A short-term opportunity in the banks

Daniel Want

Prerequisite Capital Management

The conclusion of our December 2016 Livewire article read... “Such would suggest that the 2015 peak valuations in the Australian banking sector could indeed have marked the top of a multi-decade cycle for Australian banks. The latent risks confronting Australia’s banks appear significant, suggesting a high likelihood that in the years to come lower prices (and lower dividends) are probably in store for CBA, WBC, NAB and ANZ.”

In terms of 2015 representing a multi-decade cycle high of ‘peak optimism’ towards Australia’s banks, our conclusion still stands.

However, when we ‘zoom in’ on the time horizons to update how we are seeing the prospects for Australia’s banks, say over the next 12-18 months, our views are actually a little more constructive.

Quite simply, it appears to us that presently the big four banks are potentially oversold relative to the unfolding of actual conditions in Australia pertaining to the banks.

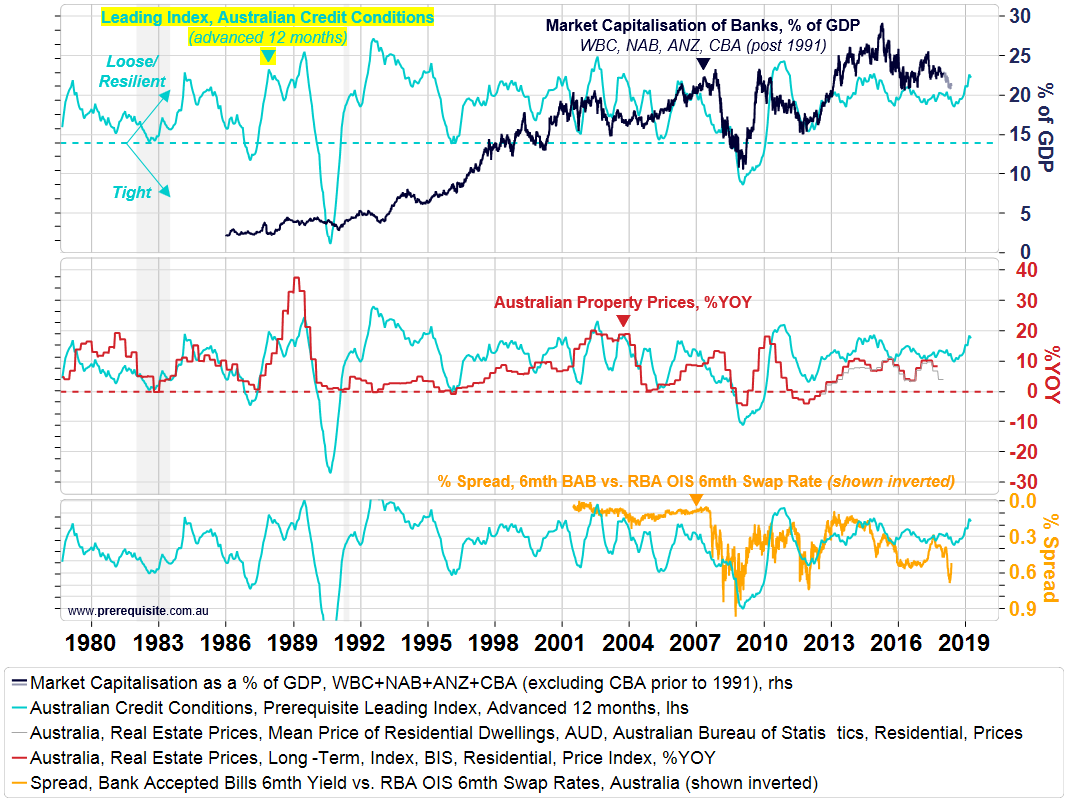

The below chart of one of our primary leading indicators shows that Australia’s credit conditions are still reasonably resilient despite the short-term pessimism that has built due to the Royal Commission and also a tightening of the Bank Accepted Bill market.

For the next 12-18 months, we could actually be in for some positive surprises with the banks. However this scenario would rest on two key assumptions; (1) that the Australian Government and Regulators are unlikely to ‘kill the golden goose’ by being too aggressive in policy changes as a result of the Royal Commission, and (2) we do not have any shocks originate internationally that impact Australia.

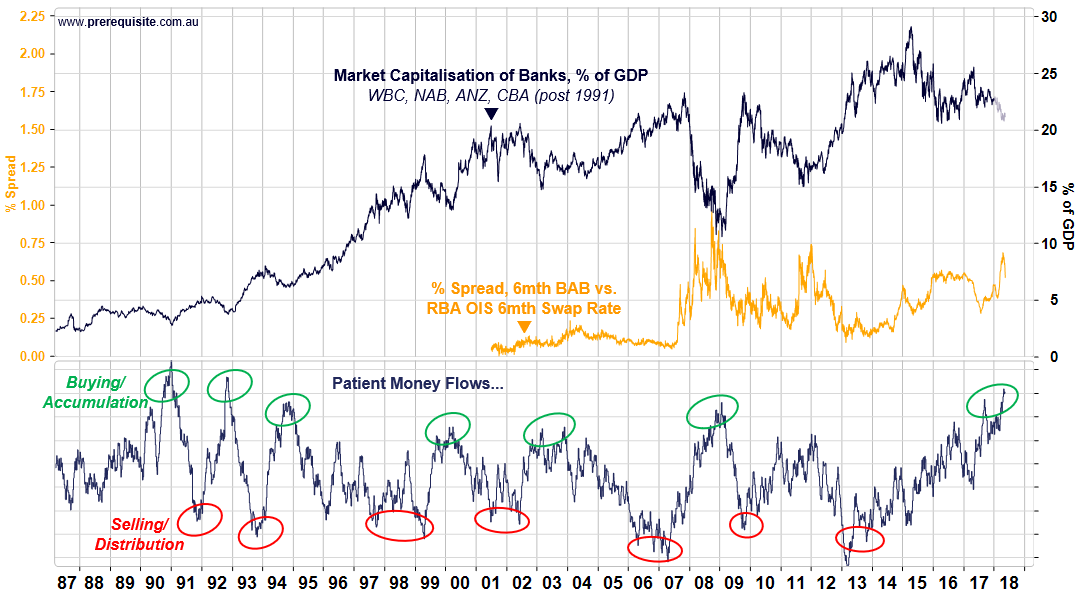

Even our money flow tools suggest that the ‘Patient Money’ is accumulating our Banks once again (see our latest Quarterly Letter for further explanation of these money flow tools). Although we should note that the behaviour of these participants can swing quite dramatically in a limited period of time (see the early 1990s) so we’ll need to monitor this for tactical cues over the next year or two.

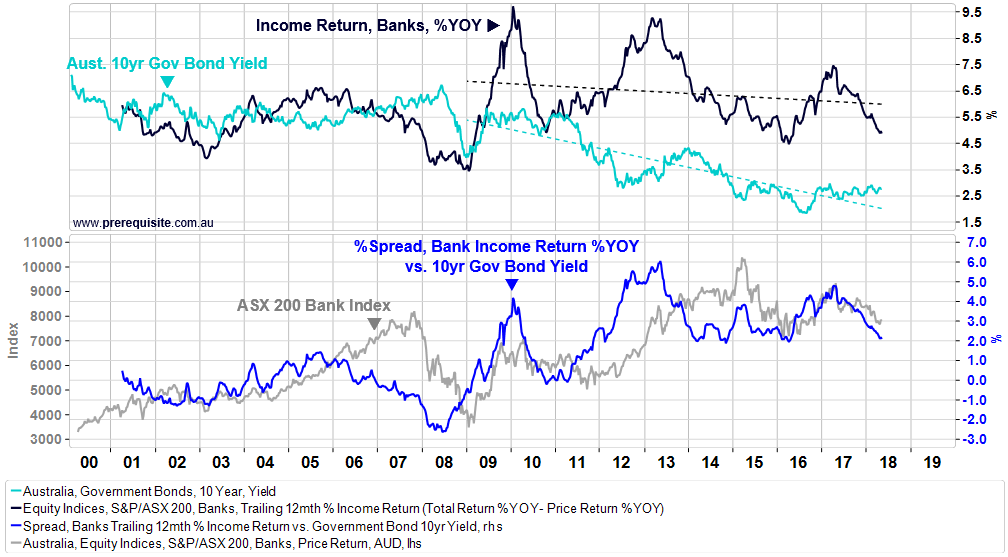

Likely because the yield differential is still too attractive to ignore, especially with the Royal Commission taking the wind out of the sails of the stock prices (short term). This next chart is a bit ‘simplistic’ but it illustrates the point in a very practical manner...

However, we would temper this 12-18 month possibility of short-term positive surprises with the fact that our broader analysis still suggests that banks will likely be much lower than they are now in 3-5 years time. Accordingly, our portfolios are still skewed away from Australia’s banks.

We are also mindful of the non-trivial risks also building within the global banking system and financial environment, and so on a longer multi-year basis, we are not optimistic as to the prospects of Australia’s banks (see another of our Quarterly Letter’s dated January 2018 that explains this in summary).

To conclude, for the next 18 months we see risks and opportunities balanced somewhat concerning the banks, with possibilities for positive upside surprises. But over the next 3-5 years, the risks (and likelihood of outcomes) for Australia’s banks are skewed heavily to the downside. Caution is advised.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

2 topics

4 stocks mentioned

Daniel Want

CIO & Co-founder

Prerequisite Capital Management

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

Expertise

Daniel Want

CIO & Co-founder

Prerequisite Capital Management

Daniel oversees the research, consulting and investment management activities of Prerequisite Capital Management (www.prerequisite.com.au).

Expertise

Comments

Comments

Sign In or Join Free to comment