Is 'Value' Investing Now Dead?

Most investors in Australia, be it consciously or otherwise, are "value" investors.If you haven't figured out what type you are, consider the following two propositions: 1) a share price drops by -20%; has your interest been triggered?; 2). a share price rallies by 20%; do you now think 'this horse has bolted, I am looking elsewhere?'...

If both your answers are affirmative, you are definitely a "value" investor. As such, you are in good company, including Benjamin Graham, Warren Buffett, and a large majority of local investment professionals. Many tomes of academic research suggest value investing leads to superior investment returns over time, but the harsh truth is it does not always work so well.

The past five years have frustrated many value investors, in particular the past eighteen months. Stocks like AMP (AMP), G8 Education (GEM), Automotive Holdings (AHG), Greencross (GXL), JB Hi-Fi (JBH), Reckon (RKN) Primary Health Care (PRY), and numerous others also including Telstra (TLS) and the major banks seemed to offer excellent "value" throughout the period but apart from temporary rallies here and there, these share prices have mostly not kept up with the broader market, if they didn't end up becoming cheap-er after a while.

Explanations as to why are plenty and varied; from an overdose in passive investment products (such as the popularisation of ETFs) to short term focused strategies simply chasing positive momentum stocks into irrational, bubble-like territory. Surely this global chase for momentum is but a precursor to the next day of reckoning for investors who keep throwing caution in the wind, forgetting everything has both a price and a valuation?

Maybe.

In theory the most important virtue for a typical value investor is patience. Whatever has caused the share price to weaken shall be resolved over time and thus the share price will respond accordingly, pulling higher and providing the patient investor with a handsome reward. But what if corporate life anno 2018 has become a lot more complicated than that? Can investors still assume that whatever made Warren Buffett wealthy and famous still applies, or are we genuinely witnessing the death of value investing in the share market?

For good measure: simply buying a stock because it has fallen in price is always and under all circumstances a high risk proposition. Those who bought shares in Retail Food Group (RFG), AMP, and BlueSky Alternative Investments (BLA), among many others, have found this out the hard way. These shares have been sold down savagely, but for good reasons, and a lot will have to change before investors can recoup their losses, if ever.

Yet, the risks involved are not always company specific and not always that easily identifiable. For years I heard fund managers talk about how "cheap" shares in accountancy software provider Reckon were, with the share price bobbing along $2, paying out an above average dividend yield, and franked too!

Yet this story has come painfully unstuck as the pressure from much better equipped competitors Xero (XRO), MYOB (MYO) and Sage has proved too much for Reckon. By now, profits are down, dividends have been cut, the share price has more than halved, in particular since a plan to merge operations with MYOB met opposition from the ACCC, and investors are now doubting the longer term survival of the business.

Investors who bought shares in Healthscope (HSO) or Gateway Lifestyle (GTY) may have been "saved" by the emergence of a corporate suitor, the chances for a similar get out of jail-solution for Reckon seem rather slim.

Taking a broad perspective on things, investors wouldn't be completely out of line if they used the predicament management at Reckon is facing today as a template for the share market overall. Frankly, I am quite surprised about how many market analyses and commentary has been released in months past suggesting a new bubble is building in technology and in growth stocks, worldwide, without any mentioning of what is holding back investors from en masse jumping on board the share market laggards.

In simple terms: the global economy is transforming under the weight of debt, low but rising interest rates, demographics, political populism, social inequality and technological advances, and some companies are ready for the future, benefiting from the many changes that are taking place, and others are not.

Faced with the above proposition, where would you put your money?

This has led to the rather unusual situation whereby stocks that had rallied by 20% simply went on with it and added a lot more as more time went by, whereas investors who jumped on stocks after they'd fallen by -20% have mostly been forced to remain patient or change strategy.

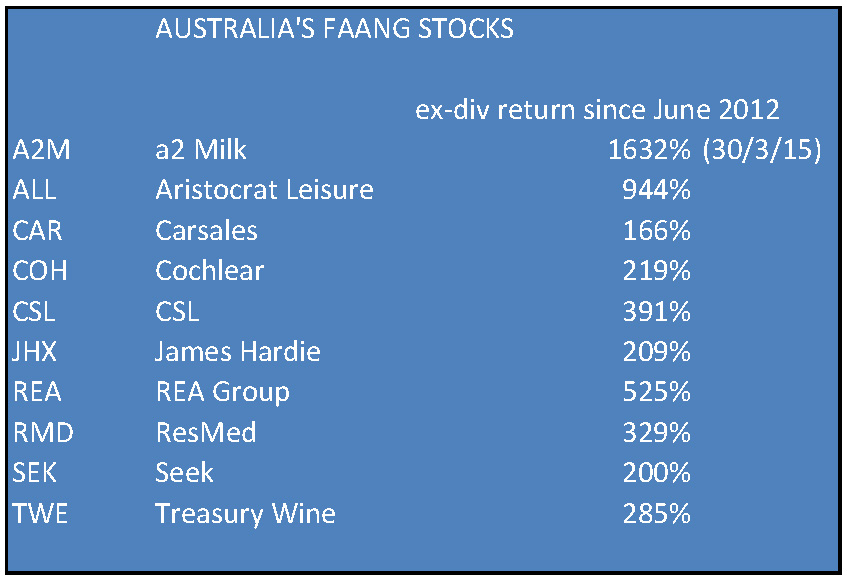

Witness, for example, the numbers I compiled earlier this year for ten of Australia's best performing members of the ASX100 (see overview below). The calculated returns assume share prices had been bought in mid-2012 with a Buy-and-Hold mindset throughout the full five and a half year-plus period. The lowest return, ex-dividends, is the 166% achieved by Carsales (CAR).

Bottom line: inequality is not just something that is ripping apart modern day societies; it is alive and well inside corporate Australia and in the share market as well.

One of the prime examples in the Australian share market, included in the table above, is Aristocrat Leisure (ALL). Having witnessed the share price rise from below $10 in 2015 to now above $30 by mid-2018, investors could be forgiven to think the next item on the menu will be a serious fall-off-the-cliff experience for shareholders who've fallen in love with the stock.

Yet most analysts covering the stock have put forward a valuation/price target in the mid-$30s, suggesting double digit percentage returns post the incredible gains achieved to date remain justifiable. Analysts at Deutsche Bank have a price target of $41. Admittedly, Aristocrat Leisure does not operate in a vacuum and risks are always present that something, somewhere -unexpected or otherwise- can disturb or interrupt this Australian born success story, but recent indications are this company remains on a roll, and management continues executing well.

Quite remarkably, after all those gains, and with the share price near an all-time high, the forward implied Price-Earnings (PE) ratio on the basis of current market consensus forecasts is still only 22.5x (FY19), with the added benefit from a potentially weaker AUD/USD.

So what is it that makes Aristocrat Leisure so different from, say, Metcash (MTS), Telstra, or CommBank (CBA)?

Management has turned Aristocrat Leisure into the number one pokie machine operator in the world, which is why local competitor Ainsworth Gaming (AGI) is doing it so tough, despite seeking refuge under the wings of Austrian gaming technology company Novomatic. See also Ainsworth's share price: same story as what happened to Reckon applies here, including fund managers climbing on board the "cheap" looking valuation.

Most of all, the global market for "one armed bandits", as critics describe the poker machines that over-populate Las Vegas and Australian RSL clubs, is considered a mature market and increasing market share through superior products can only stretch that far, which is no doubt why management has moved Aristocrat Leisure into digital gaming. Post recent acquisitions, here Aristocrat's global market share is still only 2% with this segment growing at fast pace. The company has effectively secured itself a strong growth engine which, if executed correctly, offers loyal shareholders many more years of ongoing strong growth.

This is, in a nutshell, the key difference that separates the Haves from the Not Haves in today's corporate world. It is harsh judgment, but accurate nonetheless. This is not, however, a static proposition. Those who have been caught sleeping at the wheel while the world around them was changing rapidly are today being forced into action, and this process has already started.

Wesfarmers (WES) is spinning off Coles with the promise of turning itself yet again into a higher growth vehicle. Already, investors have rewarded the company by pushing the share price outside the range that had been firmly in place for many years. Telstra is cutting its dividend and re-orienting the corporate strategy. Major banks are selling non-core assets. Additional investments in technology will be next. InvoCare (IVC) is investing more in the business and has started acquiring smaller players outside the main cities. Ramsay Health Care (RHC) just launched an unsolicited bid to acquire Gothenborg-headquartered Capio AB.

These actions should all be seen as attempts by respective management teams to steer their businesses away from the bleak future that lays ahead for the likes of Reckon, Ainsworth Gaming, Retail Food Group, and iSentia (ISD). Hopefully the end result will be a lot closer to what Aristocrat Leisure, ResMed (RMD) and a2 Milk (A2M) to date have achieved, but this is by no means guaranteed.

Understanding these dynamics is today understanding the valuation gap between winners and laggards in the Australian share market, and the differences in respective risk profiles.

Investors who had been accustomed to owning shares in old economy blue chips tend to underestimate how much growth can be achieved from success stories such as CSL (CSL), Aristocrat Leisure, and a2 Milk, and for so much longer too. On the other hand, any concerns about investing in stocks trading on a higher PE can be easily dismissed with the observation that lower PEs did not prevent CBA shares to fall from $96 to below $70 not that long ago, or Telstra shares to more than halve in three years time.

Within this context, I note Morningstar analyst Chris Kallos updated his thoughts on CSL last week, deciding the company's breakthrough medicine candidate CSL112 is ready to be included in today's valuation modeling, with the odds in favour of CSL launching the next potential blockbuster addressing recurrent cardiovascular events in the first 90 days following an initial heart attack by 2023. This area is currently not well covered by existing drug therapies and success would grant CSL a significant first mover advantage.

Morningstar has decided fair value for CSL shares is now situated at $200, but success with CSL112 can potentially move the dial to $250. Failure would pull back fair value valuation to $140, all else remaining equal. In addition, favourable currency movements remain a key sensitivity for the shares with every 1c move in the AUD/USD cross translating into a $2 move in the share price.

Of course, shares in online retailer Kogan (KGN) just lost -30% in only a few weeks time (management sneakily tried to pump up the share price so it could offload some equity). Blackmores (BKL) shares went from $206 to $91, to $171, to now around $145. And shares in Domino's Pizza (DMP) have covered everything in between $77 and $39 since August 2015. These are all high PE stocks, as are Ramsay Health Care and InvoCare, no doubt fueling anxiety that shares not purchased at bargain basement level pricing must come crashing down, eventually.

Maybe the real message here is that a society and economy in transition have radically altered the risk profile for companies listed on the stock exchange. For investors the key is to understand that, while not every share price that falls in price becomes automatically a great investment opportunity, not every outperformer today is doomed for failure and punishment next.

The upcoming August reporting season should prove exactly that.

The biggest mistake investors in Australia have made in years past is assuming that value investing equals investing. Full stop. This is a mistake investors in the US are less likely to make, and with good reason.

FNArena offers self-managing investors and professionals proprietary tools and insights to support their own market research and analysis. The service can be trialed for free (two weeks) at (VIEW LINK).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

FNArena is a supplier of financial, business and economic news, analysis and data services.

8 stocks mentioned

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

Comments

Comments

Sign In or Join Free to comment