Is Berkshire Hathaway a victim of its own success?

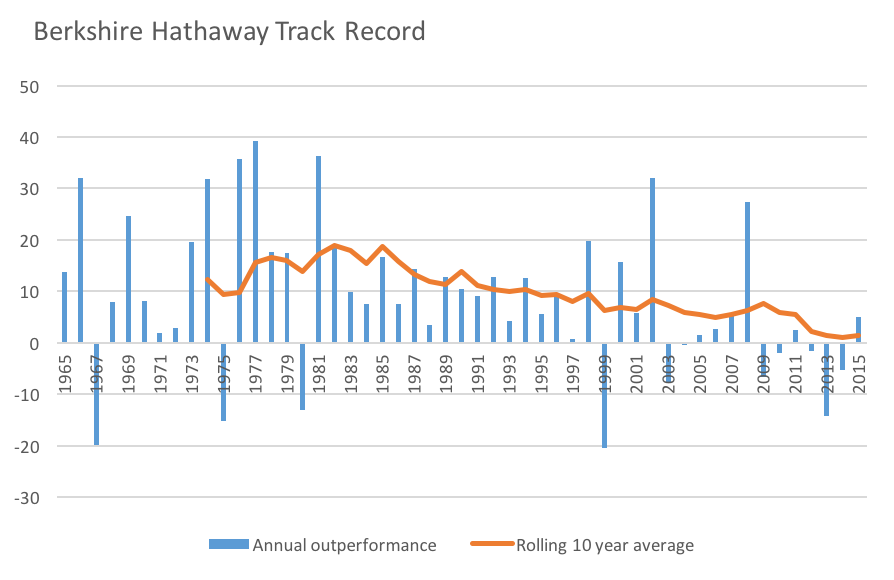

There is no debate about the long-term investment success delivered by Berkshire Hathaway. Since 1965, compound growth in per-share book value of Berkshire has far outstripped growth delivered by an investment in the S&P500 Index, resulting in an exceptional long term investment experience for Berkshire’s owners. However, while the long-term results are exceptional, the more recent results have been less so. The chart below shows the annual gap between growth in per-share book value and the return received on an investment in the S&P500 Index (in blue), and the rolling ten-year average gap (in orange). What the chart shows is that for recent ten year periods, the gap has been running at ever declining levels (albeit still in positive territory).

For anyone who subscribes to the Buffet philosophy – and that’s no small number of people – the question arises as to why this should be the case, and what it means for the ongoing success of this style of investing. It is possible that Berkshire has experienced a difficult period in recent times, but the long time frames and apparent consistency of the decline point to lasting change, rather than something temporary.

Unfortunately, it is not easy to determine what factors might be contributing to such a change, and to what extent. However, we can begin with a list of some of the more likely contributors, which would include the following:

- Sheer size – it has become difficult for Berkshire to find investments that “move the needle”;

- Markets have become more efficient over time, and therefore harder to beat; and

- Berkshire’s investment style has become so widely adopted that it is now a “crowded” space.

There are no doubt other factors that could be proposed, but I suspect the above factors all make a meaningful contribution to the apparent decline. We offer the following observations:

- Size is undoubtedly part of the issue. As an investor grows in scale, the universe of meaningful investment opportunities inevitably shrinks. This is an issue for all fund managers, and something Buffet has noted in annual letters. Berkshire now has a market capitalisation of around US$350 billion, and even with global markets to fish in, that’s a lot of capital to deploy.

- It seems reasonable to expect that markets do become progressively more efficient over time. Natural selection means that successful investors, practices, and innovations will attract increasing amounts of capital, while the less successful lose relevance. This is perhaps a double whammy for Berkshire because a more efficient market can be expected at the large end of town, meaning that increasing size pushes Berkshire into a more efficient and more limited investment universe and that limited universe becomes even more challenging over time.

- Finally, there is no doubt that Berkshire’s success has spawned a great many investors looking to follow a similar path. Over long periods of time Buffet’s willingness to share his investment wisdom may be contributing to the challenge Berkshire faces. Even without this sharing of wisdom, it is likely that there would be an army of followers seeking to adopt a similar philosophy.

We can’t tell from this what the future returns from following a Buffet style investment approach might be, but there are a couple of points worth keeping in mind:

- Scale is your enemy, and having a smaller pool of capital to deploy is a definite advantage; and

- Simply following an approach that has worked for others is unlikely to provide a material investment ‘edge.' The Buffets of the future will probably not be those that emulate Buffet. They will be innovators who see things that others have not seen and invest in ways that others do not.

Who’s up for a challenge?

Contributed by Montgomery Investment Management: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

4 topics

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment