Like investing in the Titanic

Much has been made of the increased popularity of passive investing, and rightfully so. Markets have generated excellent returns over the long term, and index tracking Funds or ETF’s provide very low-cost exposure to highly diversified portfolios. However, in this wire, we explain what it has in common with investing in the Titanic after receiving news of it sinking.

First, a brief history of passive investing:

Though there is some contention around exactly what defines Passive investing, for the purposes of this article we’ve defined it as an investment strategy that seeks to track the returns of an index. This is most often achieved through an ETF or Fund that purchases the underlying companies that make up an index.

In essence, the philosophy of passive investing is that the markets are efficient. That based on all the available information, share prices are accurate, and that attempting to find mispricing in share prices is an endeavour in futility.

Active investing is the endeavour to outperform the market. Simply put, active managers enlist strategies seeking to take advantage inefficient markets. The belief is that markets are often inefficient, and with proper consideration and effort a manager can identify mispricing and take advantage of them.

The concept of an index fund was first discussed as an academic concept in the early 1960s. However, due to a lack of interest, it wasn’t until 1973 that the first index tracking fund was available for institutions. In 1975, the first index fund was opened to retail investors, but again interest was not significant and it wasn’t until the late 1980’s that Vanguard was founded and the first index fund (a bond fund) gained traction.

Though indices have existed for over 100 years, it was uncommon for financial commentators to note them. In fact, until relatively recently financial commentators would discuss the markets by making reference to specific companies and their share price movements. In an effort to make financial news easier to digest, commentators in the 80’s began using the index (rather than individual shares) as a proxy for whether the share markets were strong or weak over a given period.

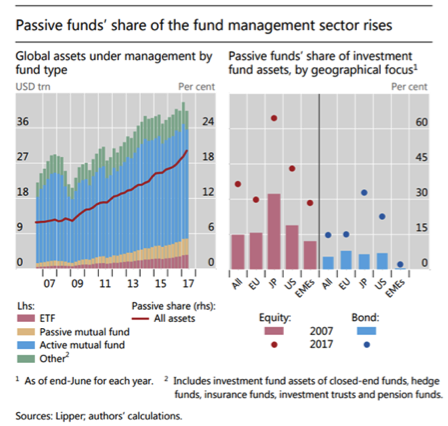

By 1999, investments in index funds surpassed a valuation of $100 billon.

Today some 45% of US investment fund assets are officially invested in index funds, with some experts suggesting that at least that many again are shadow index funds.

A Shadow index fund is a Fund marketed as an active investor, but in fact tracks the index to avoid material underperformance of its peers

If shadow Index Funds are included, the following charts suggest that as much as $16-20 trillion (out of $40 trillion of global assets) are managed passively. In the USA, passive investing might account for as much as 90% of the market.

A deeper look:

The key benefits of investing in index funds are explained by their proponents as follows:

- Investors can gain access to a truly diversified portfolio with very little effort.

- In strong markets, many investors are happy with ‘market returns’, generated with minimal volatility.

- Historically, active managers have underperformed the market.

- Due to the scale and mandate, index funds have incredibly low fees.

Let’s break down each of the points:

A Diversified Portfolio:

An index fund buys every company in the index in accordance to their weighting in the index.

There is no effort to discover price, there is no consideration for value, the Fund will simply buy the appropriate weighting of every company in the index.

In following this approach investors receive exposure to a truly diversified portfolio. The trouble is this includes all companies in the index, many of them sub-par.

Market Returns and Under Performance of Active managers:

In an environment where every investor contributes, half the market participants will outperform the market, while half will underperform it (as defined by the law of averages). However, when fees are considered, the scales are tipped ever so slightly in favour of underperformance. After all, market returns do not account for the cost of achieving those returns. Once fractional costs are added, even index funds must underperform the market.

Every investor in an Index Fund must underperform the index by at least the cost of its fee. One cannot simply earn the index return by investing in an index fund. Rather the costs of maintaining an index fund guarantees that investors in them will underperform. Nevertheless, for some investors, those returns suffice.

Lower Fees

Lower fees remain one of the strongest selling features of passive funds. This tends to be true (although the Collins St Value Fund has zero fixed fees) for good reason. The passive manager does not take risk, they do not have scope for creativity. The manager of an index fund does nothing more than direct capital as prescribed by the index. Comparing the roles of active and passive managers is like comparing a Kmart wall print with a Picasso. Both may brighten a room, and both may technically be art, but the similarities end there.

Risks and Consequences:

Subject to comfort with below average returns, an index fund is a useful tool for the uninformed. They provide lower volatility than traditional funds and provide an avenue to gain exposure to broad economic activity. As Warren Buffet has stated in the name of his teacher Ben Graham, “for the vast majority of [uninformed] investors, the index fund is a most sensible investment.”

The trouble with index funds

Index funds do not add value to the market by discovering the intrinsic value of companies. Instead, they piggyback off the efforts of traditional investors. As companies grow traditional investors support them, thereby increasing the share price and size of the business. Those businesses then become incorporated into an index, after which it is adopted by index funds.

There are two key issues with index funds:

- There is no mechanism on the sell side

Once a company enters an index, the index trackers must own that company. It does not matter if the underlying business is poor, so long as the company maintains its position in the index the index fund will continue to hold or buy the company.

The issues arise when a company’s market cap is being propped up specifically by the weight of capital entering the markets from index funds.

It has been shown that there is a correlation between a company position in an index and its valuations, that is, companies included in major indices carry higher valuations (as illustrated by share price increases after becoming a part of an index, and visa-versa). This is a concern over the long term.

Given the time, listed company share prices tend to align themselves with the businesses underlying fundamentals. Businesses buoyed by the flow of capital into index funds can significantly overshoot their underlying value and can expect the reversion to value to be just as ‘significant’.

- Increased Volatility

As capital continues to flow to passive funds, ETF’s and shadow funds, fewer traditional investors remain to discover price inaccuracies. Whereas once 90% of market participants were actively looking for price discrepancies, some data would suggest that as much as 80% of current market participants are simply index followers leaving just 20% of participants setting prices.

As a result, mispricing creeps into the market generating more volatility. There is a strong correlation between the increased popularity of automated investing like index funds, and market volatility.

Though volatility in its own right is not an issue that concerns us, it is a symptom of a less efficient market. Prices being moved by the flow of capital without regard for business fundamentals is likely to further increase market volatility and divorce markets from efficient market theory.

Final thoughts:

Investing in passive index funds is essentially the process of buying yesterday’s winners and ignoring news about upcoming impactful events. It’s a little like investing in the future voyages of the Titanic after receiving news of its sinking. It seems a little unwise.

Grounded in the concept of efficient market theory – that is the theory that all market prices are exactly as they should be based on all the available information - an index fund relies on the work and price discovery of stock pickers. Without market makers in individual companies, the concept of an index simply fails over time.

As a small proportion of invested capital, index funds provide an attractive avenue for uninformed investors to gain access to the broader market. However, at the point that the weight from index funds begins to dictate prices (as evidence would suggest is currently the case), index funds run the risk of becoming the victims of their own success. That is, those funds most heavily invested in companies propped up by index capital will most feel the effects of a return to efficient markets.

We are not great proponents of index funds. We believe they detract from the efficiencies of the market, increase the risk of volatility and long-term capital loss, and guarantee that investors who invest in them underperform the very ‘average’ they are trying to achieve.

Nevertheless, we understand their attractiveness. During times where volatility is low and the global outlook clear, index funds provide enviable diversification to economies without the need to expend energy attempting to find specific high-quality companies.

However, if investors believe we are living in predictable and calm times I would encourage them to read a newspaper.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is the MD and one of the founding partners of the Collins St Value Fund.

The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by Mercer in 2019 & 2020.

With no fixed management fee, the investment team only benefit when our investors do.

1 topic

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management