less volatile than equities. This is because the hybrid return of cash +3% is roughly equivalent to what the broader equity market has returned on an annual basis over the past 50 years.

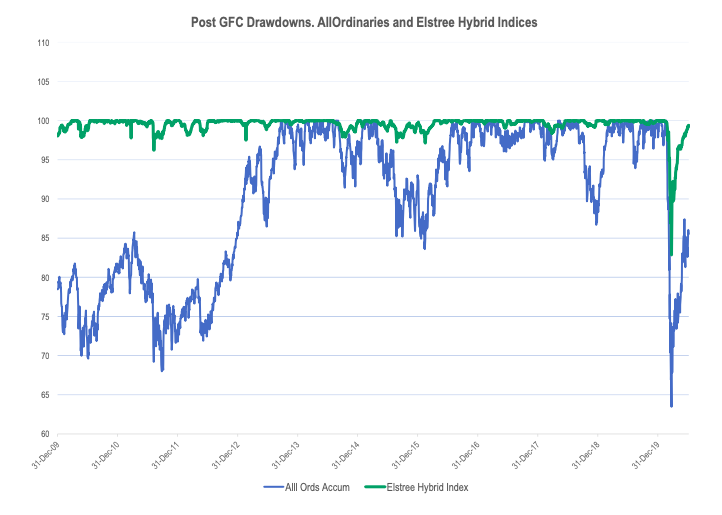

The drawdown chart below shows the differences in volatility more clearly. When the vertical axis is at 100, it indicates that the index is at an all time high. Since the GFC, equities (blue line) have had a number of 10% + drawdowns, each of which took a long time to recover, while the maximum drawdown in the hybrid market (green line) was c2% and it was not long in duration. Even the Covid 19 crisis was reasonable for hybrids despite the greater stresses presenting in the system. Hybrids fell by far less than equities and are now back to February 2020 index levels while equities are still c15% off their highs.

Risks

As we mentioned above, there is no return without risk. We see 2 main risks in the hybrid market. The risks are;

- The conversion/non viability issue . We’re much more sanguine about the conversion/non viability issue than many commentators. While it will become relevant at some point we don’t think it manifests in hybrid security prices until banks become closer to non-viability. We’ve haven’t seen a non-viable Australian bank, but offshore experience tells us that non viability presents when bank ratings approach the “BBB” level (a long way from where Australian banks are now) and share prices fall to a fraction of book value (ie CBA share price falling another 80%).

- However, weak equity markets will affect hybrid prices in the short and medium term along with occasional concerns surrounding the continuation of bank dividend payments and hybrid distribution payments.

Outlook

Historically, when spread margins are 4% or more than 4% over cash, there has not been a subsequent 12 month return outcome of less than 4.5% (with the average return in the high single figures). Spread margins over cash are now a little less than 4%, so the prospect of high single digit returns is a little lower. However, we think that spread margins are going to continue to narrow to less than 3% which will, everything being equal, produce near term capital gains (spread margins move in the opposite direction to price). We think, retail investors, who are over exposed to low yielding Term Deposits, faced with an array of uncertain investments including declining dividend yields, problematic loan funds will continue to seek out hybrid securities.

A security example: PERLSVII (ASX:CBAPD)

A typical security is the Commonwealth Bank’s PERLS VII issue (ASX coded “CBAPD”). The security has a notional ‘maturity date’, known as the ‘first call date’ of 15 December 2022 (it has a compulsory ‘exchange date’ 2 years later of 15 December 2024). The security pays a quarterly coupon rate of bbsw plus 2.80%. The coupon rate of bbsw plus 2.80% represents the gross coupon which means it is inclusive of franking credits. The current price of c$99 results in the security generating a yield of around 3.5% which is made up of; BBSW of 0.25% + spread margin of 2.8% and capital appreciation of around 0.5% p.a). This compares with a major bank 2 year Term Deposit rate of around 1%.

So given you are receiving a materially higher rate of return than a Term Deposit, what are you getting paid for and what can go wrong?

- You can’t sell it - Not an issue. The security turns over more than $50m per month.

- Its price is volatile - Sometimes. The usual monthly price movement is around $1. During Covid 19 however, the price fell from $100 to under $90 where it stayed for approximately 10 days – it was still under $96 through until the end of April. It is now $99.

- You don’t receive coupon payments - Possible. Hybrids provide a safety net for banks to protect depositors. If conditions are sufficiently dire, APRA may force the banks to not pay distributions on hybrids. However, if a bank pays a dividend or its’ ordinary equity, it has to pay a hybrid distribution and even in these days of bank dividend reticence, there has not yet been a case globally where a major bank has not paid a hybrid dividend (even when the parent bank is prohibited from paying dividends).

- You don’t get your capital back on time: Possible. As part of the bank safety net, PDS’ are full of technical clauses about “calls” and “compulsory exchanges”, which translated simply means the banks aren’t required to pay the hybrid back if conditions are dislocated or sufficiently dire. However, when conditions normalise, banks are heavily incentivised to pay the hybrid back on or before its due date.

Whether the additional return justifies the risk

is a question for individual investors and of course, the risk is inversely

related to the health of the Australian banking system. However, if an investor

can find investments that are less dependent and less correlated to Australian

banking risk, the risks highlighted above, become less of an issue and hybrids

“work”

by providing higher return outcomes.

Specialists in producing capital stable franked income returns

Capital stable, franked income returns are the investment mantra of self-managed superannuation retirees. At Elstree Investment Management Limited we cater for this mantra.

Our Funds, which invest in a diverse range of floating rate credit securities called hybrids, are designed to deliver capital stable franked income returns on a consistent basis.

Visit our website for more information or send us a message via the 'contact' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Campbell Dawson co-founded Elstree Investment Management Ltd, who are a specialist hybrid manager. In March 2021, Elstree launched the Elstree Hybrid Fund (EHF1), an Exchange Traded Product quoted on Chi X. Prior to co-founding Elstree in 2003, he had 19 years experience in Funds Management and Corporate Treasury

3 topics

Campbell Dawson co-founded Elstree Investment Management Ltd, who are a specialist hybrid manager. In March 2021, Elstree launched the Elstree Hybrid Fund (EHF1), an Exchange Traded Product quoted on Chi X. Prior to co-founding Elstree in 2003,...

Expertise

Campbell Dawson co-founded Elstree Investment Management Ltd, who are a specialist hybrid manager. In March 2021, Elstree launched the Elstree Hybrid Fund (EHF1), an Exchange Traded Product quoted on Chi X. Prior to co-founding Elstree in 2003,...

Expertise

Comments

Comments

Sign In or Join Free to comment