One of the most dangerous things an investor can do

The market corrections in February and October should be a warning to investors that the stock market is highly cyclical. It was inevitable that ‘growth’ stocks, which pushed the market to new highs for many months eventually led the collapse. Investors who paid heed to Howard Marks’ famous quote on cycles would have largely avoided the October sell-off:

“Ignoring cycles and extrapolating trends is one of the most dangerous things an investor can do” - Howard Marks

Seasoned investors like Howard Marks profess to not being very good at forecasting the future but attempt to understand the current environment to prepare for risks. When cyclical risks are elevated he has a greater focus on preserving capital.

A cautionary tale from Apple

While there are good reasons for many ‘growth’ stocks having structurally higher earnings growth, investors sometimes forget that the rate of earnings growth is cyclical.

To be clear, earnings do not have to go backwards (as they do for value traps) but just need to be revised down for investors to worry. The combination of high valuation multiples with greater uncertainty about earnings growth is all that it takes for a share price to collapse.

The dangerous environment for ‘growth’ stocks is best highlighted by the world’s largest company, Apple:

In August 2018, Apple seemed like it could do no wrong. It was trading on its highest PE multiple in 8 years, at 17x with 3-year forecast earnings growth of about 17% per annum. Then, in early November at its 4th quarter results, Apple hosed down investor expectations citing emerging market uncertainty affecting iPhone sales. Now, the 3-year forecast earnings growth has been revised down to 12% per annum with the stock trading lower on a 14x PE multiple. Even the world’s greatest investor, Warren Buffet, who bought at elevated stock prices could not stop the share price slide.

Apple’s recent earnings revision highlights that while its earnings have consistently grown, the rate of growth is cyclical, linked to the health of the global economy. It wasn’t long ago, in 2016 when global growth was weak, that Apple revised down earnings expectations significantly. During that time, Apple traded around a 10x PE multiple with net cash of about $150 billion on its balance sheet.

Apple will not be an isolated case. If a trillion-dollar market cap company can feel the effects of a global slowdown then it’s a sure bet that other companies will eventually experience something similar. In Australia, there are many technology stocks that will not be immune from a cyclical slowdown.

Aussie credit slowdown effects more than just the banks

Currently, there is a strange disconnect between the market being bearish on Aussie banks because of lower credit growth while many technology stocks are richly priced.

The truth is that the economic consequences of low credit growth extend beyond just the banks, and it will permeate through most areas of the Australian economy.

If the economy is weak it will eventually lead to:

- lower property listings (affecting REA Group and Domain Holdings Australia),

- lower car sales (affecting Carsales.com), and

- lower employment (affecting Seek).

Even Afterpay Touch is not bulletproof when consumer bad debts spike, if economic growth slows dramatically.

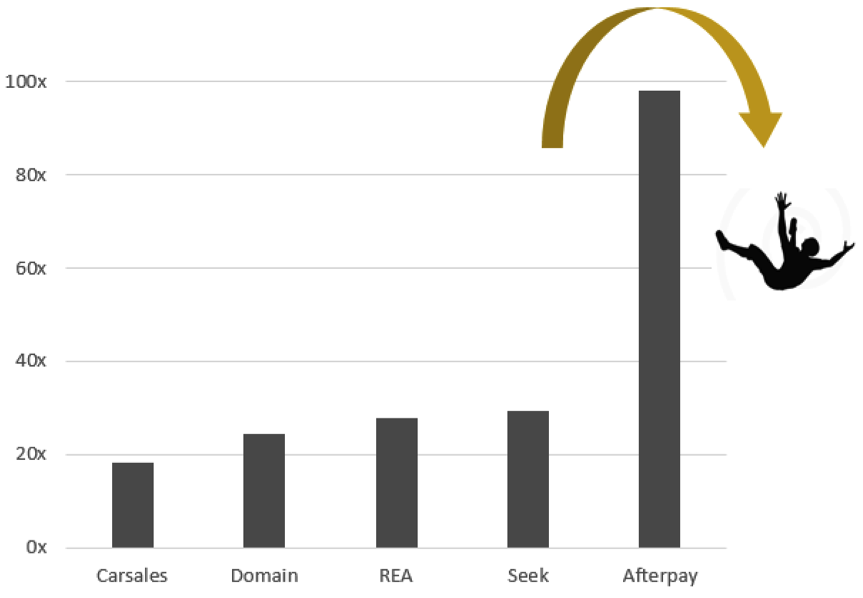

Aussie technology stocks will fall off the PE cliff when cyclical risks appear.

Chart1. Aussie Technology PE multiples

Source: Factset, Vertium

So be warned … if you accept the view of lower credit growth in Australia then the investment case for many technology stocks are extremely risky.

Their high PE multiples are not factoring cyclical risks in the economy.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

1 topic

4 stocks mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment