Income investing when yields collapse

Alex Cowie

Falling yields were already one of the biggest challenges facing retirees seeking investment income, but the dramatic impacts of COVID-19, which have seen bond yields collapse have made this issue more pressing than ever.

We reached out to four experts in the area of retirement income to ask some of the ways retirees can mitigate this issue, and whether selling down the portfolio to raise cash is even part of the solution, as some have suggested.

Read on for responses from Simon Doyle at Schroders; Charlie Jamieson from Jamieson Coote Bonds; Richard Dinham at Fidelity International; and Raf Choudhury of State Street Global Advisors.

Some drawdown of capital may be part of the solution

Simon Doyle, Schroders

Since the Asian crisis in the late 1990s, central banks have failed to allow imbalances to properly correct, bailing out markets and investors and fuelling strong credit growth and boosting asset prices in the process.

This strategy successfully averted major economic catastrophe in the aftermath of the “tech bubble”, September 11 and the GFC, but the consequence has been rising debt and rising asset prices across the risk curve. It has also manifested now in very low to negative real and nominal interest rates as policymakers struggle with the debt burden created.

This has meant that borrowers have been bailed out and asset owners have been big beneficiaries of rising asset prices and rising wealth.

This is important in the context of the current challenge of finding high quality, low risk income. While policymakers argue that lowering official rates (especially mortgage rates) is stimulatory for the economy overall given the higher propensity for borrowers to consume, the flip side is the significant reduction in income for depositors and savers more generally. As rates fall, the reduction in cash flow becomes proportionally greater.

Whether this seems fair will depend on which side you sit. From a bigger picture perspective, it is generally the “savers” or the asset owners that have benefitted most from the decline in interest rates to current levels and the asset price appreciation (property, infrastructure, equities, bonds) that has resulted from a revaluation to a low interest rate environment.

In other words, the income being generated from their investments in percentage terms (especially cash) may have declined but the value of the underlying asset base for many will likely have increased, in many cases significantly over this period.

All that said, the practical challenge for all of us, is “what do we do now” for income? I think there are several broad choices:

- We could take more risk: With dividend yields on equities still relatively high especially in Australia, dividend income looks attractive, but it will come with more capital volatility and if your timing’s wrong, significant downside risk. Normal equity market volatility is around 12-14% pa and in bear markets, prices can fall sharply, so attaining higher income from dividends does place more capital at risk. Timing will matter.

- We could restructure our portfolios: Here I’d suggest a “flatter”, well-diversified portfolio which makes broader use of the capital structure – perhaps switching some cash into high quality, but slightly higher-risk investments (like investment-grade credit, and residential mortgages) and switch some equity into higher-yielding debt investments like higher-yielding corporate bonds, commercial mortgages or Asian and emerging markets bonds.

- Finally, we could incorporate some drawdown of capital to improve the consistency and predictability of cash flows to the investor (as opposed to just utilising the actual income generated from the investment).

This last idea is most consistent with the arguments outlined above with respect to the accrued asset price appreciation on the back of the structural decline in rates. Another way to think about this is that in a world with higher interest rates, the rate of income would likely have been higher but on a much lower capital base. In a low interest rate world, the rate of income is lower but the capital base on which it accrues will be, in many cases, significantly higher.

This too may not be a popular suggestion given the strong preference investors have to leave their capital base untouched. But for those who have been beneficiaries of the last 2 decades of every rate decline and rising asset prices, it may well be a less risky path to generating appropriate and predictable outcomes than other options.

Falling yields can potentially dampen income that retirees receive from their investments, which can have an impact on living standards. Given the current low yield environment, retirees may be looking to increase their risk exposures in order to receive a higher yield as well as reduce their own discretionary expenditures.

Retirees should be mindful that they may put their capital at risk by overloading on what they perceive to be ‘defensive’ or ‘high income-producing’ assets that, during times of stress, can quickly lose these defensive characteristics.

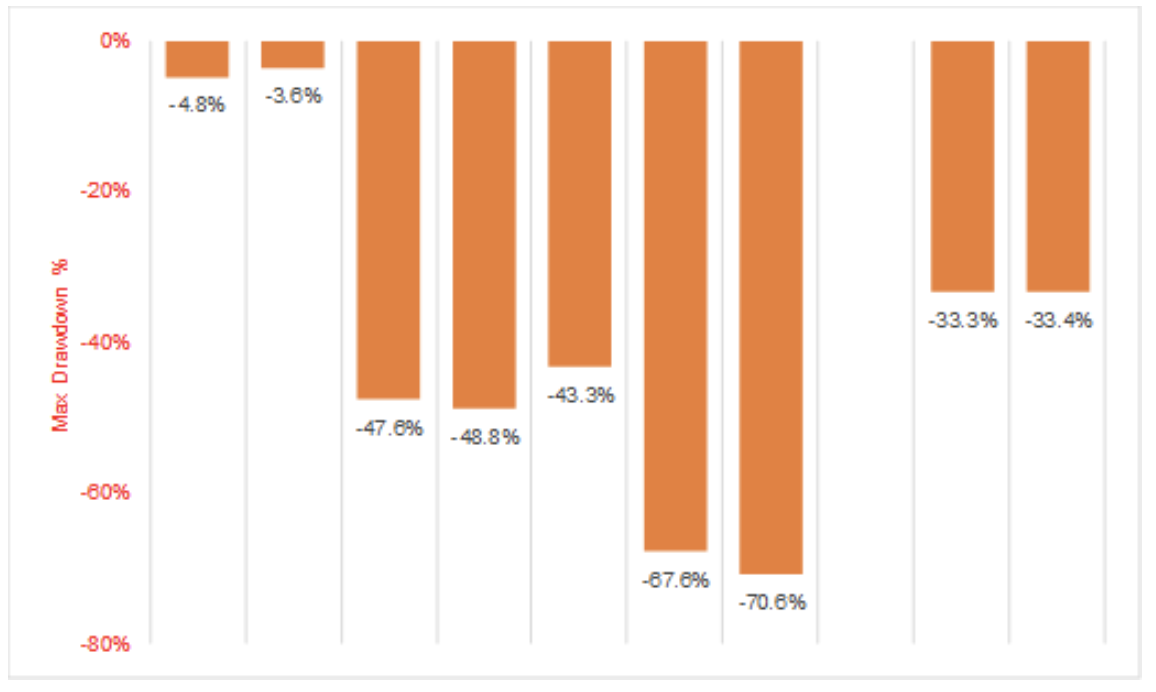

Figure 1 shows that during heightened market turbulence from the global financial crisis (2007-09), European region concerns (2011), and Chinese weakness (2015), higher-yielding instruments such as hybrids, speculative property offerings, and subordinated debt suffered in value and provided little to no liquidity.

Investors need to consider the risks carefully, as well as potential returns, before investing in high yielding products that they may not truly understand.

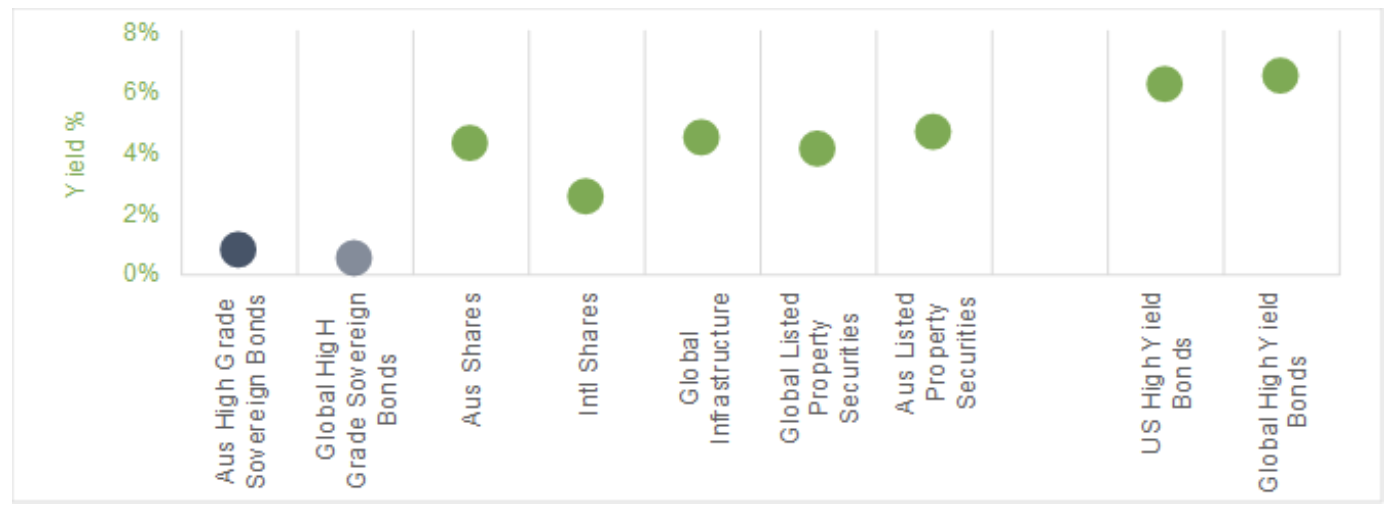

Figure 1: Reaching for yield can expose your portfolios to significant risk

The current yield of common asset classes:

Source: JCB team analysis

The worst drawdowns of these same asset classes, since Jan 2002

Source: JCB team analysis based on data from Bloomberg, to 29 Feb 2020.

What we see over time is that many retirees take on too much risk by investing in exposures that freeze in times of market stress.

Given retirees’ real susceptibility is to sequencing risk (how the order of returns can permanently affect a client’s retirement income), key strategies to reduce the impact of sequencing risk may include a reduction in the growth component of an investor’s risk profile as retirement approaches, as well as ensuring the appropriate level of defensiveness and diversification exists within their portfolio.

Asset allocation is key and investors need to carefully think through what is behind their portfolio during testing times.

A cashflow strategy could include re-weighting assets so that there is a short-term allocation to cash to cover expenses, fixed income to cover medium-term income and growth assets for longer-term income.

With an ageing demographic commonplace across the developed world, and yields likely to be low for the foreseeable future, these issues are likely to remain highly relevant.

Total returns are what matter most

Richard Dinham, Head of Client Solutions and Retirement, Fidelity International

Falling yields across the globe in virtually all asset classes has led to increasing difficulty for retiree investors in finding suitable and sustainable sources of income.

Of course, one of the benefits of falling yields has been the continued strong performance of many asset classes, in particular, risk assets such as equities (although recent market concerns from COVID-19 has caused a pull-back).

But for retirees, we should keep in mind that, at the point of retirement and beyond, the financial objectives of investors usually change. This change can be summarised as a switch from a growth-seeking mindset to more of a capital preservation and income mindset (although we should always caveat that not all investors’ objectives and needs are the same).

So, yes, retirees certainly do need income. But I would make one important observation here - investors need to be careful in pursuing income without first considering the impact of an investment on their overall total return.

Total returns are actually what matter most to the investor. The yield on an investment may be attractive, but if the total return is poor, or even negative, then that will not a good investment outcome for the investor - their savings will become depleted.

Ways to mitigate the challenges of finding sustainable income in retirement are many and varied, but I would recommend the following principles are followed:

Seek income from diverse sources - diversification is your friend here, although using too many sources of income will add to complexity. For example, income on Aussie shares has been popular in the past but we know from experience of high yielding Aussie shares in 2018/19 that total returns can sometimes be very poor. So, look at finding income from all sorts of other places such as bonds, term deposits, diversified higher-yielding credit bonds, property (listed and unlisted), and spread the allocations sensibly across these multiple areas.

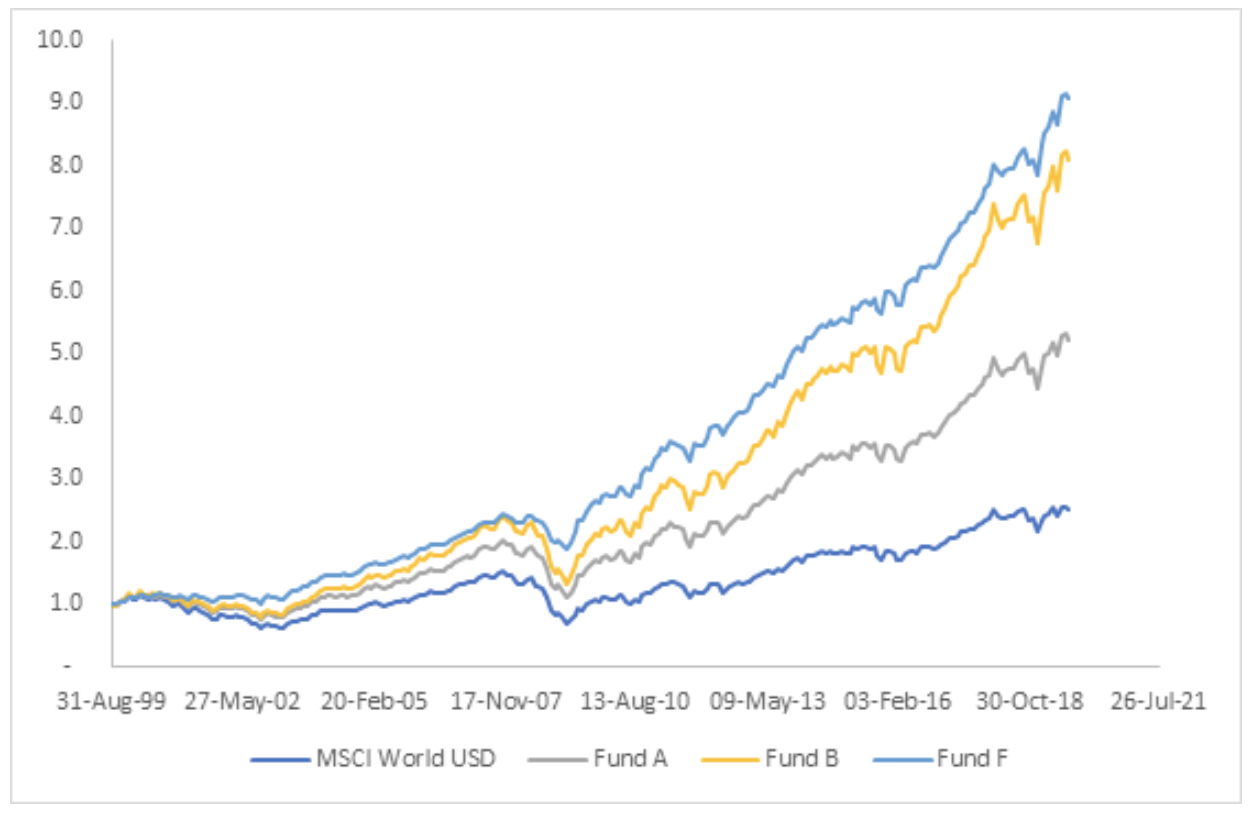

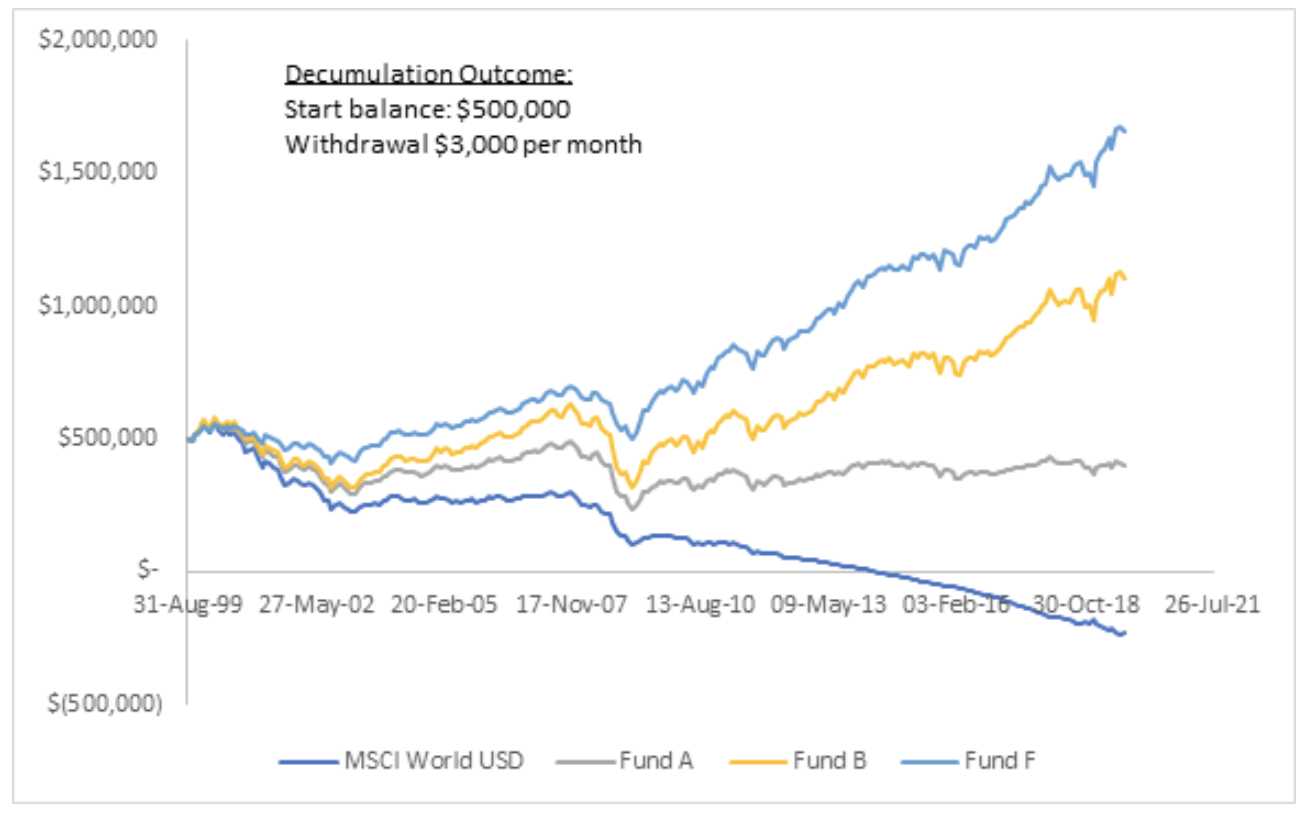

Look for investments that give exposure to a risk premium (e.g. equity, credit) but which also have an eye on capital preservation. If you can mitigate the effects of market volatility on the value of your capital whilst maintaining exposure to the risk premia, then that makes a massive difference to compounded outcomes over time, most especially for those investors who are in retirement and drawing an income. See Charts 1 & 2 below for an example of this - investments with a good ‘downside capture’ that fall less than the market during periods of volatility will perform the best for investors who are in decumulation.

The suggestion of drawing down on capital for retirement income I believe should form at least part of the approach for many retirees.

It is inevitable that this will need to be done as yields on most investments are simply not enough to sustain the necessary income in retirement. And if the investment is within Super, the minimum drawdown limits (4% from age 60, 5% from age 65, etc) will often mean that natural income in the portfolio will be insufficient to meet these compulsory limits.

Don't overlook Floating Rate Notes as an option

Raf Choudhury, State Street Global Advisors

In the current environment of low rates and increasing volatility across markets and asset classes, selling down a portfolio to generate cash is an option to manage investors' risk. It may though offer little in terms of income and yield, especially true in today’s current lower rate environment.

For investors who may need to draw down income and need to look beyond traditional “income” assets for yield, having a pool of deposits or a portion of a portfolio in fully liquid assets may be a good solution.

Term deposits tie up investors' capital for a certain length of time depending on the maturity selected, and with current rates as low as they are, investors may question if they are sufficiently rewarded for this illiquidity.

Traditionally bonds were another option for income investors but the yields across Australian and international government bonds have fallen to record lows.

Investors should also consider that with yields at current levels, any re-pricing could see a significant loss of capital.

One area investors could consider holding is floating rate notes (FRN). FRN style funds could be advantageous as these notes reset and pay coupons, and generally offer a spread above cash rates.

In summary

To wrap it up, here are some of the key points from Simon, Charlie, Richard and Raf.

Simon Doyle from Schroders suggested retirees could take more risk, or run well-diversified portfolio which makes broader use of the capital structure, or incorporate some drawdown of capital to improve the consistency and predictability of cash flows

Charlie Jamieson at JCB emphasises the importance of understanding the risks of high yielding asset classes with many having seen falls of 40-70% at various points in the last 18 years, compared to just 3-4% for bonds. He also suggested a cashflow strategy that could include re-weighting assets so that there is a short-term allocation to cash to cover expenses, fixed income to cover medium-term income and growth assets for longer-term income.

Richard Dinham at Fidelity discussed a) diversification of income sources including bonds, term deposits, diversified higher-yielding credit bonds, property (listed and unlisted); b) investments that give exposure to a risk premium. Richard also wrote that drawing down on capital is inevitable as yields on most investments are simply not enough to sustain the necessary income in retirement.

Raf Choudhury from State Street focused on floating rate note style funds which he believes could be advantageous as the notes reset and pay coupons, and generally offer a spread above cash rates.

Overlooked sources of reliable retirement income

If you found that useful, watch out for the next few parts, in which Simon, Charlie, Richard and Raf first all nominate the most overlooked sources of reliable retirement income.

We also then ask them how investors can still get a solid yield without the higher risk profile - and how they are doing this themselves.

If you want to be sure not to miss these next wires, please hit FOLLOW to get them emailed directly to you soon after they go live.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Alex Cowie,

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Featuring

2 topics

3 contributors mentioned

Alex Cowie

Content Director

Alex happily served as Livewire's Content Director for the last four years, using a decade of industry experience to deliver the most valuable, and readable, market insights to all Australian investors.

Expertise

Comments

Comments

Sign In or Join Free to comment