This rally is a little too fast, too furious for Tom Millner's liking

Tom Millner of Contact Asset Management was already cautious heading into 2020 given the ASX's pre-coronavirus surge was being driven by investors hungry for yield.

In the December quarterly update for his ~$1 billion listed investment company BKI (ASX:BKI) Tom was concerned about P/E multiples approaching a stupefying 20x despite stagnant earnings.

"We are again wary of the market expectations of earnings for the year ahead. Very rarely does the market get the earnings per share forecasts right. Curiously, lower interest driven market multiple expansion has broadly offset weaker earnings per share outcomes."

His caution proved correct as the bull market was slain, prompting BKI to start buying when the ASX was off 35% from its peak. But instead of celebrating buying close to the bottom, Tom's sharing his father Robert's sentiment in moving back to the sidelines and holding cash.

Tom was kind enough to join us on Microsoft Teams for an interview to discuss why he reckons investors are being lulled into complacency given the unpredictability of the situation and more topics:

- How his cash weighting has moved

- What surprised him about March

- Why investment process is King, especially in the current environment

- How he's dealing with stocks that have cut dividends

- 6 stock ideas that he has utmost faith in dividends being held or increased

- When BKI would be fully invested again

Watch below the full interview with Tom or read the Q&A below. (Note: This interview was recorded on 7 April 2020).

Tom, are you seeing value emerge in Australian equities after recent share price falls?

We sold a few smaller positions in the reporting season on an ex-dividend basis. In hindsight that probably wasn't enough, but when the market fell 35% from the peak we put our toe in the water, and started buying a few things. However, the markets have rallied quite significantly. It's up over 15% from the bottom, so we're back on the sidelines watching. We think there's a huge disjoint between current market prices and valuations and what we're actually seeing in the market. So we don't really know where all this is going to end up yet. So we're probably back on the sidelines at the moment.

How has your cash weighting moved over the last few months?

Once we paid the dividend in February to BKI shareholders, we had cash of probably 3.5- 4%. We lodged our NTA for March on 7 March 2020. It shows that cash is about 7% we think with the dividends that we are receiving the next few days, few weeks, we'll be at probably 8% cash.

Was the increase in cash prompted by the rebound being too far, too fast?

A bit of both. I think when you've got someone as experienced as my dad on the investment committee at BKI and Soul Patts, you listen to his comments when of tells you to be patient and make sure you've got cash on the sidelines, so that's what we've done. We don't like buying uncertainly though, so we haven't really pulled the trigger on a lot of that yet, and the current economic situation is probably going to get a little bit worse we think before it could get better.

Our unemployment rate could go to 10-15% of this country, supply chains across the globe need to be re-instated, human behaviour might change permanently.

Using Microsoft Teams and Zoom and all these programs have been an unbelievable way to access technology. But cities, airports, offices, schools across the globe, they're all closed. So we're probably going to see this situation go on for another 3-12 months. So we don't really know where we're at at the moment, but what we do know is that at the GFC we came through this and long-term, patient investors were rewarded with some pretty good opportunities.

Is there something that surprised you in particular about what happened in March?

We've had a big fall, but then you've seen a big bounce from the lows. The volumes that we've seen have been quite substantial. The ASX only yesterday announced that the average daily trading was up 96% from memory year on year. So there's some big figures.

We don't really understand the rally that we're seeing, given the fundamentals that we're also seeing in the market, but we do understand there are a lot of ETFs and index funds that need rebalancing day by day. We understand that moves in oil, iron ore, gold, for example, have had an immediate reaction on all those stocks that directly correlated to those commodities, and I think if you go back three, six months to the low rate environment we're in and chase for yield, that argument does still play out. It's probably got a bit better in some instances, rates aren't 75 basis points anymore, they're 25 basis points. Investors are searching more and more for income because they need that to live on. TDs are still only probably 1.6, 1.7%, so we can see investors going into the market looking for yield.

The trouble we've now seen the last couple of weeks is dividend cancellations, deferrals, these are probably going to be ongoing for a little bit longer yet, and if you saw, remember the GFC, a lot of companies did cut their dividend.

What are some of the qualitative factors that are important to you in the current environment?

At Contact Asset Management, BKI and SOL, we've developed five main strategies to look at a stock in any environment.

1) Principal activity

The first is their principal activity. We need to know what that company's competitive advantage is and if it doesn't have one in these environments it gets found out pretty quickly.

2) Income

Step two is income. We've found over the years that companies that offer a sustainable and growing dividend stream are usually or quite often the ones that are a bit better quality anyway.

3) Balance sheet strength

That income piece ties into the balance sheet - you're only able to pay sustainable and growing income if you've got a strong balance sheet. So we're always wary of companies with over-geared balance sheets.

We saw it in the GFC, it's playing out now. The companies with weak balance sheets have to come back to the market, they dilute existing shareholders and it's very very unattractive to us.

4) Management

Step four is the management, we spend a lot of time on assessing the management and board skillset. We place a lot of weight on alignment because we like to co-invest with managers.

5) Valuation

Once we've run through all that, we get to valuation and that's where we're looking at earnings profiles, EV/EBITDA multiples and running discounted cash flow valuations.

It's a very rigorous process. It's pretty disciplined and our process is very repeatable. So we run it across all our companies and I think at the end of the day, you've got to know what you're buying. At the moment, we don't really know what that earning stream is for a lot of our companies. So it's leaving the valuation piece a little bit untold at the moment, unfortunately.

Given the unprecedented amount of earnings guidance withdrawals and economic conditions, how are you navigating cash flow forecasts?

We've tried to keep the process as much as we can, but it's definitely been challenging. But we've got a great team at Contact, there's nine of us, we've got a really, really good board at BKI and a good investment committee. We've got a lot of access through the Soul Patts group of companies. So my fellow PM, Will Culbert and I are just trying to encourage our team to get on the phone, talk to as many people as we can.

The whole market's not shut, Reece (ASX:REH) had a call yesterday, a few of us jumped in the car, went up to a few showrooms and had a talk to the managers of those businesses to try and get a good feel on what's happening with that business. It's difficult but we're just trying to be as annoying as we can on the phones and trying to test as many theories as we can.

BKI's objective is to invest in high-quality stocks that provide growing income. How are you dealing with cancelled dividends?

It's a really good question. I think the timing of it is interesting, you've had reporting season where companies have reported their half of full-year result. They've declared a dividend and in some cases have even gone ex-dividend. So you'd think that dividends completely banked yet the day before they pay it, they've cancelled it or deferred it. So it's been a very difficult one to watch.

As an investor, you really do need to be focused on those companies who, even in this environment, have a bulletproof business. A company who's still in operation, still producing good and real cash flows, has a strong balance sheet as we mentioned before, not just to survive but to actually use that to generate cash.

A company that's well managed, situations like this make or break management teams and that's why a good quality management team is very important, and with all that then has the ability to continue to pay dividends.

There's been a few that's surprised us on the downside. I think Seek (ASX:SEK) and Harvey Norman (ASX:HVN) on the downside have probably disappointed us, but we understand why they've done it, but there's a lot of stocks that fit this criteria at the moment and are doing well.

You've got Woolies (ASX:WOW), Coles (ASX:COL), Wesfarmers (ASX:WES), TPG (ASX:TPM), Telstra (ASX:TLS), ASX (ASX:ASX), CBA (ASX:CBA), Ramsay (ASX:RHC), Sonic (ASX:SHL). WIthin resources, you've got New Hope (ASX:NHC), BHP (ASX:BHP) and then transport Lindsay Australia (ASX:LAU). So there's probably a dozen names that we own that are still doing pretty well in this time.

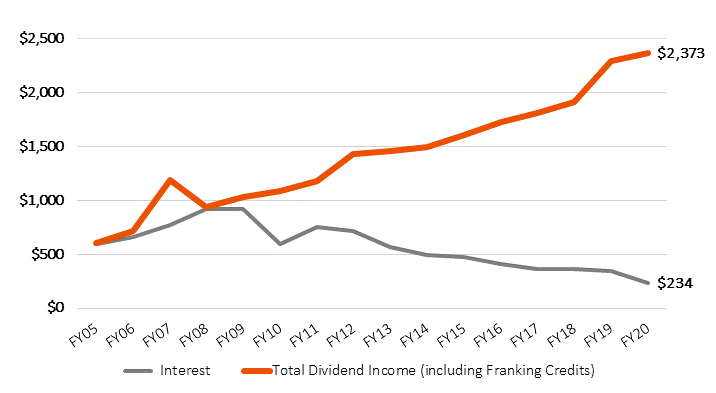

I think the important thing to note for LICs is as well is the traditional guys under the company structure can smooth dividends, and we've done that before, did it through the GFC and talking to BKI, we've got retained earnings of about $35 million and surplus franking credits that we can pay out to shareholders over time. (Ed's note: Tom also provided a chart that highlights the benefit of receiving a fully franked dividend in a falling interest rate environment below).

What's your response to a holding that cuts its dividend?

As long term managers we do have the ability to look through the cycle and hold these companies, if we, I suppose trust management and believe that they're holding that capital back to benefit shareholders in the longer term and with the Harvey Norman management team and the Seek management team, for example, we do trust them, we do believe in them. They've got a great history of creating shareholder wealth over a long term. So, it's not nice that we don't receive that dividend over the short term, but longer term by holding the capital back and making a business model stronger, it'll be beneficial for shareholders longer term.

What are a couple of stocks that you have utmost faith in and see dividends being held or increased as we go through this cycle?

Yeah, there's a couple. I think what we've seen with the stay at home strategy is that people are obviously having to eat at home and not in cafes and restaurants as we've become accustomed to.

'Stay at home' stocks - Companies like Coles and Woolworths in particular, they'll produce some pretty good results we think for the six months. The do-it-yourself market is very well suited to Wesfarmers and their business, Bunnings.

Demand for data - The strain on data, TPG and Telstra, we think their business models are going to be underpinned by the next six months.

The one bank to own - From a banking point of view, CBA is far superior to a lot of the other banks in the marketplace. They're very well capitalised, they've been, I suppose, preparing themselves for a situation like this and management has done a very good job in positioning the bank with a lot of excess capital over the last few years. So we're very confident in CBA's position as well going forward.

Last question, when do you think you'll be fully invested in again?

I think what we're looking at is some global benchmarks if you like, we're looking pretty closely at South Korea. We're looking pretty closely at Italy, they were the first countries that went through this virus crisis to start with, so we're looking to see how quickly they come out of that and how well they manage it. Once we do that, we'll obviously have to start looking in our own backyard and there's a lot of companies that have been hit quite significantly through these shutdowns. But we'll get through this, we've got through this before.

There have been many crises worldwide before that we've got through and then I think what you see then is a reset in society. Many companies will become, fit for purpose, they'll have better, stronger balance sheets, they'll have a more experienced management team that will ultimately lead to a better business and they'll be able to survive the next 8-10 year cycle, whatever it happens to be.

While we wait for that, we'll accumulate cash and like with most opportunities the fortunate investor is the most patient and the one that can look longer term.

Click FOLLOW for more

If you enjoyed this interview, please hit FOLLOW to be the first to receive my next fund manager interview straight to your inbox.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

5 topics

15 stocks mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management