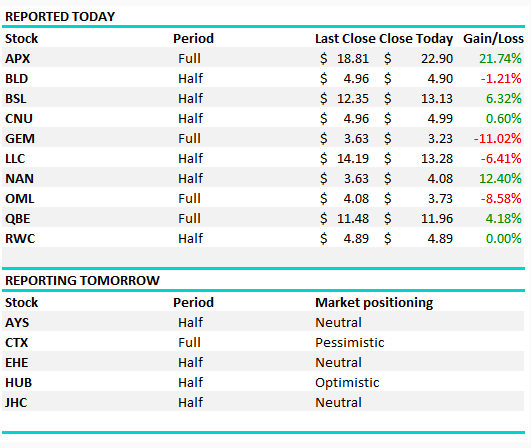

QBE enjoys a rare (reporting day) in the sun

The market was strong early however showed some signs of weakness again during the middle part of the day before a late flurry in the last 20mins saw the index close higher. The Chinese market was strong today adding more than 3% while the rest of Asia tracked higher, although not a patch on the Chinese move.

The biggest day of reporting for the week played out today however we are now starting to taper down after a fairly hectic few weeks. Overall, results were on the positive side today with two stocks we hold reporting numbers – both finishing higher on the session. At the sector level the high growth part of the market dominated the leader board headlined by AI company Appen (ASX:AHX) which delivered a great set of results (once again) and rallied more than 20% on the day. QBE was also strong adding more than 4% - sounds pretty lacklustre next to APX – but QBE rallying on results day has been a rare phenomenon in recent times. We cover these results and more below.

The ASX 200 added +19points or +0.31% to 6186. Dow Futures are currently trading up 61pts / 0.35%.

ASX 200 Chart – BANG – late rally into the close

ASX 200 Chart

CATCHING OUR EYE

Buy now pay later space (BNPL) – these stocks were hot today with AfterPay Touch (ASX:APT) up +19% while Zip Co (ASX:Z1P) was up 3.8%, although it was up a lot more early and there were some decent lines taking profit in the stock today.

On Friday, the Senate committee released a report and the outcomes where clearly short term positive for the sector. The main risk was that the BNPL space would be rolled into the National Credit Code requiring more stringent credit checking before any credit could be provided. This would have been a big issue for AfterPay’s model. That hasn’t happened and the outcome was good for now, however the issue has not been settled, specifically around whether or not credit is actually being issued. More to consider here and I doubt this issue has been put to bed in its entirety.

Here is what was said… That the government consider in consultation with ASIC, consumers and industry, what regulatory framework is appropriate for the BNPL sector – Considering that before credit is extended, providers appropriately consider consumers personal financial situations; 2) Rec 10 – BNPL develop code of practice; and 3) Rec 2) NCCP Amendment Act for SACC and leases be introduced and facilitated by government.

APT’s response was…."Afterpay supports the Committee's recommendations relevant to the BNPL sector as they are sensible, appropriate and a proportionate policy response to the BNPL industry."

AfterPay Touch (ASX:APT) Chart

Reporting today; A good session overall from those that reported – APX the star while G8 Education missed and was sold off. Reporting starts to taper off this week after a very hectic period.

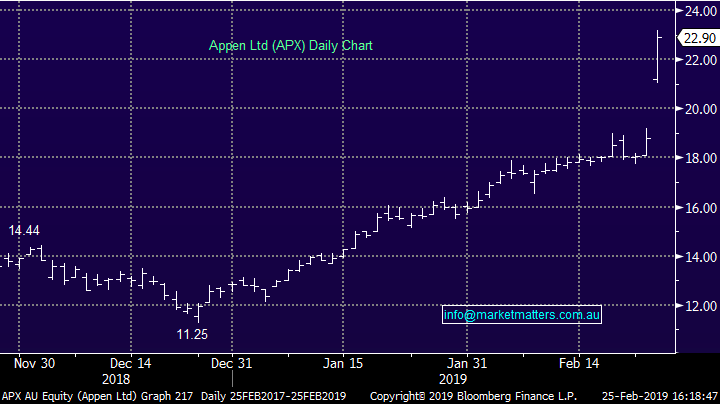

Appen (ASX:APX) +21.74% ripped higher again today as it once again delivered a cracking set of results that beat prior guidance plus eclipsed market expectations. The market has very few legitimate growth exposures in industries like artificial intelligence and APX is clearly nailing it. They guided in November for EBITDA of $62-$65m for the half and the market was at the top of that range at $65.26m, however they beat that printing $71.3m while they guided to $85m-90m for the full year. This is a stock that was sold off fairly hard in October / November hitting a low below $10 and has recovered to close today at $22.90 – clearly a massive move. We bought this well but sold too early.

Appen (ASX:APX) Chart

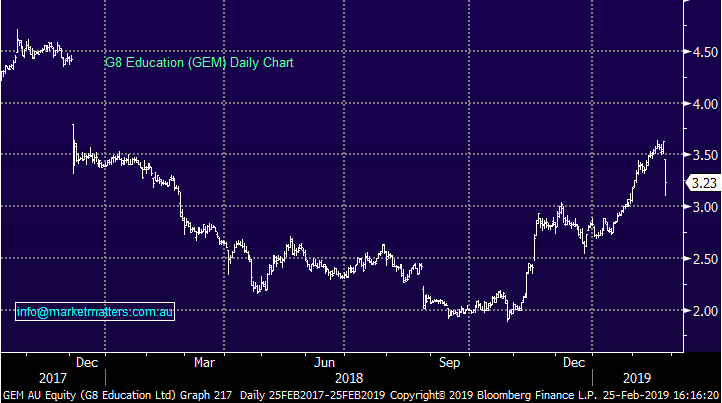

Childcare operator G8 Education (ASX:GEM) -11.02% reported full year numbers today and the stock was sold off hard. GEM has been a tear leading into the result so the market was clearly looking for a better set of numbers. Underlying EBIT came in at $136.3m versus expectations for $137.5m, so a small miss however it was the occupancy levels and a more sanguine outlook that seemed to get the sellers out and about. Average occupancy came in at 74% which was down 1.9% during the year, however they did say that supply growth in the industry was showing signs of moderating.

We have G8 on the radar and today’s decline looks interesting. The stock is reasonably cheap (15x) and they’ve got a turnaround under way.

G8 Education (ASX:GEM) Chart

Bluescope (ASX:BSL) +6.32% released their first half numbers this morning and they beat fairly low expectations. Underlying NPAT came in at $613m versus ~$600m expected and the operational metrics were all pointing to improvement, the only real issue was around guidance which was for EBIT growth of 10% for FY19. That implies EBIT of $1.395b while consensus sits at $1.455b – so a slight miss. However given the stock has traded down from near $19 to a recent of sub $11, it doesn’t take a lot to unearth some buyers looking for value in a hot market.

Bluescope (ASX:BSL) Chart

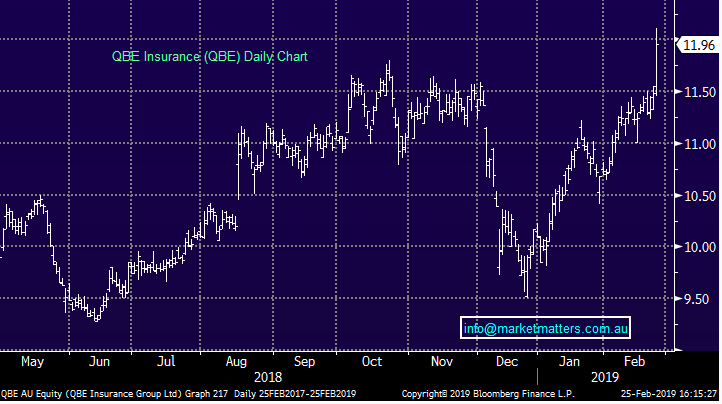

QBE insurance (ASX: QBE) +4.18%; It might look like another miss for QBE on face value, but the market has bought today’s result and the stock has tracked higher in the session. The core business is tracking well and signs that the downgrade cycle might be behind them are appearing. Earnings at $US715m was a tad below consensus of $US718m, however the underlying drivers for future growth in the business are improving. Gross written premium grew around 4% in the year while average repricing added 5%. The attritional claims ratio is moving lower, as is the expense ratio which came to 15.3% and is expected to fall to below 14% over the new 3 years. The company is also doing its bit to de-risk as it continues to recover from the multiple disasters in 2017 which greatly impacted QBE’s capital position. Gearing fell to 38%, down over 2 percentage points in the 12 months, and now targeting 25%-35% going forward.

Certainly QBE is trending in the right direction, but there is a long way to go before it is fully recovered. The new management team is doing a good job at lowering costs and driving revenue higher while focussing on the core businesses – the simplification process is working. QBE still trades on a reasonable discount to global peers (about 15%) and this discount will close if QBE can continue to execute. We hold QBE in the Platinum Portfolio, but are closer to the sell side here after its solid rally over recent weeks.

QBE Insurance (ASX: QBE) Chart

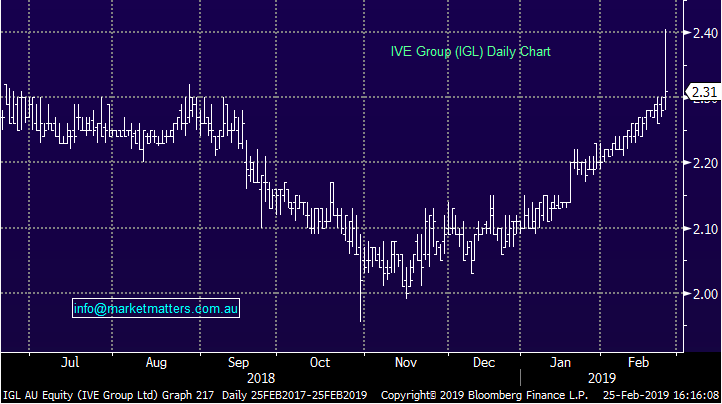

IVE Group (ASX: IGL) +1.32%; which resides in the MM Income Portfolio reported half year results this morning, the stock popped initially but closed just marginally higher (+1%). As a quick refresher, IGL is a diversified marketing, communications and print business that has its competitive advantage through high quality equipment – and the most pleasing aspect of the result today was the better utilization from recent asset purchases. Printing is now a tech heavy business and IGL is at the forefront of it servicing a lot of household names across Australia.

Today they reported revenues of $375.6m which was up 4.5% on this time last year dropping down to a statutory net profit of $17.6m. The dividend came in at 8.6cps which was up 7.5% on last year, representing a fully franked yield of 7.5%+. Trading on a PE of 8.6x & growing the stock remains good value. They provided guidance of delivering solid earnings growth for full year – although they didn’t give specific numbers around that. IGL has traditionally delivered messy numbers with a lot of ‘one-offs’ baked into them, however todays result was one of the cleanest in recent memory.

IVE Group (ASX:IGL) Chart

Broker Moves;

· Australian Finance Raised to Outperform at Macquarie; PT A$1.43

· Huon Aquaculture Downgraded to Neutral at JPMorgan; PT A$4.40

· Huon Aquaculture Downgraded to Neutral at Goldman; PT A$5.10

· Orocobre Downgraded to Hold at Baillieu Holst Ltd; PT A$3.22

· Flight Centre Downgraded to Sell at Morningstar

· Challenger Downgraded to Hold at Morningstar

· Charter Hall Group Downgraded to Neutral at JPMorgan; PT A$9

· Treasury Wine Upgraded to Overweight at JPMorgan; PT A$17.50

· Rio Tinto Upgraded to Neutral at Oddo BHF; PT 44 Pounds

· MyState Downgraded to Hold at Bell Potter; PT A$5

· Antipa Rated New Speculative Buy at Hartleys Ltd; PT A$0.06

Never miss an update

Stay up to date with the latest news from Market Matters by hitting the 'follow' button below and you'll be notified every time I post a wire.

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

5 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets