Magellan stays cashed-up amid elevated uncertainty

The S&P 500 is already back to where it was in October 2019. The NASDAQ is less than 5% shy of its pre-COVID-19 record. But the team at Magellan Financial Group ain’t buying it.

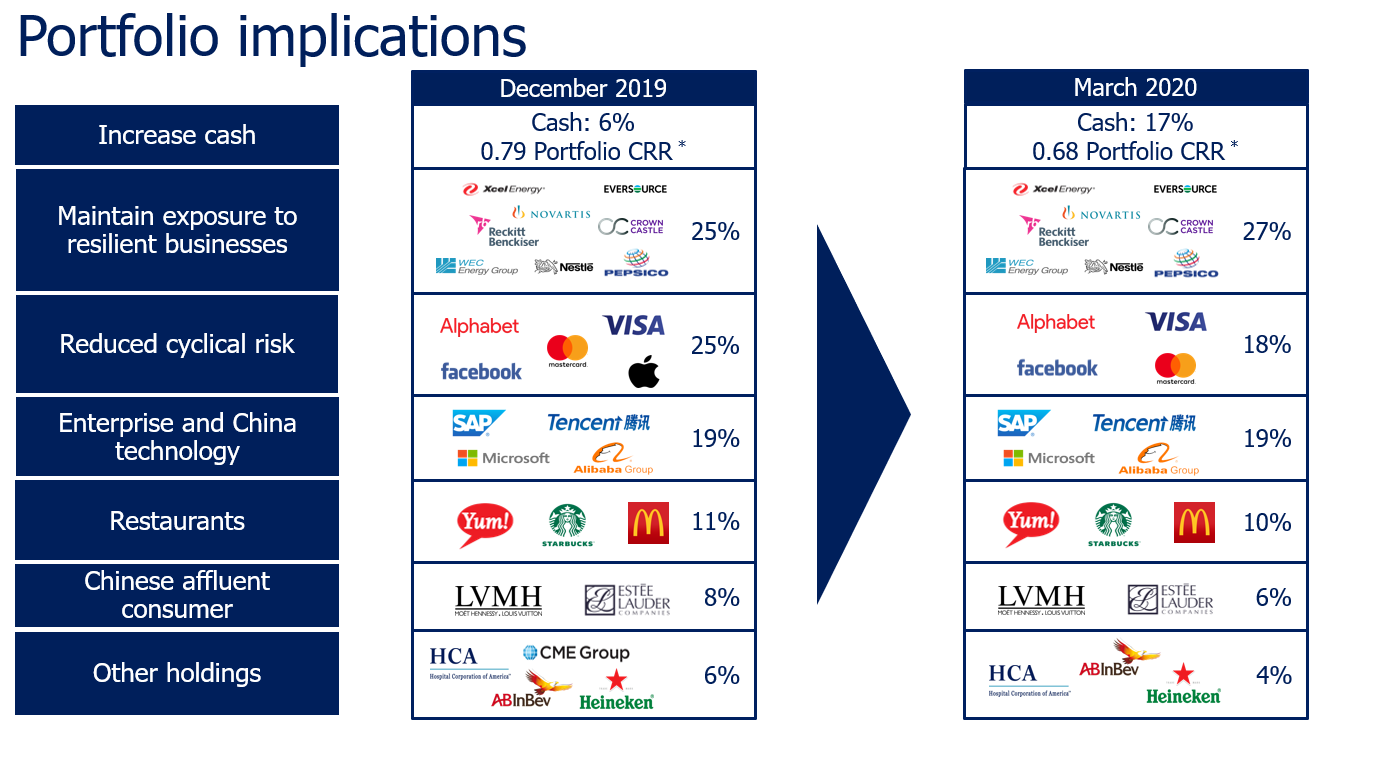

At a recent webinar, Portfolio Manager Chris Wheldon and Head of Infrastructure Gerald Stack revealed they are maintaining cash levels at slightly above 15% across Magellan’s global and infrastructure strategies, the same weighting as at the end of March.

While it eerily feels like champagne corks are about to pop again in markets, Wheldon warns that the situation remains “highly uncertain” and a very wide range of health, economic and policy outcomes are still possible.

“We have adopted an even more cautious than usual posture. That has resulted in us increasing cash and increasing exposure to those businesses and sectors that we think will be most immune to both the initial shutdown period and the recessionary period that we expect to follow.”

In this wire, I cover Magellan's views and how they feed through into sector positioning and stock selection.

Signals for a recovery

Wheldon says Magellan still expect a range of economic outcomes, with a "deep and prolonged global recession" and a U-shaped cycle being the most likely scenarios. While we’ve previously covered Magellan’s base case outlook, he did share the signals they are waiting for before putting more cash to work:

- Meaningful reduction in the risk associated with the macro backdrop

- Improvements in the health aspects of this crisis, such as a vaccine

- Whether economic policy can keep unemployment low and support businesses as well as households, providing a floor for the economy to recover from.

Magellan is also willing to put more cash to work if all those risks remained but were “reflected in the price” to the extent that valuations become very attractive again.

“As we sit here today, we have a very cautious view about the macro landscape and for most equities we don’t find the risk-adjusted return prospect that appealing at the moment.”

Intersecting with the risks, Magellan is also considering critical long-term questions including: How will government balance sheets be restored? Will we see higher corporate tax rates and lower expenditures? Will we see an increased role for government in societies? Will all this stimulus increase the likelihood of inflation or deflation? What if we do not get a vaccine?

Increased convictions in big trends

In terms of investment considerations looking forward, Wheldon called out three areas of opportunity and increased conviction.

- The first is around digital and online trends including exposure to online shopping, payments, advertising, entertainment and so on. The businesses that are lacking those capabilities are being left behind in this environment.

- The second is the Chinese consumer. In a relative sense, Magellan thinks the Chinese economy is likely to fare better than most advanced and emerging economies. That should allow the growth within the consumption sector of the Chinese economy to experience less of a hit and less destruction than consumer trends in other economies around the world, which are facing greater impact from COVID.

- And then thirdly, they have incrementally greater conviction that long-term interest rates are likely to remain at lower levels for a longer period of time.

"If risk-free rates are being held lower because of slower economic growth or because of central bank policy over the medium to long term, all else equal, that has a positive impact on the value of all assets, including equities, which we think investors need to consider."

Blending the caution along with increased conviction in parts of the market has resulted in the following portfolio. Defensive stocks have the highest allocation, while luxury brands and discretionary names have the lowest weights in the global strategy.

Click to enlarge image.

Infrastructure set for bounce

In the infrastructure world, Gerald says the nature of this asset class is that it provides services essential for the efficient functioning of communities, so he is confident that the sector will bounce back.

However, infrastructure shouldn’t be viewed as a homogenous group; some sectors will benefit during a shock while others will see demand fall for a period. Gerald says one sector winning from COVID-19 lockdowns are communications towers, which underpins the movement of big data and internet usage.

As far toll roads and airports go, COVID-19 hasn’t fundamentally altered Magellan’s thesis about the movement of people.

“We’re of the belief that ultimately humans are social animals and that they will want to continue to travel and that they will want to continue to congregate together and work together.”

He reminds investors that toll roads are built because of population growth in a catchment combined with the fact that governments don’t want to build and own roads themselves. So long as there’s more people in that catchment, there will be more drivers.

Turning to airports, Gerald says there have been demand shocks before and while they change the way we travel, it will not change our need or desire to travel. For example, we’ve all become used to security arrangements in place after 9/11; the same will happen in a health sense after COVID-19.

Furthermore, he says on Magellan’s analysis most airports generally have 18-24 months of liquidity to survive with no passengers and need only 50% of passengers back to become profitable again. So even if demand takes a long time to get back to where it was, airports are well placed to ride out the storm.

Lastly, Gerald says lower interest rates will also benefit the sector overall.

“The bulk of infrastructure assets have a pretty significant amount of their capital structure in debt, and therefore, reduced interest rates also improve their underlying financials. So we would expect fundamentally better financials and a lower discount rate to apply to those earnings over the long run.”

You buy from the world's best companies, so why not invest in them?

Magellan believes that successful investing is about finding, and owning for the long term, companies that can generate excess returns for years to come. For more information on where they are seeing the most compelling opportunities, click the contact button below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

Gerald Stack,

Magellan

Gerald joined Magellan in 2007 and is Head of Investments and leads the team responsible for managing Magellan’s infrastructure portfolios and providing research coverage of companies within the infrastructure, transport and industrials sector.

Chris Wheldon,

Magellan

Chris is Portfolio Manager of Magellan High Conviction Fund and an Assistant Portfolio Manager on the global equities strategies. He joined Magellan in 2007 as a senior investment analyst and was promoted to become the Head of the Industrials Team.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

1 topic

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment