Lower prices ahead for BHP, Rio and Woodside

When we step back and look at the capital flow, liquidity and growth conditions in the world, the implications for the recent run-up in stocks like BHP, RIO and WPL become clear: Lower prices are likely ahead. In measuring global liquidity conditions, we are careful to measure both the ‘quantity’ of liquidity as well as its rate of circulation in the world (otherwise known as ‘velocity’). In this wire we review the key drivers that enable us to form a useful perspective not just around the Australian Resources sector, but also the broader prospects for commodities and Emerging Markets in general.

Daniel Want

Prerequisite Capital Management

“...right now I’m watching the currencies, I’m watching crude [oil], I’m watching stocks and bonds, they’re all interrelated... the whole world is simply nothing but a big flow chart for capital.”

...Paul Tudor Jones (1987)

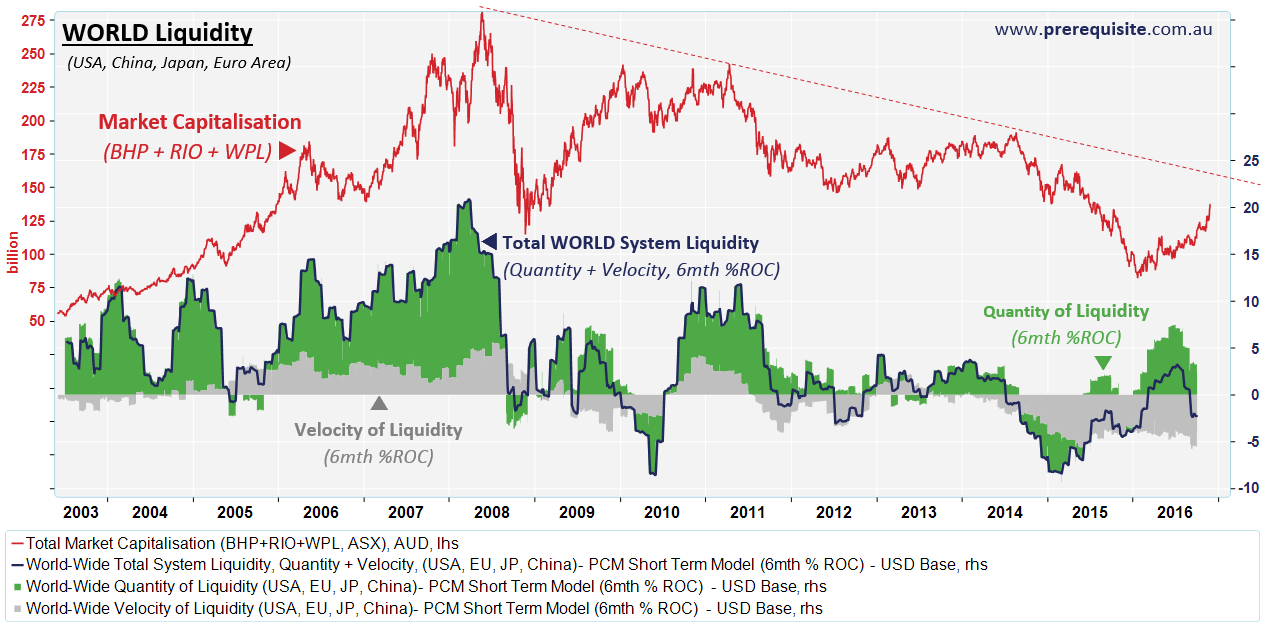

A common mistake analysts can make is looking at quantity expansion in isolation of velocity dynamics. For example, a ‘quantity’ expansion of liquidity (i.e. an increase in the money supply) doesn’t really matter if there is an off-setting fall in the velocity of that money in the economy – falling velocity usually represents a hoarding or risk-averse response by the private sector and at a structural level tends to be indicative of falling productivity. Furthermore, for analysts that do pay attention to the velocity of money, their thinking tends to start and stop at a basic GDP/M2 measure of velocity.

The following chart shows one of our primary models of short-term global liquidity conditions (constructed using central bank and commercial banking system financial metrics from around the world) in addition to the combined market capitalisations of BHP, RIO & WPL on the Australian Stock Exchange.

The above chart suggests that the reflationary bounce in commodity and emerging markets this year is likely to prove transitory, as the falling velocity trends in the world have failed to yet be reversed.

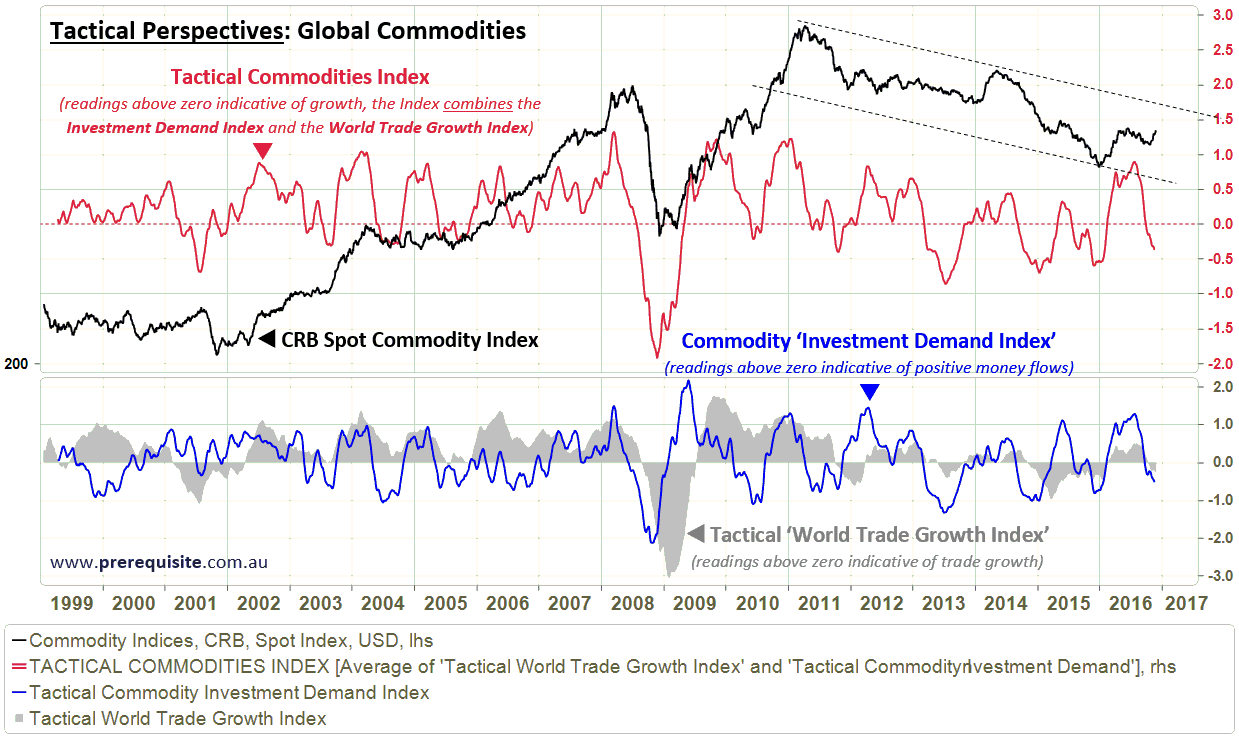

Looking more tactically at the conditions around commodity prices, we see a similar picture arising from World Trade growth conditions and (the capital flow driven) Investment Demand for Commodities – both pointing lower from here after a 2016 bounce.

The Commodity Investment Demand Index is constructed from money flow data into commodity markets around the world, adjusted for the ‘tightness’ or ‘looseness’ of financial conditions as measured by the 6mth rate of change of US 10year TIPS Yields. The Index is proprietary to PCM.

The World Trade Growth Index is constructed from Leading Economic Indicators of World Trade in addition to actual 6mth ROC World Trade Volumes. It also is a proprietary PCM model.

Having both of these indices turning negative, in the context of generally negative global liquidity conditions (see the chart at the beginning of the article), suggests that the 2016 rally in BHP, RIO and WPL is likely to prove transitory (as is the rally in Commodities & Emerging Market Stocks more generally).

Despite popular belief, the broader multi-year commodity bear market is not yet showing signs of abating.

Lower prices are likely ahead.

Exclusive to Livewire, By Daniel Want & Darren Brind of Prerequisite Capital Management Pty Ltd

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

4 topics

3 stocks mentioned

Daniel Want

CIO & Co-founder

Prerequisite Capital Management

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

Expertise

Daniel Want

CIO & Co-founder

Prerequisite Capital Management

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

Expertise

Comments

Comments

Sign In or Join Free to comment