Non-financials scream value

David Gallagher

Artesian

SWINGS AND ROUNDABOUTS

COVID-19 has caused significant swings in pricing among almost all asset classes. Much of the pricing action intuitively makes sense, some of it is harder to rationalise – we will explore some of those pricing opportunities that have become evident in this piece.

March and April presented opportunities and posed questions for investors. Is the ASX down -35% cheap? Is Crude Oil at $10 a barrel a bargain? Are listed investment trusts trading at a 50% discount to their net tangible asset value an opportunity? What about major bank senior bonds trading at BBSW +180bps? What do all these numbers really mean?

Unfortunately a lot of those opportunities no longer exist in the market, you needed to make those calls in either March or April, maybe you will get another chance in 2020, maybe you won’t. However, one opportunity that still exists is in the AUD corporate bond market.

Global corporate bonds were trapped in the COVID-19 liquidity crisis, the financial sector (retail banks, investment banks, brokers etc.) along with the non-financial sector (TMT, consumers, industrials, utilities, REITs etc.) were thrown to the wolves as global fund managers sold what they could to facilitate redemptions. Global central banks then stepped in to provide support in the form of liquidity, which calmed markets and credit spreads. The RBA has been very effective in the domestic market, due to the RBA’s Yield Curve Control (YCC), government bond yields now trade within historically tight ranges. This poses another dilemma for investors in the shape of how to protect an equity portfolio, does interest rate duration still work for this purpose? We would suggest not. The risk/reward in duration was asymmetric before COVID-19 and the RBA’s YCC has just strengthened our view.

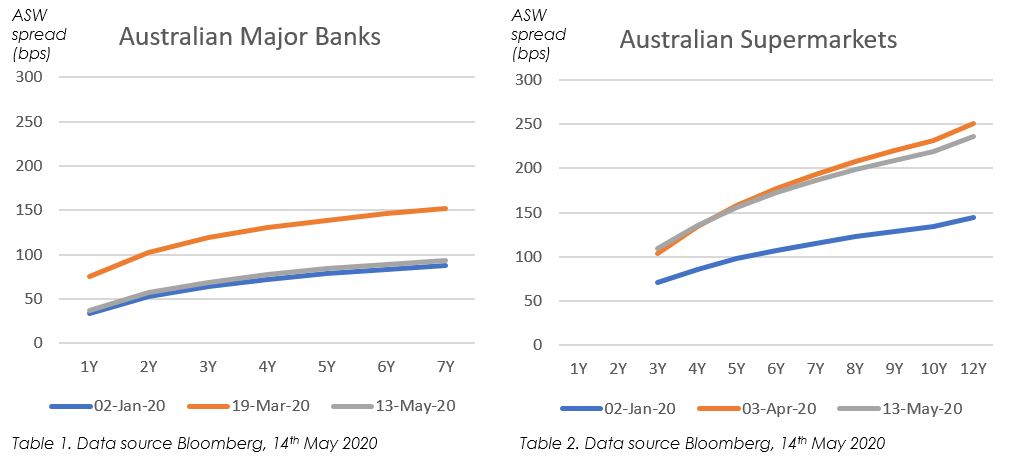

Outlined in our previous piece, the financial sector, in particularly the major banks senior debt has reverted to their pre COVID-19 spread levels. Conversely, the non-financial sector has lagged and is still quite wide to where their credit spreads were pre COVID-19. Let’s take a look at some relative value analysis between the Australian major banks (ANZ, CBA, NAB & Westpac) and Australian supermarket behemoths, Coles & Woolworths.

The above charts uses Bloomberg data to build a regression curve (linear-log), simply put we use these company’s bond prices to provide a curve of best fit for all outstanding bonds across maturities from 1 year to 10 years. The Y axis is the asset swap spread, which normalises the risky spreads of all the underlying corporate bonds so we can do a fair comparison.

It appeared to us that the worst day for Australian major bank’s senior spreads was on or around 19th March, similarly for Coles & Woolworths their worst day peaked on or around 3rd April – hence curves were built to reference these dates. The other two curves represent the start of the year pre COVID-19 and now.

The major banks have reverted almost all the way back to their pre COVID-19 levels. Coles & Woolworths however, have hardly retraced any of their spread widening.

WHAT DOES THE EQUITY MARKET TELL US?

Data source Bloomberg, 14th May 2020

The major banks have all underperformed the ASX and both Coles and Woolworths have significantly outperformed the ASX. Year to date Coles is actually positive 1.33% and Woolworths is a small negative at -3.42%. Compared to the majors which are down -24% to -37%, the ASX is down only -19%.

Data source Bloomberg, 14th May 2020

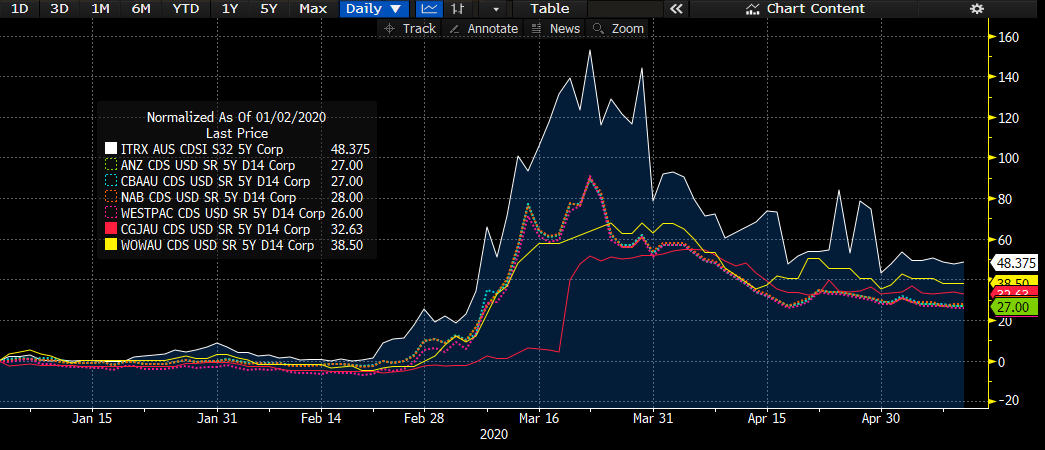

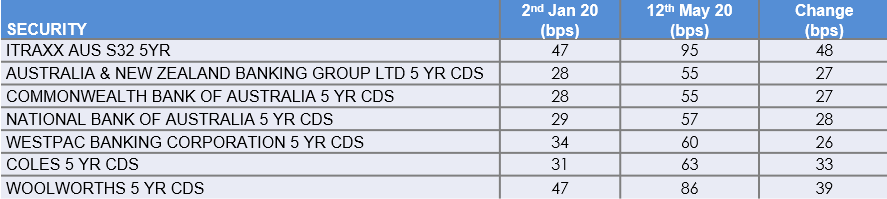

WHAT DOES THE CREDIT DEFAULT SWAP MARKET TELL US?

Using the 5 year credit default swap spreads for the major banks, Coles & Woolworths we can see that these spreads have all been quite positively correlated. However, the major banks underperformed in the middle of March when the markets were at their most stressed. The market took the view that the credit risk of the major banks had increased more than the credit risk of Coles & Woolworths.

Another observation is that neither the major banks, Coles or Woolworths are back to their pre COVID-19 spread levels, therefore the market believes all of these companies now pose more credit risk than pre COVID-19.

Data source Bloomberg, 14th May 2020

HAS THE MARKET STARTED TO REPRICE?

In our opinion the non-financial sectors of the market still represent considerable value when compared to the senior debt of major banks which look relatively fully priced. Can major banks continue to go tighter than their pre COVID-19 levels, faced with increasing bad debts and sluggish loan growth? Regardless, we believe that the prospects for many of the undervalued non-financial corporates who haven’t been overly effected by COVID-19 remain the best opportunities.

May 5th the RBA announced that it had broadened the range of corporate debt securities that are eligible as collateral for domestic market operations to include investment grade. This will have a positive impact on AUD non-financial corporate bond spreads. Up until now, only senior ranking, highly rated financials were eligible which was a driving factor behind the mean reversion of their spreads to pre COVID-19 levels. We now expect similar price action in high quality non-financial corporates that are RBA eligible.

Since COVID-19 the new issue market for non-financial corporates has essentially been closed. That changed this week, a commendable effort by ANZ, CBA, NAB & Westpac who were the lead arrangers in a 5yr and 10yr bond issued by Woolworths. Woolworths also deserves a pat on the back from investors for being responsible for kick starting the new issue market again for non-financials.

Woolworths issued AUD 400m 5yr at ASW +145bps and AUD 600m 10yr at ASW +195bps. As you can see by referencing Table 2, both of these bonds priced just inside our 13 May 20 implied curves and where we saw fair value. However, with considerable demand for non-financial bonds at these elevated levels, Woolworths attracted bids greater than AUD 2.82 billion, versus their total amount issued of just AUD 1 billion. At the time of writing both bonds have buying interest 5bps to 10bps inside their issue spreads in the secondary market, a great result for the issuer and investors.

CONCLUSION

Whilst we have used a relative value opportunity in this piece between Coles, Woolworths and the majors, many others exist for the same reasons. As the new issue market for non-financials reopens and volumes increase, we believe that the spreads between the major banks and good quality corporates will compress to their historical ranges. The technical arguments for major banks senior spreads being RBA eligible, is now also applicable to investment grade corporate bonds.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS. David has extensive investment and PM experience.

........

Artesian Corporate Bond Pty Ltd (ACN 618 342 895) has been appointed as the investment manager in respect of the Fund. Artesian Venture Partners Pty Ltd ABN 58 112 089 488 holds an AFS license no.284492 and has appointed the Investment Manager as its authorised representative (number 001260177). Equity Trustees Limited (‘EQT’), ABN 46 004 031 298, AFSL 240975, is the Responsible Entity for the Fund . This information has been prepared to provide you with general information only. Some of the information in this document may be derived from third parties. We do not express any view about the accuracy or completeness of information that is not prepared by us and no liability is accepted for any errors it may contain. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information. Past performance should not be taken as an indicator of future performance. In preparing this information, we did not take into account the investment objectives, financial situation or particular needs of any particular person. You should obtain a copy of the product disclosure statement before making a decision about whether to invest in this product. Copies of the product disclosure statement can be obtained by visiting www.eqt.com.au/insto or request a copy by emailing the Investment Manager at bondoperations@artesianinvest.com, visiting www.artesianinvest.com or calling +61 3 9288 9444. Distribution of this information to anyone other than the original recipient and that party’s advisers is unauthorised. Any reproduction of these materials, in whole or in part, or the divulgence of any of its contents, without the prior consent of Artesian is prohibited. Any securities recommendation or comments (including an opinion) contained in this document is general advice only and does not take into account your personal objectives, financial situation or needs. Artesian and EQT are not acting in a fiduciary capacity. Recommendations or statements of opinion expressed may change without notice. You should not act on a recommendation or statement of opinion without first considering the appropriateness of the general advice to your personal circumstances. Nothing in this document should be construed as Artesian or EQT providing an opinion, statement or research dealing with the creditworthiness of a body or the ability of an issuer of a financial product to meet its obligation under the product.

1 topic

6 stocks mentioned

David Gallagher

Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund

Artesian

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS....

Expertise

David Gallagher

Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund

Artesian

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS....

Expertise

Comments

Comments

Sign In or Join Free to comment