Livewire Summer School - An essential guide for commercial property investing

APN Real Estate Securities Group

APN Real Estate Securities

Take a quick look out of the window. If you live in the country and all you can see are fields and trees, well, lucky you. But if, like most Australians, you live in a city, you’re probably gazing at rooftops and maybe a few apartment blocks.

You’re probably familiar with how investing in assets like these work. You take out an investment loan and negatively gear your purchase, hoping that the capital growth will offset a meagre rental return and maintenance charges.

But what about those taller buildings in the distance, closer to the city, or your local shopping centre and office park? They’re expensive to build and maintain. But that doesn’t mean only the very wealthy can profit from them, leaving the rest of us to play on the residential property merry-go-round.

The commercial property sector is focussed on delivering an attractive yield first (from rent collected) with capital growth second. Whilst the foundation of both residential and commercial real estate is ‘bricks and mortar’, commercial property investing is a very different proposition to residential property.

For starters, you have more choice

In addition, there are opportunities to invest in retirement living, leisure parks and hotels. Whilst the range of investment choices is attractive, it raises two questions: first, how can an ordinary person invest in buildings that can cost tens and sometimes hundreds of millions of dollars? And second, even if you do have the money, who has the time and expertise to manage them?

Australian Real Estate Investment Trusts (AREITs) allow investors the opportunity to access a wide range of commercial property which delivers regular, hassle-free income to ordinary investors just like you.

It works like this. When you buy an interest in an AREIT you’re buying a slice of a commercial property portfolio and the dividends and capital growth it delivers, without the risk of purchasing and owning a commercial property or portfolio yourself.

As for the property management - the capital improvements, rent negotiations, tenant relations, maintenance, accounting and legal compliance - that’s covered by professional managers paid to deal with these headaches so you don’t have to.

In this way, investors can receive a regular distribution, from their investments in commercial property, without lifting a finger or making a huge capital outlay.

“The major benefit of A-REITs is that they can provide access to assets that may be otherwise out of reach for individual investors, such as large-scale commercial properties. A-REITs may appeal to investors looking to diversify their portfolio into property with potential to receive a regular and consistent income stream.” – The Australian Securities Exchange

So, now you know that you don’t need to be a billionaire to invest in commercial property and can enjoy the benefits of doing so without the hassle, another obvious question arises: if commercial property is so good, why do most Australians opt to invest in residential property instead?

Residential versus commercial real estate

The intention behind the investment is the biggest difference; because effective cash yields are typically lower, residential property investors are in effect banking on higher capital growth to compensate for a yield that may not beat inflation. Commercial property, meanwhile, is regarded as a defensive investment due to the predictability of rental income and cash flows, even during volatile economic conditions.

If you’re happy to assume that residential property prices will continue to rise and you’re okay with an effective cash yield not much better than that paid by a risk-free term deposit, fair enough. There are many people making the same choice, in which case commercial property may not be right for you.

But if your focus is on a higher, more stable income from which you can cover day-to-day living expenses, plus a little capital growth on top, commercial property may well be a suitable choice.

Does that mean the benefits of a stable, regular income come at the expense of total returns? Not at all.

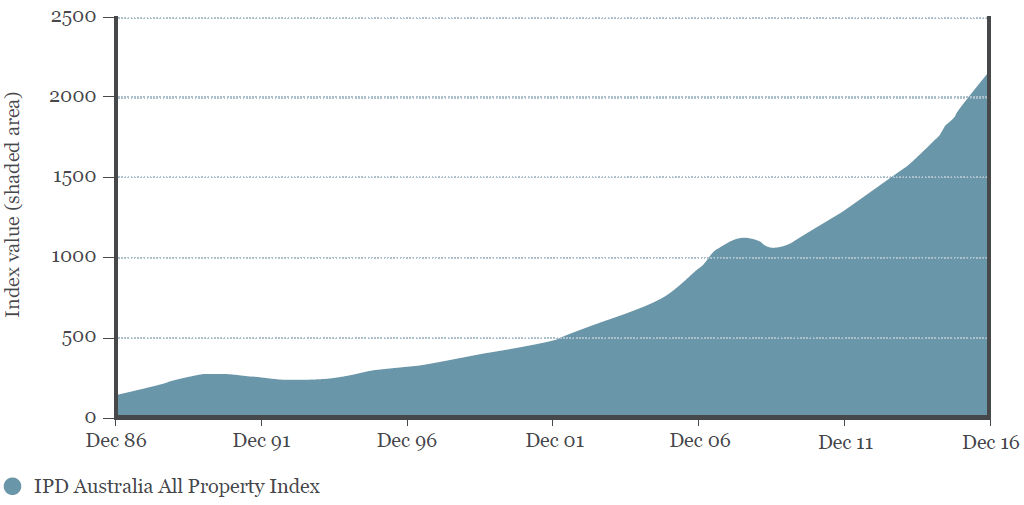

Commercial property has delivered an average annual return of approximately 10.4% pa for the last 30 years.

Commercial property - an excellent defensive investment

It’s a good idea for you to understand the three main reasons for the sector’s defensive attraction.

1. Rent is predictable; a business’s profitability is not

Shareholders in BHP or ANZ receive a dividend only if the business makes a profit. If times are good, everyone’s a winner. If not, the dividend may be cut or halted altogether. When cash flows are volatile, so too is the income paid to shareholders.

Now think of the rent these companies have to pay for the premises they occupy; the commercial offices, warehouses and retail outlets. These businesses cannot run their businesses without these premises; they are essential for them to be able to operate and generate sales. BHP and ANZ must pay rent to the owners of these properties whether they’re profitable or not. And they must do so each and every month, whether cash flows from their businesses are strong or weak.

For commercial property investors this is the source of the sector’s defensive strength. Income from property trusts can be relied upon each and every month, while dividends from ordinary listed companies cannot.

2. Long contracted lease terms provide reliable income

In residential markets, lease terms often run for just a year. In commercial property they’re usually contracted over five years and it’s not uncommon for 10, 12 or even 15 year leases. In addition, and in stark contrast to residential property, rents cannot usually fall over the period of the contract.

It’s the rent collected from tenants, secured by long term lease agreements, that delivers the distribution of relatively high, sustainable income to commercial property investors.

3. Regular rental increases provide a defence against inflation

In commercial property there are up to three ways in which rents can be increased (but not reduced) over the lease period:

- A rental review can be triggered by movements in the consumer price index, the traditional measure of inflation

- Contracts may offer provision for a fixed annual increase in rent, agreed between the landlord and tenant at the time of the lease agreement;

- A review based on a calculation of ‘current market rent’ agreed between the landlord and tenant (or possibly by a property valuer if a dispute arises).

This is not to say that rents can’t go down at the end of a lease, but these regular reviews can mitigate against inflation and make commercial property a defensive investment.

How to invest in commercial property

Before the advent of AREITs, the only way to invest in commercial property was via property syndicates (an illiquid fund) or purchasing commercial property which was an “all or nothing” affair. It was impossible to purchase a part of a shopping centre, warehouse or hospital in a liquid format. Everything was bought and sold in its entirety, which is why to this day many investors think commercial property is beyond their means.

The advent of the listed property trust (AREIT) sector in the 1970s changed all that. Now it’s possible to access commercial property indirectly, buying and selling small parcels of real estate much as one would an ordinary share, with minimal upfront capital commitment.

The sector has since expanded further to cover property securities funds and unlisted property trusts, sometimes known as syndicates, each with their own pros and cons.

Let’s look at each in turn:

1. Australian Real Estate Investment Trusts (AREITs)

You may not know of the term but you will almost certainly know the names. Westfield, Stockland and Mirvac are but three well known AREITs. There are many, many more. In fact, because many investors the world over want reliable, stable yield, each major global sharemarket has its own ‘real estate investment trust’ i.e., ‘REIT’ sector.

There are seven major benefits of using AREITs to gain access to the commercial property sector:

- Easy to build a diverse portfolio with the sector covering thousands of properties

- Simple to buy and sell, tradeable just like ordinary shares

- Low entry costs

- High yields

- Teams of specialist property and investment experts manage AREITs

- Part of the income received from AREITs may be tax effective

- Capital growth is generally consistent with inflation over the medium to long term

As for the risks, these rest largely with you. As with ordinary shares, AREITs can sometimes be relatively cheap and at other periods over-priced. There’s a risk that you might buy and sell at the wrong time.

Then there’s the need for diversification, across the various sectors and geographies. Building a sensible, high-performing portfolio of AREITs requires similar skills to building a portfolio of listed shares. You may not have the time or inclination to acquire those skills.

Finally, there’s the risk that every self-directed investor takes; whilst acquiring sophisticated analytical skills is one thing, applying them successfully at a time of high emotion is quite another.

It’s for these reasons that many AREIT investors decide to pay expert professionals to develop and manage a high-performing commercial property portfolio on their behalf, which brings us to the second way of gaining access to the sector.

2. Property securities funds

Properties securities funds are much the same as managed funds consisting of a portfolio of shares, except they specialise in AREITs rather than ordinary listed companies.

Real estate securities are managed funds consisting of underlying investments in AREITs, which are listed on the ASX, and unlisted property trusts which aren’t.

Both options allow investors to gain access to some of Australia’s highest quality, professionally managed commercial real estate without the need for large amounts of upfront capital.

There are five distinct advantages to using property securities funds to develop your commercial property portfolio:

- Expert management

- Built-in diversification

- Easy entry and exit

- Simple administration

- Minimal time and effort

Of course, these benefits come at a cost. As with ordinary managed funds, most property securities funds charge a percentage based fee of funds under management.

If a property securities fund doesn’t sound like your thing but you don’t want to establish and manage your own commercial property portfolio, there’s one final option for you to consider.

3. Unlisted property trusts (syndicates)

Unlisted property trusts are similar to property securities funds in that they allow you to access a slice of commercial property or properties with relatively little capital outlay, fully supported by a professional property management team.

The big difference is that when you invest in this structure you are only one step removed from direct ownership. That gives you a higher degree of visibility and financial involvement in the properties themselves.

In many cases you can visit the building(s), monitor the performance of corporate tenants and track performance, delivered via transparent unit pricing and regular valuations. Although the day-to-day building operations and asset management rests with the management team, investors receive a share of the rental income (generally paid monthly or quarterly) and ultimately, the proceeds when the property is sold.

Unlike listed AREITs and ASX-listed shares, property syndicate pricing reflects the true value of the underlying assets based on regular independent valuations. But it’s important to note that unlike AREITs and many real estate security funds, unlisted property trusts are generally illiquid. That means your funds are locked in for the term of the fund, which typically are five years or more. Hopefully at the end of the term, the property would have increased or at least maintained its value; however there is a risk that the value declines leading to potentially significant capital losses. Whilst the manager could choose not to sell the property in this instance and trigger a capital loss, that would result in you not being able to access your funds at the end of the fund term. In this case, the term of the fund may be further extended.

Are you the best person to manage your money?

Only you can answer this question. What we can offer are a few pointers based on experience, plus a little research.

- First, building your own AREIT property portfolio requires time, skill and psychological commitment. If you think you might fall short on one or more of these requirements, you might want to think twice about managing your own portfolio. The costs of getting it wrong can be very high indeed. If, on the other hand, you have some investing experience and enjoy the idea of managing your own money, we suggest you start slowly.

- Read the annual reports of big AREITs like Scentre Group (the owner of Westfield in Australia) and Stockland. This will give you a flavour for the issues, management teams, assets and performance measures in the sector.

- Also consider portfolio diversity, macro trends, pricing and the long term strategy of each AREIT because, if you’re investing for the long term, it’s the decisions that are made today that will affect your investment in five years’ time.

APN’s six-strong investment team spend their days down in the weeds of the sector, fine tuning each fund’s investment strategy and risk exposure as well as considering major trends which may impact on different parts of the commercial real estate sector. Please don’t think that you need to follow suit. As long as you’re prepared to accept potentially higher levels of volatility and maybe lower returns, perhaps offset in part by not having to pay a management fee, there’s a chance you can be successful.

For further information on APN, including accessing our funds, please visit our website

NB: The above article is a summary of APN’s “The little book of BIG PROPERTY”. You can download the full guide on our website

This summary has been prepared by APN Funds Management Limited (APNFM) (ACN 080 674 479, AFSL No. 237500) for general information purposes only and whilst every care has been taken in relation to its accuracy, no warranty is given or implied as to the fairness, accuracy or completeness or correctness of the information. APNFM is a wholly owned subsidiary of APN Property Group Limited ACN 109 845 068. APNFM is the responsible entity and issuer of the APN Property Group managed investment products. The information provided in this material does not constitute financial product advice and does not purport to contain all relevant information necessary for making an investment decision. It is provided on the basis that the recipient will be responsible for making their own assessment of financial needs and will seek further independent advice about the investments as is considered appropriate. Past performance is not necessarily an indication of future performance. Returns shown are for retail investors, net of fees and costs and are annualised for periods greater than one year. Returns and values may rise and fall from one period to another. Investors’ tax rates are not taken into account when calculating returns. General risks apply to an investment in APNFM’s funds and must be considered before making an investment. In deciding whether to invest or continue to hold an investment in a particular fund, a person should obtain a copy of the relevant Product Disclosure Statement (PDS) for the fund and consider its content. APNFM recommends that a person obtain financial, legal and taxation advice before making any financial investment decision. Allotments or issues of units will be made only on receipt of an application form attached to a copy of the relevant PDS. A copy of the PDS is available from APNFM, Level 30, 101 Collins Street, Melbourne, Victoria 3000 or by visiting (VIEW LINK).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

APN Real Estate Securities (RES) is a specialist investment manager that actively manages portfolios of listed property securities. Since inception in 1998, our deep understanding of real estate and “property for income” philosophy, together with a highly disciplined investment approach has been the backbone of our performance.

Our team of investment professionals possess real estate experience spanning several property cycles. Our investment decisions are supported by extensive research and valuation processes that have been developed over more than two decades.

APN Real Estate Securities became part of Dexus (ASX: DXS) in August 2021. Dexus is one of Australia’s leading fully integrated real estate groups, with over 35 years of expertise in property investment, funds management, asset management and development.

2 topics

APN Real Estate Securities Group

APN Real Estate Securities

APN Real Estate Securities (RES) is a specialist investment manager that actively manages portfolios of listed property securities. Since inception in 1998, our deep understanding of real estate and “property for income” philosophy, together with...

Expertise

APN Real Estate Securities Group

APN Real Estate Securities

APN Real Estate Securities (RES) is a specialist investment manager that actively manages portfolios of listed property securities. Since inception in 1998, our deep understanding of real estate and “property for income” philosophy, together with...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management